On 9 June 2026, MCP Emerging Markets hosted a Zoom webinar where founding partner Carlos Hardenberg and investment analyst Swati Mehta discussed the current investment landscape and opportunity set in India, drawing on insights from the team’s recent research trip to the country.

Carlos shared on-the-ground observations from meetings with company management teams, industry participants and local market experts, as well as outlining two current Indian portfolio companies, Groww and Aditya Infotech.

The video below is a replay of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.

Carlos Hardenberg features on a full episode of Killik and Co’s Investor Insights Podcast with Gordon Smith. Carlos reflects on MCP’s differentiated investment approach and the evolving opportunity set in emerging markets, highlighting how structural shifts, particularly in AI and market leadership, are creating new winners. He discusses the resilience of EM despite geopolitical risks, including Iran, shares insights from a recent research trip to India, and emphasises the importance of active stock selection and corporate engagement. The conversation also covers where MCP is finding high-conviction opportunities today, alongside a balanced view on risks and portfolio positioning.

In a recent interview with Das Investment, Carlos Hardenberg shares his perspective on why resilience across emerging markets continues to strengthen, driven by deeper global integration and sustained investment in innovation and R&D.

He highlights the importance of focusing on high-quality, often overlooked companies that are globally competitive and benefiting from structural trends such as AI infrastructure growth. He also discusses the key drivers behind recent fund performance, particularly mid-sized technology companies experiencing strong demand and order momentum.

Carlos further outlines why he remains constructive on India despite elevated valuations, pointing to robust economic growth, improving talent dynamics, and expanding capital markets. In contrast, he takes a more cautious stance on China due to governance and shareholder alignment considerations, favouring indirect exposure through companies operating there.

Carlos von Hardenberg kommt zu Drescher & Cie und erinnert sich zusammen mit uns anlässlich des Todes des großen Schwellenländer-Fondsmanagers Dr. Mark Mobius an den Menschen, die Persönlichkeit, den Investor und sein Vermächtnis für die Nachwelt. Aus unserer Sicht ein gleichermaßen einfühlsames wie lehrreiches Gespräch für Anleger.

We are deeply saddened to learn of the passing of Mark Mobius.

Mark was not only one of the founders of MCP, but also a cherished mentor, partner, and source of inspiration to all of us. His influence on the emerging markets investment landscape was extraordinary, and his vision helped shape both our firm and the industry more broadly.

Until his retirement from the company in 2023, he remained a guiding presence and a passionate ambassador for MCP. His wisdom, energy, and generosity left a profound and lasting impression on everyone who had the privilege of working with him.

We will remember Mark not only for his remarkable achievements, but also for his character, his guidance, and the enduring impact he had on our lives. He will be greatly missed, and we hold his memory with deep respect and gratitude.

Carlos Hardenberg joins Jonathan Davis, host of the Money Makers Podcast and editor of the Investment Trusts Handbook (winner of the AIC Best Broadcast Journalist You Award 2024 and 2025), to discuss – amongst other things – the ongoing impact of the Iran War on financial markets and the investment trusts sector.

On 10 March 2026, MCP Emerging Markets hosted a Zoom webinar where founding partner Carlos Hardenberg and investment analyst Swati Mehta provided an update on the strategy, performance and portfolio of the Mobius Emerging Markets Fund (MEMF) and the Mobius Investment Trust (MMIT), as well as providing an in-depth review of their insights from a recent research trip to India.

The video below is a replay of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.

MCP wishes everyone a prosperous Chinese New Year as we are now over a week into the Year of the Fire Horse, a “Double Fire” combination symbolising energy and volatility.

In markets, “fire” could either symbolise a continuation of last year’s blistering rally or a crash and burn. Reflecting on China’s performance last year, the market appeared driven more by sentiment and liquidity injections than by earnings growth or fundamental re-ratings. The Fire Horse also symbolises independence, a theme likely to remain central to China’s strategic direction, particularly in the technology sector amid increased geopolitical tensions with the US.

The last year of the Fire Horse in 1966 stands as one of the most volatile, defining, and ultimately tragic periods in China’s modern history, marked by the beginning of the Cultural Revolution. The movement was launched by Chinese Communist Party Chairman Mao Zedong, with the stated goal to preserve communism and purge those “who have followed the path of capitalism”. Beyond the profound human tragedy, with an estimated 2 million lives lost, the revolution caused a severe economic contraction as industrial production, agriculture, and the education system were all majorly disrupted by the social and political turmoil.

China has since undergone extraordinary transformation becoming the world’s second-largest economy and home to some of the largest capital markets, such as the Shanghai Stock Exchange, only opening in 1990.

As we enter the Year of the Fire Horse, 2026 reflects the continued structural rebalancing of China’s growth drivers. GDP growth is projected at around 4.5%, with export momentum moderating and the property sector remaining a drag, albeit a diminishing one. Domestic activity is expected to remain broadly resilient, supported by measured policy actions and ongoing expansion in innovation-driven sectors. At the same time, uncertainties surrounding trade and technology policies, the trajectory of the property adjustment, and global macro conditions may contribute to continued market volatility. In this environment, a disciplined and selective approach remains warranted.

Carlos Hardenberg features on AJ Bell’s Money and Markets Podcast. Carlos speaks about dealing with political turmoil in emerging markets, and how he safeguards investments from it.

In contrast to previous years, when MEMF delivered strong returns driven by small- and mid-cap emerging market companies despite broader EM equities lagging, the asset class entered a recovery phase in 2025. Emerging markets demonstrated to global investors that they can deliver strong returns in a market previously dominated by American exceptionalism.

However, the benefits were largely captured by a small number of mega-cap stocks, resulting in unusually narrow market leadership. While gains have been highly concentrated so far, a broader set of supportive dynamics for emerging markets should increasingly extend beyond the largest stocks and benefit quality small- and mid-cap companies.

At the same time, many of our holdings have continued to execute well operationally, but this has not been fully reflected in share prices due to macroeconomic headwinds. As these pressures ease, we see scope for a catch-up in valuations, providing support to the portfolio in the years ahead.

Emerging Markets Supported by Numerous Tailwinds

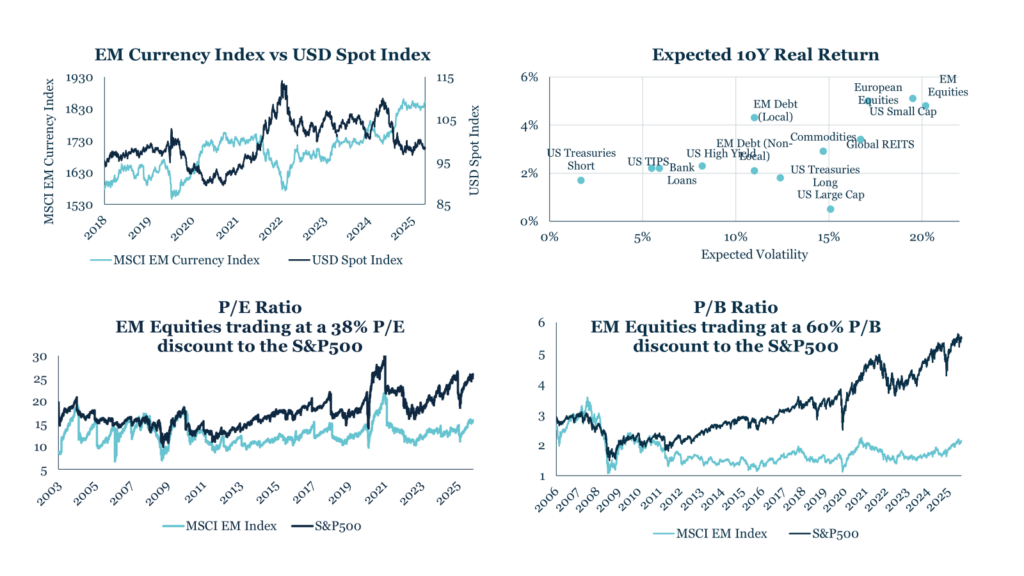

At year end, emerging markets were trading at a 38% discount on a P/E basis and a 60% discount on a P/B basis relative to developed markets. These valuation gaps are particularly pronounced in the sectors we focus on, such as technology and consumer discretionary. Importantly, the attractive discounts noted above are also increasingly evident across quality stocks, extending beyond traditional value segments.

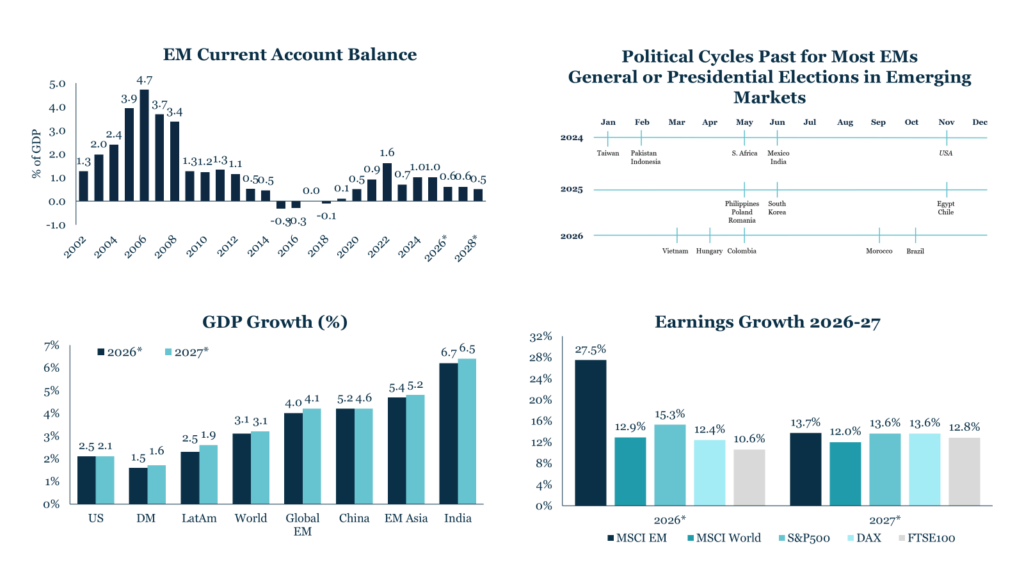

Furthermore, emerging markets are supported by a 9.4% weakening of the US dollar in 2025, which is expected to continue into 2026. This typically benefits EM currencies, with the Brazilian real, Colombian peso and Taiwanese dollar among the strongest performers this year. Emerging markets continue to maintain healthier debt levels than developed markets (69% versus 109% of GDP in 2024), while simultaneously offering stronger GDP and earnings growth projections.

Higher Growth in EMs Combined with Healthier Debt Levels

Source: IMF WEO October 2025, Bloomberg. * indicates forecast.

Political risk related to elections is lower this year, with major electoral events in 2026 limited to Vietnam and Brazil across our key markets. However, geopolitical risks more broadly remain elevated. Recent developments, including tensions between the US and Europe over Greenland and events in Venezuela, have already added complications to the outlook for 2026, alongside long-standing risks such as the Russia–Ukraine conflict, instability in the Middle East, global trade wars, and ongoing tension between China and Taiwan. We remain highly mindful of geopolitical risks and always apply a macro risk overlay to our bottom-up stock selection.

The Federal Reserve’s expected rate cuts this year further enhance the outlook, as lower US yields generally push investors toward higher-return emerging market assets—particularly as many EMs benefit from moderating inflation and higher real rates themselves. While effects may vary across countries, the global easing cycle provides a broadly supportive backdrop for EM performance.

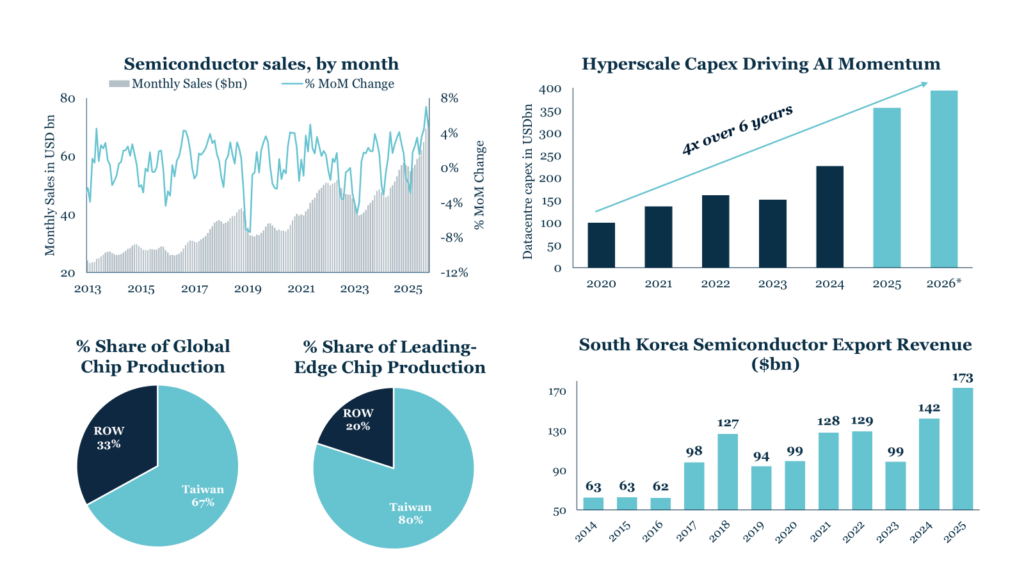

Furthermore, a number of country-specific tailwinds should support our portfolio exposures. Taiwan continues to benefit from a powerful semiconductor investment cycle and a globally competitive innovation ecosystem. South Korea is advancing structurally in high-end manufacturing, materials and automation, where we continue to find globally competitive businesses trading at attractive valuations.

Taiwan and Korea Well Positioned in Semiconductor and AI Markets

Source: Statista, Semiconductor Industry Association, Bloomberg, Economic Times, South Korea Ministry of Trade. * indicates forecast. Data as of 31 December 2025.

Despite a challenging start to 2026, marked by foreign outflows amid reduced risk appetite and heightened macro volatility following recent geopolitical developments, India’s longer-term outlook remains compelling. We continue to look through near-term volatility, supported by resilient GDP growth, rising discretionary consumption and improving capital expenditure trends. The year 2026 could turn into another period of significant progress for the country.

Brazil offers selective opportunities as inflation moderates, interest rates decline and corporate balance sheets strengthen. We remain cautious around the upcoming elections, which are likely to introduce additional volatility in 2026.

While emerging markets have delivered strong headline returns this year, dispersion beneath the surface has been significant. With valuation spreads at elevated levels and earnings revisions diverging meaningfully by country, sector and company, passive exposure increasingly reflects index concentration rather than the breadth of opportunity available.

In this environment, disciplined bottom-up stock selection is essential to identifying structurally stronger businesses beyond benchmark heavyweights. We believe the portfolio is well positioned should the recovery broaden into under-owned areas of the market where fundamentals remain intact.

With a portfolio built around high-quality, lesser-known companies and a disciplined, active approach to capital allocation, we remain fully committed to our investment philosophy and to delivering long-term performance and shareholder value.