In the sixth episode of Insiders and Outliers, Carlos Hardenberg, founder and portfolio manager of MCP, explains how on-the-ground research trips add an edge to MCP’s investment process, and draws on his recent visit to Vietnam to unpack the country’s rapid economic growth over the past few decades. He shares key insights into Vietnam’s vibrant technology sector, its rapid digitisation, its emergence as a manufacturing hub, and the addition of a new high-conviction Vietnamese holding following the trip.

The world’s attention is fixed on the outcome of what many have called one of the most divisive U.S. elections in recent history. Yet the results are anything but close, with a Republican sweep across the Senate, likely the House of Representatives, and, of course, the presidency, secured by Donald Trump. Businesses and governments worldwide are now asking how a second Trump presidency will affect them. Given Trump’s notorious unpredictability, the answer for many is not straightforward. At MCP, we’re asking the same for Emerging Markets and, despite the often pessimistic narrative, we’ve identified several potential silver linings in a Trump presidency.

Trump’s Domestic Economic Policies:

Trump positions himself as a champion of “the people,” and if that term refers to America’s wealthiest individuals and business leaders, he may be right. A central pillar of his domestic economic agenda is tax cuts, and with a Republican majority, an extension of the 2017 Tax Cuts & Jobs Act is highly likely. This act established a flat corporate tax rate of 21% and lowered individual tax rates, with the wealthiest Americans seeing the greatest benefit. Additionally, Trump has consistently advocated for deregulation, especially in sectors like digital assets and non-renewable energy.

Much like the pre-election polls, economists are divided on whether Trump’s next term will ultimately harm or hinder the U.S. economy in the long term. However, there is general consensus that, in the short term, Trump’s pro-business policies are likely to stimulate US economic growth. Herein lies the first silver lining for EM: a strong US economy has positive spill over effects on the global economy as it boosts demand from U.S. consumers for EM exports.

Trump, Trade and Tariffs:

However, the subject of Trump and trade is particularly sensitive for EM and Trump’s clear ‘America First’ stance is hard to ignore. Trump has been outspoken about his support for tariffs, yet both DM and EM may be left out in the cold as Trump has threatened a universal 10-20% tariff on all trading partners and indicated replacing income tax with tariff revenue via the proposed “Trump Reciprocal Trade Act.” That being said, China will clearly be the most effected with Trump advocating for a 60% tariff on Chinese imports.

It may be wise not to take such threats at face value. Trump himself has described tariffs as a powerful negotiation tool and he might actually use them as such. The reality is that the U.S. remains heavily reliant on imports, particularly from China, whose production capacity is unparalleled. Although there is momentum behind reshoring manufacturing, reducing the U.S.’s global trade deficits through this approach is likely a long-term endeavor, potentially spanning decades. This economic interdependence could restrain Trump’s ability to impose sweeping punitive trade measures without risking inflation and considerable supply chain and economic disruptions domestically.

Differing Impact on EM Regions:

While finding a silver lining in China itself may be challenging, it’s much easier to spot ones in countries like India, Indonesia, Vietnam, Malaysia, and Mexico. These nations, known for their low-cost manufacturing, are set to become even more attractive to FDI as the global shift to “China+1” accelerates. As higher tariffs on China undermine its cost competitiveness, supply chain gaps will emerge, offering these countries opportunities to meet the demand and capture a larger share of global manufacturing. This increase in production could help offset the negative effects of higher tariffs on their exports to the U.S.

Moreover, escalating U.S.-China trade tensions could create opportunities for other EM to strengthen their trade relationships with China. For example, during the trade war in 2018, China shifted from importing U.S. soy beans to sourcing them from Brazil. Similar patterns of retaliation could benefit countries with strong trade ties to China or those that produce goods that can replace US exports.

Resilience in EM:

Emerging Market companies have demonstrated their resilience, thriving even amidst geopolitical and economic uncertainties, thanks to robust business models, innovation, and strong growth prospects. Structural advantages such as favourable demographics, higher GDP growth projections, and ongoing digitalisation ensure that EM will remain competitive, despite potential tariff-related challenges.

While Trump’s presidency introduces a degree of unpredictability, more clarity over Trump’s intentions in the months ahead along with administration appointments is expected to reduce short-term market volatility. Although Trump’s policies pose risks to the global trade order, the outlook for EM is not all doom and gloom. In fact, certain EM regions stand to benefit from new growth and investment opportunities stemming from shifts set to accelerate under Trump such as China+1. We are confident that this resilient asset class will navigate these turbulent times as effectively as it did during Trump’s first presidency, during which the MSCI EM Index delivered a 57% return in USD terms1.

1 Bloomberg: From 20 January 2017 – 20 January 2021

Navigating Market Swings: Reflections on Volatility in Investing

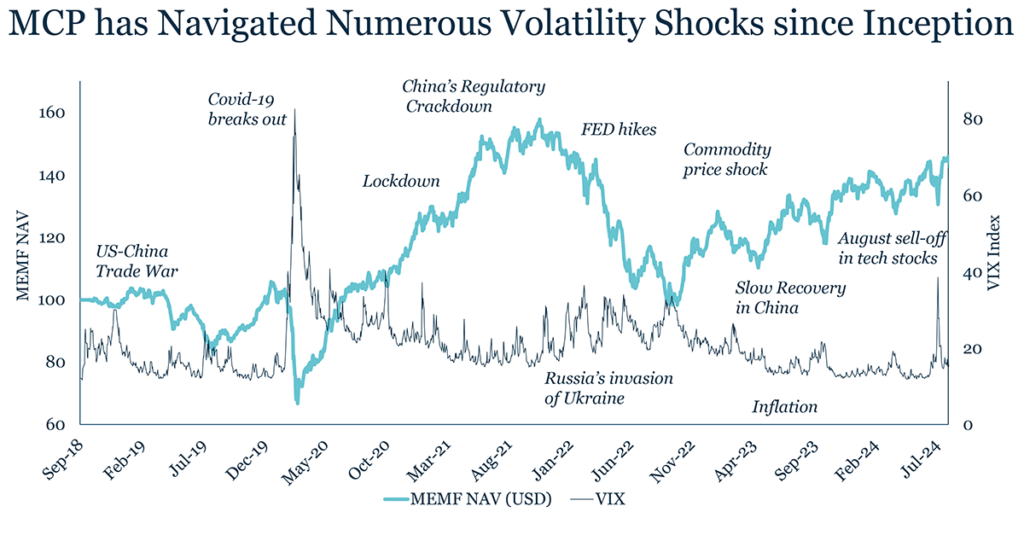

Navigating volatility has always been a priority for the MCP investment team, not just to mitigate risks but also to proactively capitalise on the opportunities that market fluctuations present. Given the recent spike in volatility this summer, we thought it was an opportune time to share our insights on navigating market turbulence, drawing on Carlos Hardenberg’s 25+ years of experience. Beginning his career during the Asian financial crisis, Carlos has navigated the dotcom bubble, the global financial crash, the Covid-19 pandemic and numerous other market disruptions. His experience as a long-only equities investor has only reinforced the idea that volatility can be your friend if you use it effectively.

Understanding Volatility

Managing market volatility starts with understanding its causes — asking why investors buy one day and sell the next, often without any significant change in fundamentals. This behaviour is rooted in the fear of the unknown, a human characteristic to which investors are not immune.

Source: Bloomberg. As of 30 September 2024.

Uncertainty leads to nervousness, causing a risk-averse instinct which, in investing, often leads to sell-offs. The herd mentality exacerbates the situation — as everyone else sells, the fear of being left behind and suffering greater losses grows stronger, pushing more investors to follow suit. The widespread use of algorithmic trading, most of which trades on the same set of predefined conditions that mirror market movements, compounds the effects of sell-offs and thus increases volatility further. In 2018, Select USA estimated that algorithms now dominate 60-75% of trading in major US, European and Asian markets.

Leveraging Volatility

In times of volatility, we believe it is important to remain calm and focus on fundamentals and the long-term. We seek high-quality companies with excellent management teams, strong moats, positive cashflows and little to no debt. These companies are more likely to prove resilient and maintain a positive outlook. Nevertheless, we always monitor macro developments and their potential impact on our investment case very closely. Timing is critical in responding to changing macro and micro conditions — selling too early or too late can have significant consequences. Yet 25 years of investment experience has taught Carlos that selling on volatility alone usually leads to poor investment decisions. During the 2008 global financial crisis, many investors fled risk assets such as emerging markets, resulting in a vast pool of undervalued EM stocks despite their strong fundamentals and sound business models. Rather than following the herd, Carlos leveraged the volatility as a source of additional alpha generation. By staying disciplined, closely monitoring his investments and adjusting his strategy when needed, he was well positioned to capitalise on these mispriced assets during the subsequent recovery, thereby leveraging uncertainty as a friend. Similarly, during the Covid-19 pandemic, the team swiftly repositioned the portfolio, seizing the opportunity to add high-quality companies from our watch list. These companies were being unfairly dragged down by market sentiment. This timely and strategic response, we believe, contributed significantly to the fund’s strong outperformance.

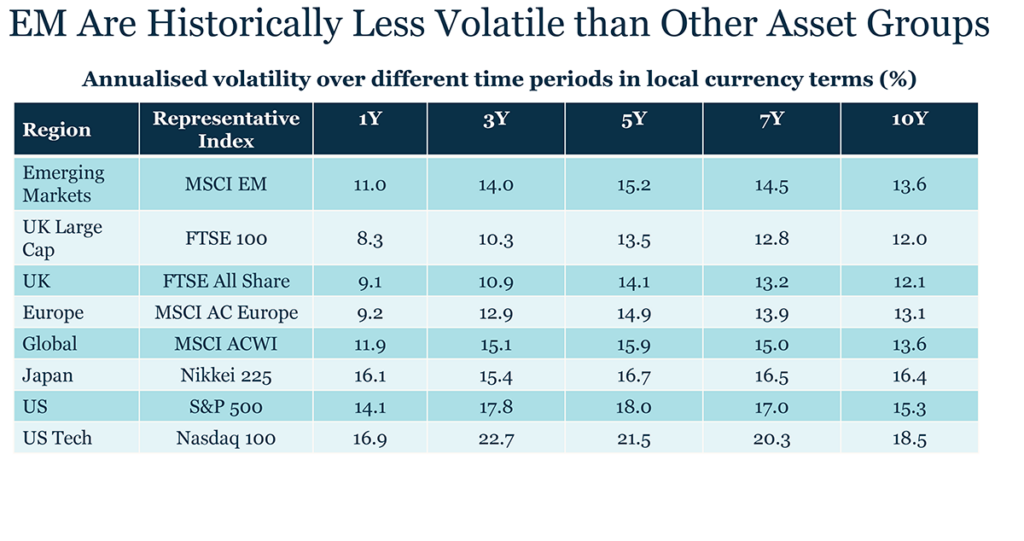

Interestingly, over the past decade, US equities have been more volatile than emerging markets in local currency terms. One reason could be the high concentration of the US market. Since 2014, big tech companies have rapidly increased their market dominance, with the ‘Magnificent 7’ now accounting for around 30% of the S&P500. In a highly concentrated market, sell-offs can become more severe as many investors rush to offload the same stocks, leading to outsized losses for those who remain invested. Historical examples have showcased the risks inherent in highly concentrated markets. For example, the dotcom bubble era was dominated by five tech stocks, which were quickly sold off when the bubble burst, contributing to the 78% loss in the Nasdaq index from its peak in March 2000 to its low in October 20021.

Source: FE Analytics

Market Concentration and Volatility

While the high concentration of the US market is widely recognised, many investors do not realise that the situation is similar in emerging markets. In the MSCI EM Index, the top 10 companies account for approximately 25% of the total index weight, despite there being around 1,300 constituents in total. In addition, many of the bulge-bracket EM funds’ portfolios are similarly concentrated in these top 10 names, potentially increasing their vulnerability to significant drawdowns during market sell-offs. This highlights the importance of portfolio diversification. We prefer smaller, lesser-known innovative companies in emerging markets, particularly in sectors like AI and the semiconductor supply chain, which we believe have a strong potential to deliver alpha.

Monetary Policy, Volatility and Emerging Markets

One of the main sources of volatility this year has been the Federal Reserve’s decisions regarding interest rate cuts. While the pace of future cuts and any unexpected employment or inflation data may continue to cause market fluctuations, the direction is now clear with the first cut behind us. Our focus, however, remains on the impact of these rate cuts on emerging markets rather than the short-term volatility around Fed meetings. With rates trending lower, as demonstrated by the Fed’s half-point cut on 18 September, we believe emerging markets are poised to benefit. Lower interest rates in advanced economies typically weaken the dollar, which in turn supports EM currencies and eases the burden of dollar-denominated debt.

Since 1988, EM equities have, on average, outperformed DM equities in 4/5 Fed rate-cutting cycles returning 29% in the 24 months following the last Fed rate hike2. Moreover, while many LatAm countries are ahead in the rate cutting cycle, Asian countries have been more cautious. Fed cuts now give many of them more room to begin their respective cutting cycles, thereby enabling cheaper borrowing, improving consumer sentiment and corporate spending, and stimulating growth.

Source: Maybank Research, Bloomberg, local sources. As of September 2024.

In addition, lower US interest rates can benefit emerging markets by reducing the attractiveness of safer, lower-yielding assets in developed markets, encouraging investors to seek higher yields in EM, increasing FDI flows and supporting EM asset prices. However, this impact varies across emerging markets as increased risk appetite and lower US yields cannot offset poor macroconditions or weak corporate fundamentals. For example, in the rate-cutting environment of 2019, Taiwan saw strong FDI inflows of $8.2bn, up 16% from 2018, while Argentina, with weaker fundamentals saw a 43% drop in FDI to $6.7bn3. Therefore, maintaining a robust macroeconomic overlay, combined with diligent stock selection, remains essential. This approach focuses on companies with strong fundamentals and resilient business models that can capitalise on a lower interest rate environment.

Volatility around Elections

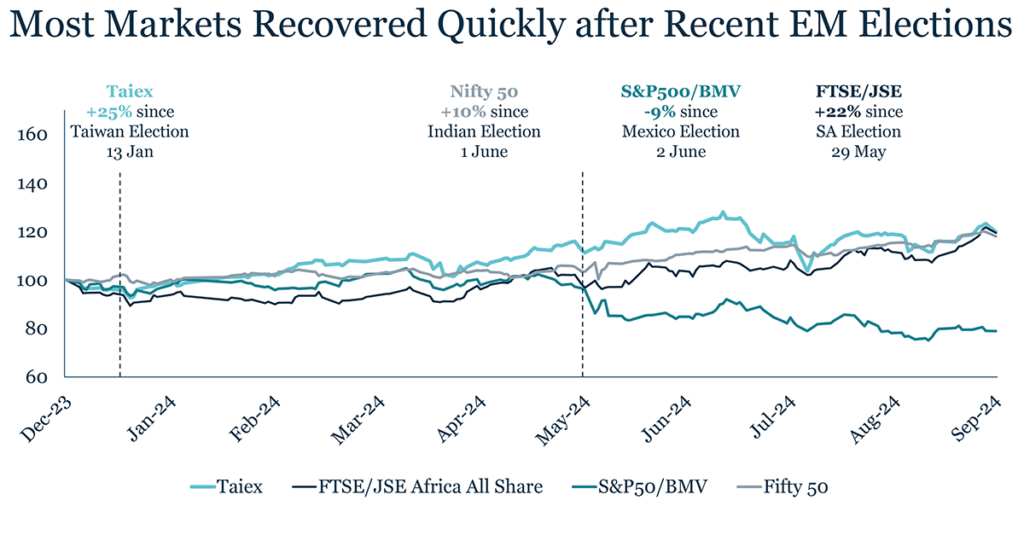

The global election year, seeing more than 60 countries and two billion people participating in elections4, has provided an additional source of volatility as uncertainty over new governments and policy directions incites investors’ fear of the unknown. However, most of the elections in emerging markets this year have not led to significant long-term spikes in volatility as the results have largely maintained the status quo in government policy. While initial declines in equity markets were mostly brief and quickly reversed (Mexico being one exception) some elections have even reduced local market volatility, with South Africa being a good example.

The US election remains a major source of uncertainty, more so than local EM elections, and will probably cause short-term market fluctuations in the lead up. However, historically, volatility tends to decline after the election announcement as uncertainty is reduced and, in fact, the MSCI EM Index often shows positive performance in the 100 days following the election announcement. The long-term impact of the new government’s policy direction, particularly on the strength of the USD and foreign policy, is what is most crucial for emerging markets. Donald Trump has perhaps been a more vocal proponent of protectionism, proposing extreme measures, including minimum tariffs of 60% on Chinese goods, 10% tariffs on global imports and, most recently, 100% tariffs on countries that turn from the US dollar. However, Joe Biden has retained and expanded many of the tariffs implemented by Trump during his presidency, reflecting a rare area of agreement between the two adversaries and a broader US shift towards de-globalisation and protectionism. Given Kamala Harris’s role as Vice President in implementing and expanding key protectionist policies such as the Inflation Reduction Act (2022) and the CHIPS and Science Act (2022), significant changes in trade policy may not be expected if she takes office.

Source: Bloomberg, figures are calculated from the first trading day after each country’s final election to 30 September 2024.

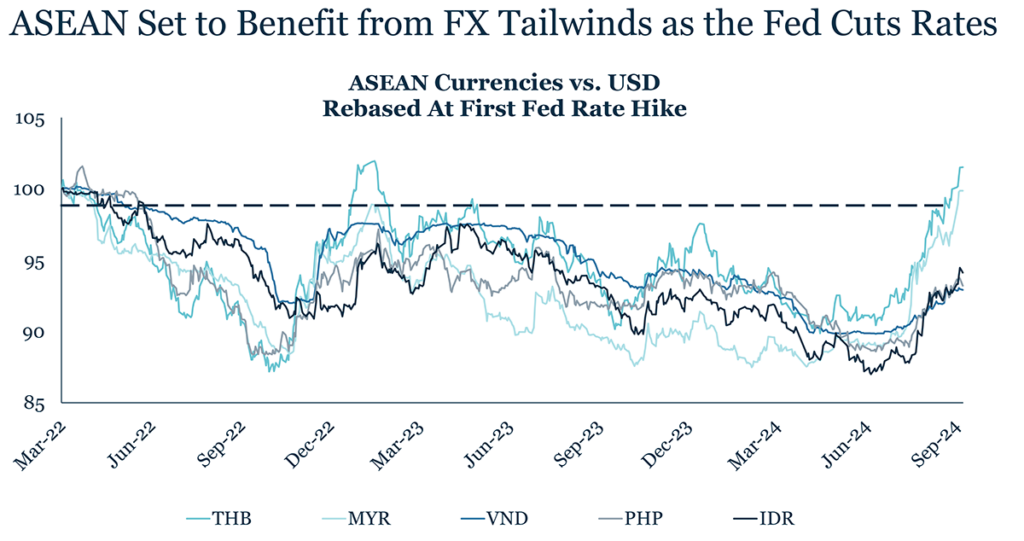

As a result, we expect friend shoring and nearshoring to continue driving capital into regions like Mexico and ASEAN, particularly in their manufacturing sectors. Additionally, the US’s decoupling from China is likely to strengthen ties with allies such as Taiwan and South Korea for semiconductor chips, and with South American and Eastern European countries for raw materials such as lithium, benefiting these emerging markets’ respective industries.

Geopolitics and Volatility

Geopolitics has long been, and is likely to remain, a significant source of volatility in global equity markets. No market, whether developed or emerging, is immune to the impacts of geopolitical events such as trade wars, ongoing conflicts or rising regional tensions. We believe the key to navigating these shocks, much like economic crises, is to stay disciplined by continuously monitoring the situation, staying informed and revisiting and reconfirming every single investment case as circumstances evolve. A disciplined macro-overlay is essential in emerging market investing, even for bottom-up stock pickers like ourselves. This approach has allowed us to effectively navigate and mitigate risks associated with major geopolitical events. For instance, we had no exposure to Russia during its invasion of Ukraine, driven by concerns over governance issues and the regulatory environment.

We closely monitor the relationship between China and Taiwan and believe that China will continue to focus on its own economic priorities in the near future, such as the overcapacity in the property market and high unemployment levels, and the recent measures to boost the economy seem to confirm this. Meanwhile, our exposure to Taiwanese companies is limited to asset-light businesses or those with a well-diversified global production base, providing some downside protection in the event of an escalation.

Conclusion: Stay Calm and Carry On

The bottom line is to stay disciplined and maintain a long-term perspective as markets tend to mean revert. Therefore, we believe by focusing on quality fundamentals rather than short term trends, volatility can be more effectively managed and even leveraged. In addition, falling interest rates have put EM back on the table as an attractive investment case for many, but we believe it is important to optimise EM investments via under-covered and mispriced small and mid-cap companies that will benefit from growing trends, such as AI, renewables and the growing consumer and middle classes, as well as diversifying your portfolio beyond the most concentrated stocks.

We are pleased to announce that the Mobius Investment Trust has been nominated in the Global Emerging Markets category at the Citywire Investment Trust Awards 2024.

We are delighted to share that the Mobius Investment Trust has been shortlisted in the Emerging Markets category for Investment Week’s Investment Company of the Year Award 2024.

In the fifth episode of Insiders and Outliers, we dive into navigating market volatility in the wake of this August’s spike. MCP’s portfolio manager and founder, Carlos Hardenberg, shares insights from his decades of experience investing through major crises including the Asian financial crisis, the dotcom bubble, and the global financial crisis. We explore how volatility can present opportunities in undervalued companies, and examine the effects of interest rates, geopolitical risks, and currency fluctuations on market instability. Listen to the latest episode via the link below or on Spotify, Apple Podcasts and Soundcloud.

We would be delighted if you would join us for the Mobius Capital Partners Investor Day 2024 on Wednesday, 25 September, at 11am (BST) at the Royal Society of Chemistry, Burlington House, Piccadilly, London W1J 0BA. This will be an in-person event with the option to join via Zoom. The investor day coincides with the Mobius Emerging Markets Fund and Mobius Investment Trust reaching their 6-year track records.

On this occasion, the founding partner, Carlos Hardenberg, and the MCP team, will reflect on the six years since inception and provide an update on the portfolio, strategy and performance of the Mobius Emerging Markets Fund and the Mobius Investment Trust. Portfolio companies CLASSYS and 360 ONE WAM will present their respective businesses, provide an outlook for the coming years and talk about their progress on ESG+C® efforts and their involvement and engagement with the Mobius Capital Partners team.

The Companies

Our Korean portfolio company CLASSYS is a global leader in nonsurgical painless fat reduction and fat freezing instruments with a 30% market share excluding the US, is poised for long-term growth. Renowned for its innovative technologies, CLASSYS also offers a comprehensive range of skincare and beauty products. As demand for non- invasive aesthetic solutions rises, CLASSYS continues to expand its market presence and enhance its product lineup, solidifying its position in the medical aesthetics industry.

Indian wealth manger 360 ONE WAM is a leading Indian financial services provider, offering specialized solutions in wealth and asset management. Its Wealth Management division provides advisory services, equity and debt broking, estate planning, and management of financial products, while its Asset Management division focuses on managing pooled funds.

The Speakers

Carlos Hardenberg

Carlos Hardenberg is the founder of Mobius Capital Partners and has been Portfolio Manager of the strategy since inception in 2018. Carlos spent 17 years with Franklin Templeton Investments starting as a research analyst based in Singapore, focusing on South East Asia. He then went on to live and work in Poland before moving to Istanbul, Turkey for ten years. Carlos has spent extensive time travelling in Asia, Latin America, Africa and Eastern Europe researching companies and identifying investment targets.

He managed country, regional and global emerging and frontier market portfolios and was appointed lead manager of the LSE-listed Templeton Emerging Market Trust PLC in 2015. Carlos successfully managed the fund and generated significant outperformance over the entire period of his leadership. He also established and managed one of the largest global frontier market funds for a decade.

Seung Han Baek

Seung Han Baek is the CEO of CLASSYS. His career has spanned over two decades in the healthcare and medical devices industry. He began his professional journey at Bayer HealthCare in 1999, where he served as a Business Unit Manager until 2005. Since then he has held high level positions at Abbott, SK Telecom, Korea Medical Devices Industry Association, and Beckman Coulter Diagnostics. Seung Han Baek has served as the CEO of CLASSYS since April 2022.

Anshuman Maheshwary

Anshuman Maheshwary is Chief Operating Officer at 360 ONE WAM. He is responsible for designing and implementing business strategies, as well as setting comprehensive goals for performance and growth.

Anshuman brings with him more than 20 years of experience. He had been with A.T. Kearney since June 2001 and was last designated as Partner and Lead, Energy & Process Industries. Here, he was responsible for senior client relationship development & management and driving high impact programs across all areas on the CEO agenda.

If you would like to attend or dial into the investor day, or have any further questions, please email anna@mcp-em.com. We look forward to welcoming you to this special event.

In the fourth episode of ‘Insiders and Outliers’, Carlos Hardenberg, founder and portfolio manager of MCP, goes beyond the hype surrounding Gen-AI to explore its potential for delivering sustainable returns and making a truly meaningful impact on our lives. He explains the critical role that emerging markets play in the Gen-AI ecosystem, highlighting various portfolio companies that are leveraging and benefiting from Gen-AI advancements, including MCP itself!