On 18 March 2025, MCP Emerging Markets hosted a Zoom webinar where founding partner Carlos Hardenberg and investment analyst Swathi Seshadri provided an update on the strategy, performance and portfolio of the Mobius Emerging Markets Fund (MEMF).

The video below is a replay of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.

Portfolio Manager, Carlos Hardenberg, and the MCP team are currently on-the-ground in Taiwan. So far, they have had company meetings with:

All of MCP’s Taiwanese holdings

Foundries

IC design houses, incl. ASIC

Silicon IP

Server assemblers

Material & component manufacturers

Private companies looking to IPO soon

Here are some key facts about the country that we find particularly interesting:

Semiconductor Industry:

1. TSMC held a 64.9% share of global semiconductor foundry revenue in Q3 2024, a 12% YoY increase. Including other foundries, Taiwan’s total market share surpassed 72%, up 9% YoY1.

2. The global semiconductor market has experienced significant growth, nearly doubling over the past decade. According to Gartner, revenues reached $626 billion in 2024, with forecasts predicting an increase beyond $700 billion in 20252.

Taiwan’s Economy:

3. Taiwan’s GDP grew by approximately 4.3% in 2024, bringing per capita GDP to around $34,000. Economic growth is projected to continue at a rate of 3.1-3.3% in 20253.

4. Taiwan’s government debt-to-GDP ratio has steadily declined over the past decade, standing at 26% in 2024. In comparison, the U.S. debt-to-GDP ratio exceeds 120%4.

Taiwan’s Trade:

5. Taiwan’s exports surged by 32% YoY in February 2025, marking the strongest growth since February 20225.

6. In 2024, Taiwan recorded a net trade surplus of $80 billion6.

7. Despite geopolitical tensions, Taiwan and China maintain robust trade relations and FDI flows. China remains Taiwan’s largest trading partner, although Taiwan ran a $70 billion trade surplus with China in 20247.

More Facts!

8. Taiwan is recognised as a highly liberal and democratic nation, with a score of 94/100 in the Freedom House rankings8.

9. Taiwan is officially recognised by only 12 countries, most of which are small island nations9.

10. Taiwan has four official languages and over 20 living languages.

Footnotes:

1 Statista

2 Gartner

3 Statista

4 IMF

5 Trading Economics

6 Statista

7 Statista

8 Freedom House

9 Ministry of Foreign Affairs, Republic of China (Taiwan)

On the occasion of Women’s Day, celebrated on March the 8th, RankiaPro take a look at how the sector is evolving and how we are all making an effort to achieve greater gender parity, collecting the testimonies of three leading female professionals in the industry, including our Head of Investor Relations, Anna von Hanh, along with Maxime Carmignac and Rose Ouahba from Carmignac.

Anna’s Testimony:

My journey into finance was anything but typical. After 15 years in book publishing, I made the leap into the financial world—a shift that quickly revealed stark gender disparities between industries. For over a decade, I attended the Frankfurt Book Fair, where, based on my own observations, women seemed to make up around 80% of people working there. Now, instead of strolling through the book fair, I find myself traveling just 70 kilometers further to a finance fair in Mannheim, where the ratio appears exactly reversed. The contrast made me question why finance remains so male-dominated and what can be done to change that.

For generations, women have been underrepresented in finance. Girls are less frequently introduced to financial topics, and societal expectations continue to influence career choices. Many women gravitate toward creative (often less well paid) industries, possibly not only out of preference but also due to ingrained perceptions that men should be the primary earners. Meanwhile, men face pressure to pursue high-paying roles, reinforcing a gender imbalance in finance and investment.

A bias within the industry might be compounding this disparity. A 2021 CFA Institute study found that over three-quarters of women in investment believe the field is biased toward men, particularly in recruitment, promotions, and workplace culture. Addressing this requires systemic change, starting with early financial education. All schools should introduce finance and investment topics to both boys and girls, and women in the industry should be visible role models to inspire the next generation.

Even within finance, women are more commonly found in marketing and client relations rather than investment roles, further limiting women’s influence in financial decision-making. Yet, research shows that diverse teams make better decisions. Studies indicate that investment teams in the top quartile of gender diversity outperform those in the bottom quartile by 45 basis points annually. Despite this, only 12.5% of global fund managers are women, a figure that has barely changed in the past decade.

I have observed that women in finance tend to question themselves more, which can sometimes be seen as a lack of confidence. However, I believe, in investing, this self-reflection is an asset—it encourages deeper analysis, continuous reassessment, and a more balanced approach to risk. I have seen cases where overconfidence led to emotional attachment to an investment thesis, preventing rational decision-making. Encouraging diversity in investment teams fosters a broader range of perspectives, better risk management, and ultimately stronger performance.

At MCP, we are fortunate to have a 50/50 gender split within the team, and in my experience, this dynamic works exceptionally well. Yet, challenges persist—women still bear more childcare responsibilities, impacting career progression. While outsourcing is an option, many prefer to be present, particularly as children face growing digital distractions.

The COVID-19 pandemic briefly reshaped workplace dynamics, providing more flexibility. However, the recent push back to office-based work risks reversing this progress, making it harder for women to balance work and family. Companies that embrace flexibility will retain more skilled professionals, fostering a more diverse and resilient workforce.

Progress has certainly been made, but there’s still a long way to go. In some parts of the world, we’re even seeing signs that gender equality could be slipping backward. I truly hope that’s not the case—for the sake of my daughter and her generation. The future of finance will be stronger, more innovative, and more resilient with women fully included.

During my recent visit to South Korea, not only did I experience extremely cold weather conditions, but I also witnessed the nation navigate through significant political turmoil following the impeachment of President Yoon Suk Yeol over his declaration of martial law on 3 December 2024. The Constitutional Court concluded its final hearing on 25 February 2025, and a verdict is anticipated in mid-March. Concurrently, President Yoon faces a criminal trial on insurrection charges, which commenced on 20 February 2025. The main opposition Democratic Party is led by Lee Jae-myung, who narrowly lost the 2022 presidential election to Yoon and is now a prominent figure in the political landscape.

Despite the political uncertainty, the situation on the streets remained calm. I witnessed protests that were peaceful, well-organised, and did not create any fear or disruption to daily life.

During my stay, I visited over 30 companies across the consumer, healthcare, semiconductor, and technology sectors, including our portfolio companies, where we had excellent interactions and came away with a positive outlook for 2025, as well as exploring new investment ideas.

Since our inception, there has rarely been a dull moment, and 2024 was no exception. While a global election year would naturally bring a degree of unpredictability, many of the year’s most significant surprises and sources of volatility stemmed from elsewhere, ranging from speculation around rate cuts and tech-driven market movements to Chinese stimulus measures— alongside the backdrop of the US election.

Amidst the turbulence, one of the more encouraging developments has been the ability of several developed and emerging markets to successfully steer towards what appears to be a soft landing, accompanied by the gradual (albeit occasionally uneven) normalisation of global inflation. While some fluctuations may still occur, the overall trend of easing inflation pressures, with only a few exceptions, seems clear.

For the MCP team, 2024 was a productive year, marked by extensive research trips to key markets resulting in several new additions to our portfolio. In-person meetings with companies, their competitors, local experts, politicians and economists inform our deep understanding of companies, and are an invaluable tool for conducting due diligence on investment ideas.

During these conversations and in follow-ups afterwards, we received positive updates from several companies in our portfolio that confirm our outlook. For example, Elite Material, a leading producer of semiconductor materials, is preparing to supply its upgraded M8 material for a US cloud service provider’s ASIC (Application-Specific Integrated Circuit) in 2025, addressing the growing demand for AI processing and the need for customised solutions over NVIDIA’s GPUs (Graphics Processing Unit). Similarly, Chroma has developed a unique device for its foundry client’s advanced packaging processes, ensuring precise alignment of stacked chip components, an essential capability for manufacturing next-generation AI chips.

Over the year, MEMF was able to generate robust outperformance returning 5.4% (Private C USD Founder) and 11.9% (Private C EUR Founder). In Q4, MEMF returned -2.3% (Private C USD Founder) and 5.0% (Private C EUR Founder), outperforming the benchmark (MSCI EM Mid Cap Index Net TR) by 6.5% (USD) and 7.0% (EUR) respectively.

The final quarter of 2024 has largely been defined by Donald Trump’s election victory, prompting businesses and governments worldwide to prepare for the implications of his second presidency. Additional key developments influencing emerging markets this quarter include the Fed’s second and third rate cuts of the year, the South Korean president’s controversial attempt to impose martial law, and the announcement of further stimulus measures in China aimed at bolstering economic growth.

Donald Trump’s landslide victory and Republican control of Congress mark a pivotal shift for the US and global markets. While US equities and the dollar have strengthened in response, emerging markets face a more uncertain outlook due to Trump’s aggressive tariff rhetoric. Yet, as Einstein suggested, within difficulties lie opportunities. Countries like India, Indonesia and Vietnam, are already benefiting from the “China+1” strategy and appear well-positioned to attract new manufacturing investments. Their competitive labour markets, improving infrastructure and supportive government policies make them increasingly appealing, as companies seek to diversify supply chains and reduce dependency on China. At the same time, the US’s heavy reliance on imports, particularly from China, reduces the likelihood of sweeping tariffs, which could risk significant domestic disruption. Nevertheless, Trump’s track record and rhetoric on trade raises the possibility of bold policy shifts that may reshape global trade dynamics in the years to come.

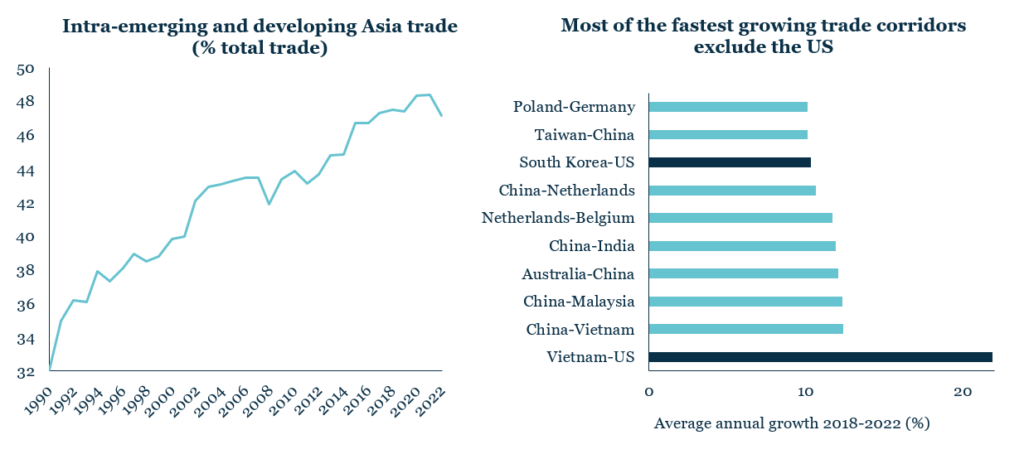

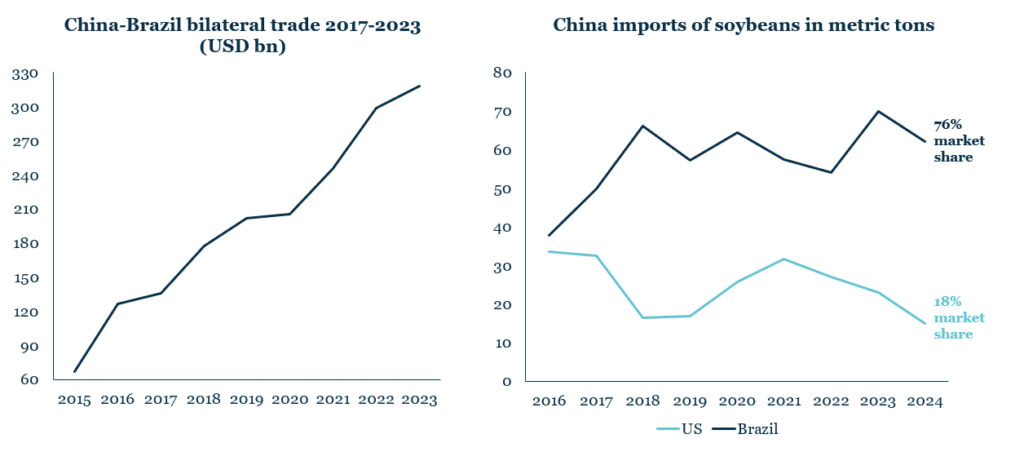

Emerging markets have previously responded to the above dynamics with increased trade diversification and reduced reliance on the US dollar. During the 2018 trade war, for example, China shifted imports like soybeans to Brazil, a move that fuelled record bilateral trade. This pattern could reemerge under Trump’s renewed tariff threats.

Rising Intra-EM Trade Reduces Dependence on US Trade

Source: Asia Regional Integration Centre, Economist Impact calculations, Financial Times. As of 31 December 2024.

Additionally, nations such as India are advancing local currency trade agreements, fostering resilience against external shocks. Intra-EM trade, particularly within Asia, set to rise from $4.3 trillion in 2023 to $7.1 trillion in 2030 (HSBC Forecast), has also grown significantly and is poised to accelerate further, offering emerging markets the chance to deepen their autonomy and global influence.

Brazil-China Trade Grows as China Diversifies from the US

Source: Reuters, Statista. As of 31 December 2024.

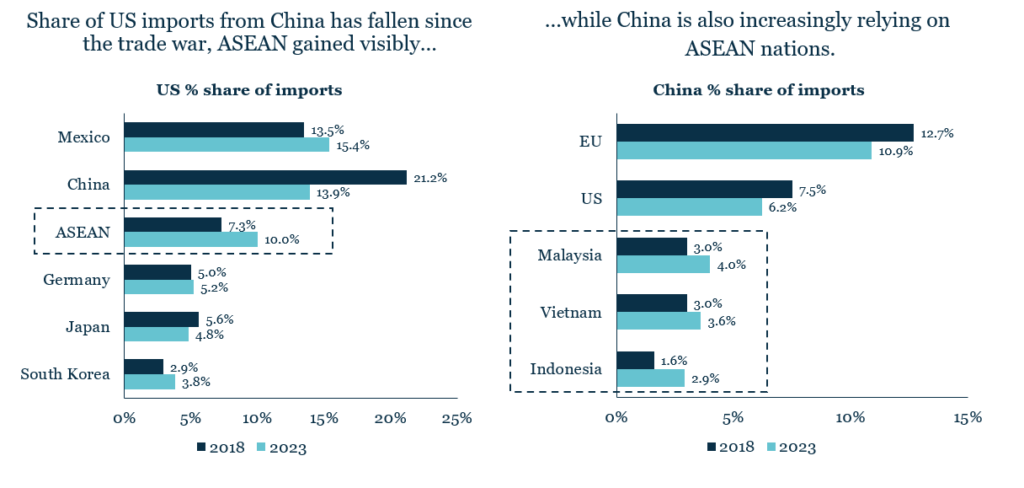

ASEAN Macro

Source: Maybank Research, Bloomberg, local sources. As of August 2024

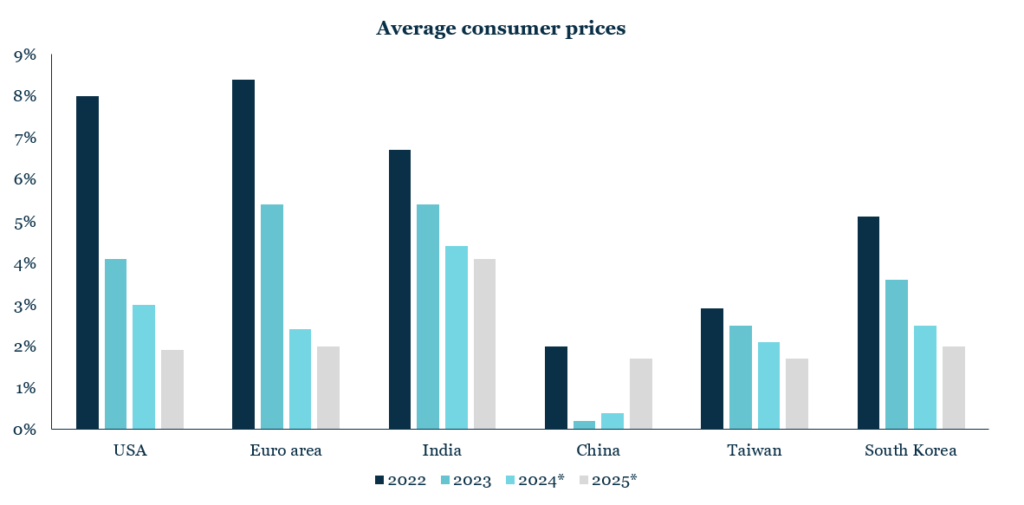

Monetary policy adds another layer to this evolving landscape. Inflation has moderated over the past year, following the Federal Reserve’s earlier rate hikes. This had created room for monetary easing in 2024, with a cumulative 75bps rate cut signalling a shift in policy. However, the strength of the US economy may slow the pace of future reductions, even if the overall direction seems clear. Lower rates provide emerging market central banks with room to ease monetary policy, enabling cheaper borrowing, improved consumer sentiment and increased corporate investment. At the same time, local conditions remain pivotal. Brazil, for example, continues to raise interest rates to combat inflationary pressures. Nevertheless, we believe the country still holds attractive long-term opportunities, particularly in quality companies with strong fundamentals.

Global Inflation is Normalising

Source:IMF WEO October 2024, * indicates forecast

China, meanwhile, continues to grapple with significant economic challenges of its own, including its property sector crisis, weak consumer sentiment, and deflation. Recent stimulus measures, including a $1.4 trillion plan to address hidden debt and monetary easing, have provided only short-term relief. However, deeper structural reforms remain essential. The Politburo’s efforts to boost domestic demand and stabilise the property sector are positive signals, particularly in light of potential US tariff increases, but caution remains warranted.

Geopolitics remains an ongoing risk, with tensions in the Middle East, the Russia-Ukraine war, and China-Taiwan relations posing significant challenges. Our disciplined macro-overlay has been instrumental in navigating these complexities. This approach will remain central as we navigate 2025. On the positive side, Trump’s leadership may offer the potential to de-escalate conflicts and foster peace negotiations—a trend that may already be emerging in the Middle East at the time of writing.

Taken together, these interconnected factors paint a complex picture for 2025. While risks are evident, emerging markets could leverage this period of transition to strengthen resilience, diversify trade and attract investment, positioning themselves as key drivers of global growth in the years ahead. Furthermore, emerging markets are essential for diversification, offering strong growth potential, attractive valuations and innovative companies that play a key role in global supply chains. This is particularly important as the US market, with the S&P 500 heavily concentrated in just seven companies which were accounting for around 28% of its market capitalisation at the end of 2024 and contributed over 50% of its returns during the year, poses significant concentration risks. Active investing in emerging markets allows for another layer of diversification by identifying lesser-covered companies, which may offer unique opportunities for long-term growth and the potential to outperform broader market trends.

Heading into 2025, we remain focused on our long-term strategy and the core fundamentals of our holdings. Conversations with our portfolio companies in recent months have reinforced our cautiously optimistic outlook for 2025 and beyond.

As Lunar New Year celebrations continue this week, it presents an opportunity to reassess the Chinese market. The Snake, whose symbols include wisdom, transformation, and strategy, serves as a hopeful emblem for China as it navigates ongoing structural challenges this year.

The economy remains under pressure, grappling with a property sector crisis, weak consumer sentiment, and deflation. In response, Beijing has signaled plans for further stimulus measures beyond those introduced late last year, including a $1.4 trillion plan to address hidden local debt and monetary policy easing. These are certainly positive steps but have so far provided only short-term relief. Given the depth of China’s economic challenges, which we believe will take years to resolve, more strategic and decisive action appears to be the wise course for Beijing in 2025. The upcoming annual CPPCC National Committee meetings in early March will be a key event to monitor for further announcements of potential stimulus and domestic support measures.

Beyond the New Year, there is limited cause for celebration this week as today an additional 10% tariff on Chinese imports to the US will take effect indefinitely. While this increase is lower than many anticipated, especially compared to Trump’s threats on the campaign trail, it is likely to spur market volatility as speculation grows over further tariff increases and their timing.

Beijing has said it will legally challenge the tariffs as they violate World Trade Organization rules and today announced it will impose additional tariffs between 10-15% on a basket of US imports, including, but not limited to, oil, gas, and farming equipment.

Overall, while the Year of the Snake represents transformation, we maintain our cautious outlook and underweight position in the Chinese market given the significant domestic and global challenges the country faces. Instead, we prefer indirect exposure to the country through Korean and Taiwanese companies that have better corporate governance and operate in a more stable macroeconomic and regulatory environment. However, China remains the world’s second-largest economy, with its 2024 GDP growth having meet its 5% target, outpacing most developed and even emerging markets growth. Therefore, amidst caution, we still search for exciting investment opportunities that meet our quality investment criteria.

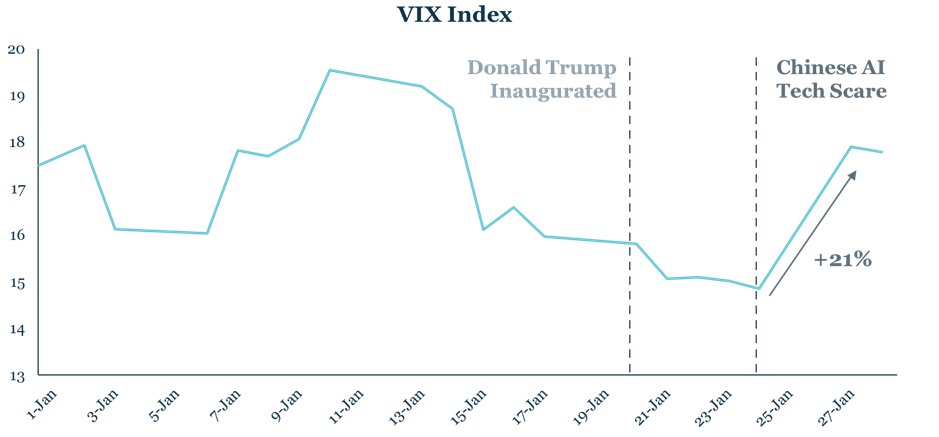

Yesterday, market volatility, measured by the VIX Index, jumped 21% from the previous trading day’s close. This spike was triggered by DeepSeek, a Chinese AI start-up, unveiling a large language model (LLM) reportedly built with just USD$6M, challenging the long-standing assumption that AI development requires vast amounts of expensive Nvidia chips. As a result, Nvidia’s share price dropped 17% on Monday with sell-offs reaching across U.S. big tech with other ‘Magnificent 7’ companies experiencing smaller, yet notable, declines.

Source: Bloomberg

This underscores the risks of a highly concentrated market where sell-offs can become more severe as many investors rush to offload the same stocks, leading to outsized losses for those who remain invested.

While the high concentration of the U.S. market is well-known, it’s less widely recognised that a similar dynamic exists in emerging markets. In the MSCI Emerging Markets Index, the top 10 companies make up roughly 25% of the total index weight despite having around 1,300 constituents. Additionally, many bulge-bracket EM funds are heavily weighted toward these top 10 names, potentially increasing their vulnerability to significant drawdowns during market sell-offs.

This highlights the importance of portfolio diversification. Instead of over-concentration in a few dominant players, MCP focuses on smaller, innovative companies in emerging markets, particularly in sectors like AI and the semiconductor supply chain as well as those catering to the global recovery in consumer demand. These are areas we believe have strong potential to generate alpha and provide long-term growth opportunities.

For the MCP team, 2024 has been a productive year, highlighted by extensive research trips to key markets which we believe provide us with a competitive edge. In-person meetings with portfolio and pipeline companies, local experts, policy makers and private equity houses have provided invaluable insights into macroeconomic and geopolitical trends, businesses’ operating conditions and corporate governance, as well as enabling in-person engagement. Additionally, in under-researched emerging markets, where stocks can be mispriced due to limited available information, these trips are essential for uncovering high-quality investment opportunities that have the potential to deliver significant alpha.

The Importance of a Strong Network

We believe the key to successful research trips lies in having a trusted and extensive network. Our 25-year network is built on Portfolio Manager Carlos Hardenberg’s decades of experience in emerging markets and complemented by the industry relationships built by MCP’s analysts throughout their careers.

We don’t expect our analysts to be experts in everything, but we do expect them to know where to access relevant information, including identifying key contacts during research trips. Building these robust networks—and leveraging the valuable insights they offer—drives our commitment to frequent research trips, which in turn, creates further opportunities to engage with local experts and businesses, continually expanding our network. We adopt a targeted approach to our research trips, customising each trip to align with the unique macroeconomic and geopolitical conditions of the region and the specific characteristics of the opportunity set. This allows us to gain a deeper understanding of both country- and sector-specific challenges. Furthermore, our priority is to visit regions where we hold a strong investment conviction and have a higher portfolio exposure, leading to the majority of our trips being concentrated in Asia.

For example, during a research trip to Greater China in Q2 2024, in Taiwan, our highest country exposure, the team prioritised meeting with portfolio companies’ management teams and actively driving engagement. When the team continued to mainland China, they focused on conducting visits to manufacturing facilities of portfolio companies with operations in the region. In contrast, when the team visited Vietnam in Q3—where our exposure is just 3%— they prioritised exploring new opportunities through meetings with pipeline companies and local experts, which ultimately led to the addition of a new holding, FPT.

Looking Beyond the Sell-Side

In today’s investment landscape, it is all too easy to believe you have all the information you need at the click of a finger. When investing in well-known highly liquid stocks, information is readily available through sell-side reports, online resources and advanced data platforms such as Bloomberg. However, the ubiquity of this information leaves little room for competitive knowledge advantage in what are highly efficient markets. Moreover, relying solely on sell-side information often overlooks the depth, nuance and context that can only be gained through on-the-ground research.

In contrast, our focus is on identifying and understanding lesser-known companies. By concentrating on mid-cap stocks in emerging markets, we operate in a universe that is often under-researched, with limited sell-side coverage, reduced visibility and minimal overlap with major benchmarks. This lack of broad market coverage often leads to mispricing, creating opportunities to generate alpha by identifying undervalued companies with strong fundamentals. However, investing in these types of unknown stocks also demands rigorous, independent, in-person channel checks. While conducting this research, our team maps the competitive landscape, evaluates total addressable market (TAM) opportunities and stays informed about sector innovation and R&D trends.

MCP Visiting Taiwanese Holdings

Therefore, for our investment strategy, conducting research trips is not just beneficial—it is essential. These trips allow us to look for hidden opportunities, gain insights that others might overlook, and capitalise on market inefficiencies with the aim to generate additional sources of alpha.

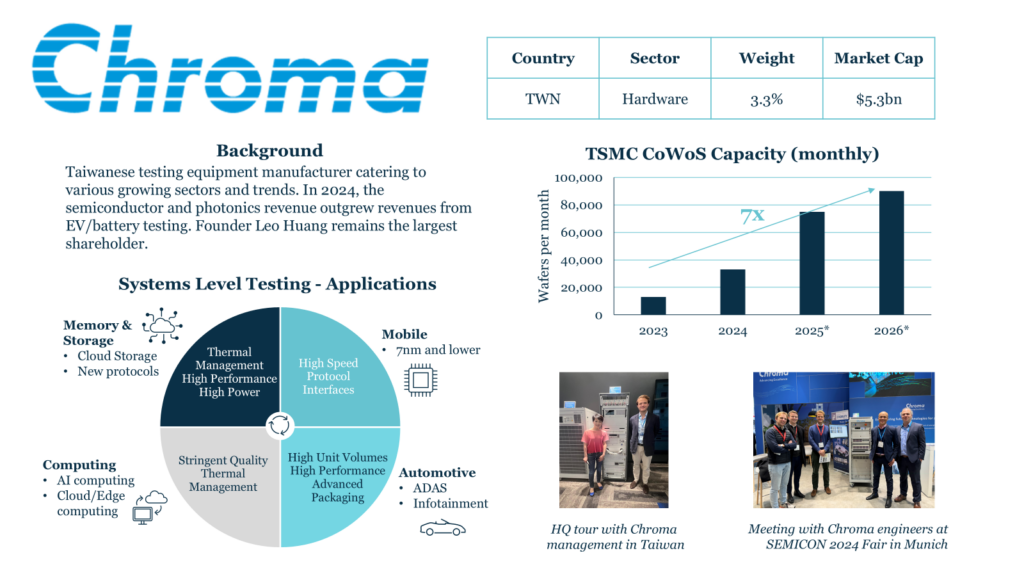

Company Case Study: Chroma

The Greater China trip in Q2 2024 exemplifies how a well-structured research trip can profoundly enhance our understanding of a portfolio company. During this trip, the team focused on Chroma, a Taiwanese equipment supplier and a recent addition to the portfolio. Spending several weeks immersed in Taiwan’s vibrant semiconductor ecosystem, the team conducted comprehensive channel checks on Chroma.

Source: Chroma, Bloomberg, CLSA

Traditionally a manufacturer of testing equipment for EV and battery applications, Chroma has leveraged its expertise in thermal management to establish a foothold in the niche market of systems-level testing for high performance computing chips (HPC).

Through formal meetings, campus tours and discussions with technical experts, MCP gained deeper insights into the demand dynamics for Chroma’s innovative products. A standout example of its innovation-driven approach is the development of a cutting-edge metrology tool designed for a leading foundry’s advanced packaging process. This breakthrough positions Chroma to capitalise on the foundry’s rapid capacity expansion, driven by the growing demand for CoWoS (Chip-on-Wafer-on-Substrate) technology as the AI/HPC boom accelerates.

Enhancing Geopolitical & Macroeconomic Insights

Over the past year, the MCP team has visited India on several occasions, Greater China— including Taiwan, Hong Kong, and mainland China—as well significant portions of ASEAN, including Vietnam, Malaysia, Thailand and Singapore. As well as providing company-specific insights, in-person visits help us to assess the broader environment and challenges that companies operate in by providing a deeply informative perspective on each country’s macroeconomic landscape and enabling us to closely monitor risks, including regulatory changes and geopolitical tensions. Based on observations from recent on-the-ground trips to Greater China, we believe that the likelihood of a Chinese invasion of Taiwan in the short term appears low, given the substantial domestic economic challenges China is currently facing. However, we continue to monitor the situation very closely.

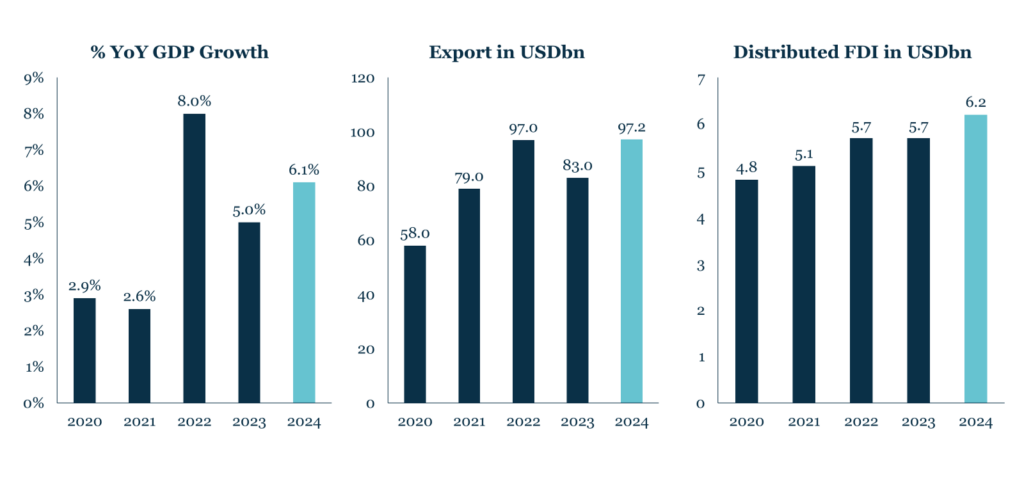

As we move into 2025, we do so with a strengthened bullish conviction in ASEAN, particularly in Vietnam, following the team’s visit to the country in September. Leveraging Carlos’ extensive network, the trip provided access to company founders, entrepreneurs, local private equity leaders, government officials, former colleagues and numerous businesses. The team also visited a local tech university and even test-drove the new VinFast car through the streets of Hanoi.

These meetings and conversations, combined with Carlos’ two decades of experience traveling to Vietnam, highlighted the country’s remarkable pace of technological innovation and transformation—an insight that stood out as the trip’s primary takeaway. Everyday observations further reinforced this perspective, from the widespread use of Grab (Asia’s version of Uber) as the primary mode of transportation, to seamless digital payments via Apple Pay.

MCP visiting Vietnam

Other key takeaways highlighted Vietnam’s impressive, world-class infrastructure—spanning airports, roads, and bridges — a business-friendly government, and significant strides in corporate governance. Collectively, these factors reinforced our optimistic view of the country’s strong growth trajectory, which we believe will support its transition to emerging market status.

Opportunities in ASEAN: Example Vietnam

Source: Maybank Research, Bloomberg, local sources, IMF WEO October 2024, FT, Export and FDI figures as of Q2 of each year

While we are excited about opportunities in Vietnam, our core convictions remain in India, Taiwan and South Korea. Research trips to these regions have reinforced our convictions, highlighting the innovation of local companies, strong corporate governance practices and supportive macroeconomic environments. India’s well-educated, youthful population supports long-term growth, while Taiwan and South Korea lead in innovation, particularly in tech sectors such as AI, 5G and renewable energy, where we favour asset-light, IP-based businesses.

Although South Korean President Yoon Suk Yeol shocked the nation and global investors with his failed attempt to impose martial law in December, we believe the Constitutional Court’s decision to impeach Yoon, leading to his arrest in January 2025, highlights the strength of the country’s democratic framework which will allow the country to focus on its economic potential. Fundamentally, we remain confident in the country’s stability and its promising investment opportunities, particularly in the export market.

Conclusion

In 2025, the team is excited to continue these on-the-ground research trips to both familiar and unfamiliar markets. Trips already planned include India, Taiwan and Latin America, with additional trips to follow later in the year. These visits will allow MCP to conduct in-depth channel checks on portfolio companies, perform rigorous due diligence on pipelines companies, stay attuned to evolving macroeconomic and geopolitical trends, and conduct in-person engagement.

Donald Trump’s inauguration yesterday following his landslide victory marks a pivotal shift for U.S. and global markets. While U.S. equities and the dollar have strengthened in response, emerging markets face a more uncertain outlook due to Trump’s aggressive tariff rhetoric.

Yet, within challenges lie opportunities. Countries like India, Indonesia, and Vietnam, for example, are already benefiting from the “China+1” strategy and appear well-positioned to attract new manufacturing investments. Their competitive labour markets, improving infrastructure, and supportive government policies make them increasingly appealing as companies seek to diversify supply chains and reduce dependency on China.

At the same time, the U.S.’s heavy reliance on imports, particularly from China, reduces the likelihood of sweeping tariffs, which could risk significant domestic disruption. Trump refrained from threatening immediate tariffs on China in his first days in office, and even spoke by phone with President Xi Jinping just days before his inauguration, suggesting that tariffs on China could be more moderate than Trump advocated on the campaign trail. Nevertheless, Trump’s past track record and rhetoric on trade raises the possibility of bold policy shifts that may reshape global trade dynamics in the years to come.

Emerging markets have previously responded to the above dynamics with increased trade diversification and reduced reliance on the US dollar. During the 2018 trade war, for example, China shifted imports like soybeans to Brazil, a move that fuelled record bilateral trade. This pattern could reemerge under Trump’s renewed tariff threats.

Additionally, nations such as India are advancing local currency trade agreements, fostering resilience against external shocks. Intra-EM trade, particularly within Asia, has also grown significantly and is poised to accelerate further, offering emerging markets the chance to deepen their autonomy and global influence.

Overall, while risks are evident, emerging markets could leverage this period of transition to strengthen resilience, diversify trade, and attract investment, positioning themselves as key drivers of global growth in the years ahead.