On 24 June, the Mobius Investment Trust portfolio manager Carlos Hardenberg hosted a webinar on Investor Meet Company to help retail investors better understand the opportunities within emerging markets, as well as outlining MMIT’s differentiated approach to generating long-term capital growth across emerging markets.

Despite a volatile macroeconomic environment, the Trust maintains high conviction in select small and mid-cap companies with strong margins, governance, and innovation-led business models – particularly in India, Taiwan, and Southeast Asia. The portfolio, concentrated in fewer than 30 holdings, has achieved a 44.4% return since inception and outperformed both the MSCI Emerging Markets Index and its LSE-listed peers over the past 5 years. With earnings growth in emerging markets forecast at 14-16% for 2025-2026, MMIT sees an inflection point driven by attractive valuations, resilient GDP growth, favourable demographics, and global decoupling from overvalued developed markets. The Trust actively avoids overexposed sectors and geographies like China, maintains liquidity discipline, and integrates ESG factors into its investment process. Management is exploring portfolio gearing to enhance upside potential and continues to focus on aiming to deliver superior risk-adjusted returns. With a high active share and deep on-the-ground research, MMIT is likely to benefit from innovation-led value creation across emerging markets. Investors are encouraged to view the current discount as a long-term opportunity.

Last February, we published an article outlining South Korea’s newly announced Value Up Program introduced by the Financial Services Commission (FSC) together with the Korea Exchange (KRX). The program was designed to tackle the ‘Korea Discount’, whereby Korean equities trade at significantly lower valuations than to their global counterparts.

At the time of writing, the program’s specifics were limited. It was understood that it would comprise a set of voluntary guidelines encouraging companies to devise mid- to long-term targets to increase shareholder value. Companies participating in the program would receive substantial financial incentives. In addition, companies with a proven track record of profitability or those that were expected to boost valuations would be included in the upcoming Korea Value-up Index, with ETFs tracking the Index to be launched in Q4 2024. In fact, all four of our Korean holdings have been included in the Index.

Despite the program’s ambitious aims, initial reactions were cautious, with concerns raised about the lack of detail, particularly regarding the unspecified tax incentives that the FSC emphasised as a key reason to participate. In response, the FSC promised to release more concrete guidelines by June 2024.

A year on from the program’s launch, we believe it is timely to revisit the initiative to shed light on the more detailed framework that has since been released and to offer an assessment of its early successes and failures.

What Further Details Have Been Released?

The Corporate Value Up Program:

In May 2024, the FSC released their guidelines for the Value Up Program, which were published in full on their website in August. The guidelines recommend that companies’ Value Up plans include information from six key categories.

1. Company overview

Corporate information should be specified to provide a comprehensive description of the company, including business sectors, major products and services and company history.

2. Current status analysis:

Companies should disclose the most relevant financial indicators for medium- to long-term value improvement specific to their industry. These may include price-to-book ratio (PBR), price-to-earnings ratio (PER), return on equity (ROE), return on invested capital (ROIC), dividend payout ratio, shareholder return ratio, revenue growth, and so on. In addition, non-financial indicators, most significantly those related to corporate governance, are encouraged to be disclosed.

3. Goal setting:

Companies should set goals for improving their disclosed metrics to enhance corporate value in the medium- to long-term. These goals may include expanding R&D, investing in human and physical resources, efforts to increase shareholder returns, such as the cancellation of treasury stocks, and so on.

4. Planning:

Detailed plans should be submitted regarding how these goals will be achieved.

5. Implementation evaluation:

It is recommended that plans are submitted once a year, alongside a review of the previous year’s achievements.

6. Communication:

Companies should submit a report on the status, plans and performance of their communication, including quantitative methods for promoting effective communication, such as English translations of their Value Up plan.

The KRX commenced its first Corporate Value-up Award Program on 27 May, recognising and awarding companies with notable value-up achievements. In a prior press release the FSC stated that awarded companies will be eligible to receive (a) an exemption from the external auditor designation requirement, (b) a mitigation in penalties resulting from an audit review, (c) an exemption from KRX listing fees and annual dues, (d) an exemption from fees related to making changes to KRX listing status, and (e) a six-month postponement of sanctions resulting from dishonest disclosure.

The KRX plans to provide a range of services to support companies’ voluntary disclosures. These services will include disclosure-related training, providing information on the program to internal and external company directors, and offering one-to-one consulting services to support small and medium-sized businesses that may lack the human resources and physical infrastructure to develop and disclose their Value-up Plans independently. According to the KRX, it provided this consultation service to 55 companies in 2024, including nine from the KOSPI and 46 from the smaller KOSDAQ Index. The KRX plans to increase the number of consultations in 2025, offering the service to 50 KOSPI and 70 KOSDAQ companies. Priority will be given to companies that plan to participate in the Value Up Program.

The Korea Value Up Index:

Details of the Korea Value-up Index were released in September 2024, with ETFs tracking the index becoming live in December. The index comprises 105 companies listed on the KOSPI or the KOSDAQ, with the majority listed on the former. The Index is intended to serve as a benchmark for pension funds and institutional investors to help them identify companies with higher shareholder value.

Selection for the Index is based on criteria such as profitability and shareholder return, including dividends, share buybacks, price-to-book ratio and return on equity. Moreover, the KRX has adopted a relative evaluation method in order to account for differences across industry characteristics thereby ensuring sectorial balance.

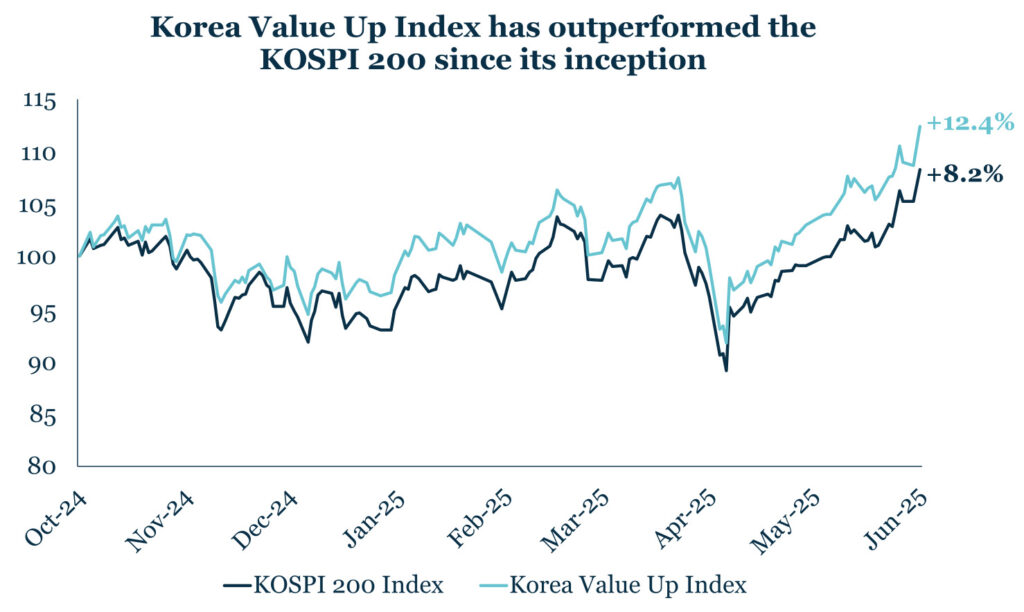

The Korea Exchange announced the first rebalance of the Index on 27 May 2025, adding 27 new stocks and removing 32. Changes reflect the preferential inclusion of companies actively disclosing Value-Up plans and the removal of those that have undertaken actions which may have harmed shareholder value or are not in line with the policies of the Value Up Program. The actual rebalancing was implemented on 13 June. We are pleased to announce that all four of our Korean holdings have retained their place on the Index, reflecting their commitment to high shareholder return and strong corporate governance in line with the goals of the Value Up Program.

Source: Bloomberg; as of 4 June 2025.

What are the Program’s Early Successes?

So, what—if anything—has the Value Up Program achieved in its first year? According to the FSC and the KRX, 125 companies had officially disclosed their Value Up Plans by the end of March 2025. While this represents only 5.1% of all listed firms on the KOSPI and KOSDAQ, these companies together account for 46.1% of total market capitalisation[1]. The Korean business news outlet, Chosun Biz, reported that, encouragingly, between the second quarter of 2024 and the first quarter of 2025, listed companies repurchased 22.88 trillion won worth of shares, a 2.4x YoY increase. Stock cancellations reached 19.59 trillion won, up 2.3x YoY, while cash dividends rose by 11% to a total of 48.35 trillion won. These developments suggest that early adoption of the program may already have translated into tangible changes in corporate behaviour.

Although the number of participating companies remains relatively low, momentum is said to be building as major Korean conglomerates, known as ‘chaebols’, begin to show increased interest. Hyundai Motor has already announced new targets for total shareholder return and share buybacks as part of its commitment to the initiative. LG and Posco are expected to join the program too. The Financial Times reported Jeong Eun-bo’s, Chief Executive of the KRX, argument that once Korea’s largest companies join the program, over time, it will encourage other companies to join due to Korea’s strong naming and shaming culture.

Additionally, Kim Byoung-hwan, Chairman of the FSC, has stressed that the program’s effectiveness should be evaluated in the long-term, acknowledging that shifts in corporate culture, particularly those involving governance and capital allocation, are always gradual. We share this view: the Value Up Program is a long-term structural reform initiative, designed with a decades-long horizon in mind. Japan’s own corporate reform efforts, which started over a decade ago and have only recently begun to bear fruit, demonstrate that such deep-rooted changes require a long-term strategy and perspective.

What are the Program’s Early Shortcomings?

The main criticism of the program is that it is voluntary. While 125 companies have joined, some argue that this figure is underwhelming. Whether this level of participation is significant or not ultimately depends on one’s perspective, but it is clear that the number would be higher with more enforceable guidelines or legislative obligations. Given the seriousness of the ‘Korea discount’, including the fact that the National Pension Fund is projected to be depleted by the 2050s due in part to the low valuation and growth of domestic stocks, the program’s non-compulsory nature seems misaligned with the scale of the problem. From this standpoint, many argue that the program should be mandatory to ensure companies are held accountable for delivering shareholder value and improving market efficiency.

Critics also highlight that the program falls short of addressing deep-rooted structural issues in Korea’s corporate environment. With inheritance tax rates as high as 50–60%, families are incentivised to suppress corporate valuations to mitigate future tax burdens on the next generation. Furthermore, the program does not prevent the opaque and complex cross-holding structures that many large Korean conglomerates rely on to maintain majority control, which in turn allow the interests of minority shareholders to be disregarded. Therefore, even if the program raises valuations to some extent, it is not until the conflicts of interests between the large corporations’ self-interests verses boosting shareholder value are aligned that the ‘Korea discount’ can truly be tackled for good.

What is the Future of the Program?

As it stands, the FSC has no plans to transition the initiative from a voluntary framework to an enforced one. This means that the program’s long-term success will depend on whether more companies choose to participate willingly. In turn, this will likely require additional regulatory activity and structural reforms to overcome entrenched disincentives.

The direction of the program may be significantly influenced by political developments. Following the impeachment of President Yoon Suk Yeol, resulting from his failed attempt to impose martial law, early elections were held on 3 June 2025 with Lee Jae-myung of the Democratic Korea Party (DKP) winning the election.

Lee has publicly committed to addressing abuses by controlling shareholders and promoting better governance in support of the Value Up Program. Notably, in March 2025, the DKP succeeded in pushing through a revision to the Commercial Act, aimed at expanding the fiduciary duties of board members. The revised law would require directors not only to act in the company’s interest but also to protect minority shareholders and promote board independence. However, the PPP under acting president Han Duck-soo vetoed the amendment on the basis of over regulation. While this has blocked the amendment, the DKP’s clear willingness to push through such reforms demonstrates a strong commitment to structural change and addressing corporate governance issues. Furthermore, with the DKP now in power, the legislation could be revived.

By following the regulations the new government prioritises during their initial period in office, we will soon have a better idea of the future of the Value Up Program. We will continue to closely monitor these developments, as well as any other relevant regulatory changes within Korea’s political landscape. Nevertheless, we believe that the Value Up Program is an important starting point for the country’s development towards higher valuations and better corporate governance. At the very least, the program has sparked conversations and drawn attention to these structural issues, which require the attention of both the corporate and political leaders of Korea for the long-term health of the country and its market.

Over the last 6 days, MCP analyst Swati Mehta has been in New Delhi and Mumbai meeting more than 30 companies and attending the Trinity India Conference organised by B&K.

Swati has shared with us some valuable insights from her trip:

”It was fascinating to meet companies across industries like tech, healthcare, capital markets and consumer electronics space amongst others. The challenges around liquidity and food inflation seem to be resolved now and while tariff related uncertainties exist, there has not been a material impact yet and it is expected to be offset by oil prices. Consumer demand is still a little slow, but there are plenty of green shoots – rural India seems to be doing better, discretionary products are seeing strong traction and private infrastructure spends have picked up. I continue to remain very excited about the India story and am impressed by the number of well-governed, capital efficient businesses in the country!”

Thank you, Swati! We couldn’t agree more – the opportunities in the dynamic and rapidly growing Indian market are some of the most exciting.

Since its official founding on 15 August 1948, South Korea has achieved remarkable economic success, combined with a turbulent journey towards democracy. The first 30 years of the nation’s history were dominated by authoritarian rule, with martial law frequently employed to maintain dictatorial control. It was not until 1987 that a democratic system was firmly established. Since then, the country has maintained a stable democracy, free from military coups and widely regarded as one of the most democratic countries in the region over the recent decades despite its young age.

However, that perception changed dramatically on 3 December 2024 when President Yoon Suk Yeol declared martial law on the grounds of protecting the country from “anti-state” forces sympathetic to North Korea. This caused international alarm around the state of the country’s democracy. South Korea’s standing in global democracy rankings declined sharply. For example, in the Economist Intelligence Unit’s Democracy Index 2024, the country fell to 32nd out of 167, down from 22nd in 2022.

However, we believe that the swift institutional response to this crisis, paradoxically, reaffirms the strength of South Korea’s democratic framework. The National Assembly acted quickly, suspending Yoon from office and initiating impeachment proceedings. On 14 December, Yoon was formally impeached and stripped of his presidential powers. Yoon was then arrested on 15 January 2025, following a failed attempt on 3 January 2025 as forces withdrew due to concerns for the safety of their personnel following resistance from pro-Yoon demonstrators and a military unit defending Yoon.

On 4 April, the Constitutional Court unanimously upheld the impeachment, officially ending Yoon’s presidency. A snap presidential election has been scheduled for 3 June, with several politicians having served as acting president in the interim period, including Han Duck-soo, Choi San-mok, and currently Lee Ju-ho.

So what are the implications of this impeachment crisis for South Korean democracy?

Despite the initial shock of martial law, the nation’s swift return to constitutional order is a testament to the fact that its institutional processes are capable of defending its democracy in the face of an extreme threat. The impeachment and lawful arrest of a sitting president sends a clear message that abuses of power will not be tolerated, and that the country’s institutional checks and balances are robust and functional.

The next president will take office against the backdrop of this crisis, acutely aware of subsequent public dismay it caused demonstrated by millions of people taking to the streets of Seoul to peacefully protest for Yoon’s arrest over several months. These protests were witnessed first-hand by an MCP analyst during a research trip to Korea in February.

So that leads on to the question of who will be the next President?

Lee Jae-myung, the Democratic Party (DKP) presidential candidate, has been the leader of the centre-leftist party since 2022. He lost the 2022 general election to Yoon Suk Yeol only by a margin of 0.8%. Additionally, he played a significant role in the impeachment of Yoon. However, Lee himself is not free from controversy and is actually contesting criminal charges around alleged bribery linked to a $1bn property development scandal. Courts have agreed to push back further hearings until after the election.

Kim Moon-soo is the People Power Party (PPP) presidential candidate, the current right-wing ruling party. He served as the minister of employment and labour from 2024 to 2025. While Kim publicly disagreed with President Yoon’s decision to declare martial law, notably he refrained from joining other cabinet members in issuing a formal apology and he opposed Yoon’s impeachment. Kim has resultingly gained much support from Yoon loyalists but has struggled to broaden support beyond this group. In the Gallup Korea poll released on 16 May, Kim trailed significantly behind Lee who led with 51% support compared to Kim’s 29%.

Not only is this election set in the aftermath of the recent impeachment crisis, it is also taking place amid the current global tariff crisis. Korea was one of the first countries to hold official trade talks with the US. The new president will be responsible for continuing these crucial negotiations in an attempt to prevent a potential 25% tariff on Korean exports to the US. This measure could be implemented on 8 July, when the current 90-day pause expires, if no trade agreement has been reached.

Moreover, the tariff crisis is set to exacerbate the country’s existing economic problems, which include low growth and a rapidly ageing population. It is hoped that, once the leadership vacuum has been filled, the country will be better able to respond to its current economic problems.

The first televised debate between the leading candidates took place on 18 May and included Lee, Kim, Lee Jun-seok of the minor centrist Reform Party and Kwon Young-kook of the minor progressive Democratic Labor Party.

In terms of the economy, Lee said that the government should play a more active role in stimulating domestic demand and promoting growth in key sectors such as the high-tech and renewable energy. This would involve development a form of ‘sovereign AI’ – something he likened to a similar, but free version of ChatGPT for the nation.

He promised to work towards promptly implementing a supplementary budget to boost the domestic economy and benefit ordinary people, as well as providing greater protection for unionised workers and introducing a four-and-a-half-day working week.

Meanwhile, Kim promised to create jobs, deregulate by creating a government agency dedicated to innovating regulations, and to invest more than five percent of the budget in research and development to spur economic growth.

Regarding the U.S, Lee and Kim promised to take very different approaches, with Lee preferring to take time to hash out a trade deal with the US that will ensure Korea benefits. In contrast, Kim emphasised the importance of South Korea’s alliance with the U.S., and that he would seek to hold a summit with Trump as soon as taking office in order to accelerate trade negotiations.

Additionally, Lee has called for constitutional reform to allow a four-year, two-term presidency and a two-round system for presidential elections through a referendum, in contrast to the single five-year term president’s currently serve. He also vowed to curb the presidential right to declare martial law and to hold account those responsible for the 3 December declaration.

It is also worth pointing out that the DKP pushed through a revision of the Commercial Act in March which expands the fiduciary duty of board members to act not only in the interest of the company, but also to protect the interests of minority shareholders and improve board independence. However, the PPP under acting president Han Duck-soo vetoed the amendment on the basis of over regulation. More broadly, Lee has vowed to renew efforts in support of the Value Up Program in order to improve corporate governance and raise Korean valuations, despite this initially being an initiative under Yoon Suk Yeol’s presidency.

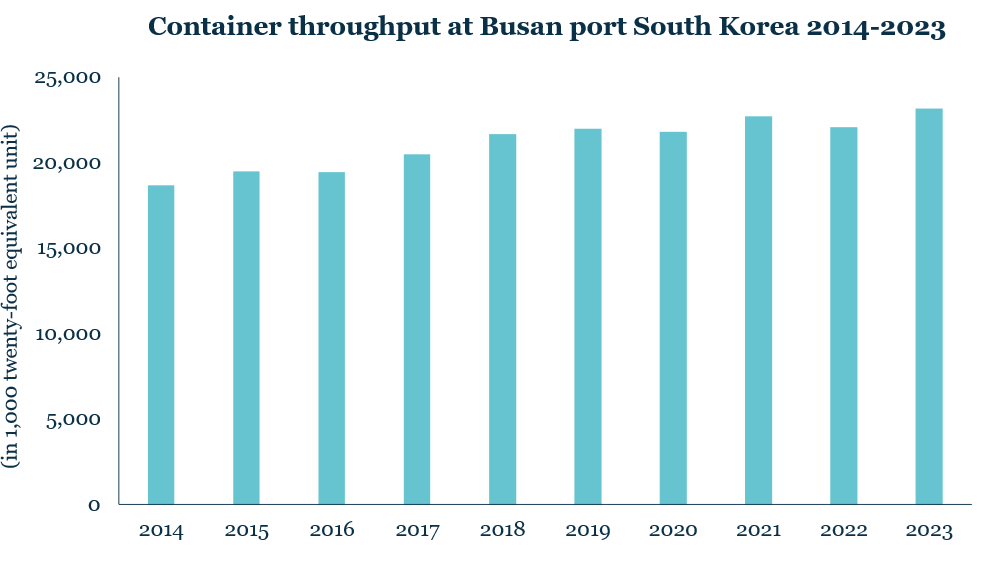

We will continue to monitor the ongoing political and economic developments in South Korea closely, assessing the impact of the next president’s policies on the country’s economy, its Value Up Program and our portfolio specifically. We believe that the new president must prioritise securing a favourable trade deal and restoring the international communities’ trust in the country’s democracy and institutional processes. Overall, we remain fundamentally confident in the country’s stability and its promising investment opportunities, particularly in the export market. For example, the chart below shows a significant increase in import and export traffic through Korea’s primary port, Busan, over the past decade.

The global economy is once again entering a turbulent phase, driven in part by the revival of aggressive U.S. trade policies under Donald Trump. His return to unilateral tariffs—particularly in the context of U.S.-China tensions—risks not only disrupting direct trade but also undermining the stability of global supply chains. While the immediate effects include higher prices and export slowdowns, the deeper, more lasting damage lies in weakened business confidence, delayed investments, and a breakdown in multilateral cooperation. For emerging markets, this isn’t just a moment to react—it’s a moment to rethink. To navigate this uncertainty, they must diversify their trade relationships, invest in regional partnerships, and build resilience in their economies. The shift toward a more multipolar and self-reliant trade system is not just inevitable, it’s essential.

Speaking exclusively to ET EDGE INSIGHTS, Carlos Hardenberg, Founder & Portfolio Manager, MCP Emerging Markets LLP,discussed the rising global market volatility driven by Donald Trump’s aggressive trade stance. He explored the far-reaching impact of tariffs, the evolving role of emerging markets, and whether the world is truly entering a new era of global trade. Hardenberg also highlighted Asia’s shifting economic gravity, investment opportunities in India, and shares valuable guidance for retail investors navigating today’s complex geopolitical landscape. He stated that “In times of uncertainty, staying invested with a long-term perspective often proves more rewarding than trying to time the market.”

Uncertainty and shock over the reciprocal tariffs announced on ‘Liberation Day’ by the new US administration has, to put it bluntly, created market chaos. The sharp global sell-offs are reminiscent of the turmoil experienced during the Covid-19 pandemic. As was the case then, few have been spared. Trump’s recent decision to delay reciprocal tariffs for 90 days applicable to any country that has not retaliated, has provided markets with what appears to be a temporary lifeline.

However, we do not interpret this as a signal that markets have bottomed, nor do we assume this policy will necessarily hold givenTrump’s unpredictability. Rather, this move appears to reflect a form of targeted pressure—some might say economic bullying—directed against China, particularly given that it remains the only country to have retaliated thus far. As a result, market confidence has been deeply shaken and we can expect elevated volatility and uncertainty to persist in the coming months.

Like many, we had anticipated the possibility of rising protectionism under a second Trump administration, though not to the extent we seem to be witnessing now. In recent months, we have proactively assessed the potential impact of higher tariffs on our portfolio. Each individual position has been carefully reviewed under this assumption, and we continue to re-evaluate our holdings in light of the evolving situation.

As far as the direct impact of Trump’s reciprocal tariffs is concerned, we believe companies exporting physical goods to the U.S. from countries facing the steepest approved tariff increases are likely to be most affected. Fortunately, although our portfolio includes companies based in several of these countries—which could be hit hard if the announced ‘Liberation Day’ tariffs are fully implemented—our current assessment suggests the immediate impact on our holdings may be limited. Many of our portfolio companies have minimal direct export exposure to the affected sectors, providing a degree of insulation from near-term disruption.

Take Classys, a Korean medical device manufacturer facing a potential 32% tariff on its U.S. imports. The company derives less than 5% of its revenue from sales to the U.S., significantly reducing the potential impact on overall earnings. The bulk of its revenue, approximately 35%, comes from the domestic Korean market, while Europe and Southeast Asia each contribute around 20%. Japan and Brazil account for roughly 10% each, providing further geographic diversification.

Additionally, the top three US-revenue exposed companies in our portfolio are asset-light, IP-based software companies. As a services industry, they are not directly targeted by the new tariffs. Furthermore, semiconductors are currently excluded from the newly announced tariffs. But the situation remains highly fluid. While chips themselves are not directly taxed, components that contain them, such as laptops and smartphones, had been at risk of future levies. However, over the weekend, the White House appeared to grant temporary exemptions for certain electronics, including smartphones, laptops, hard drives and flat-panel monitors. At the same time, a Section 232 investigation into semiconductor imports has been launched, raising the prospect of targeted tariffs based on national security grounds. We are closely monitoring developments in this sector, as it remains a potential flashpoint in the broader trade narrative.

Finally, we also prioritise business models oriented towards domestic consumption in select markets. As a result, our consumer holdings have minimal direct exposure to U.S. demand, with the exception being a Turkish apparel retailer, which derives less than 5% of its revenue from the U.S.

Beyond the direct taxation of goods, few businesses are likely to escape the broader, more insidious effects of escalating tariffs. Even in cases where companies are not directly targeted, tariff-induced slowdowns in demand and profitability can ripple through global supply chains, dampening investment sentiment and tightening margins. These second-order effects pose significant risks—not just to individual companies, but to entire economies. From shifts in consumer spending patterns to declining trade volumes and tightening financial conditions, the cumulative pressure could contribute to a broader global economic slowdown. We are actively assessing these cross-currents as we evaluate portfolio exposure and position for resilience.

In the meantime, the trade war between the US and China has exploded into full force. At the time of writing, the US has imposed tariffs of 145% on Chinese imports, while China has responded with tariffs of 125% on US goods. Who knows how much higher these could go. This extreme tariff war between the US and China alone will have serious repercussions across the global economy.

Amidst the chaos here are some glimmers of light on the tariff horizon. It’s worth remembering that we’ve been through a Trump-led trade war before, and global trade patterns had already begun to shift well before the current escalation. One of the most important structural changes over the past few decades has been the rise of South-South trade, particularly across Asia. Between 2007 and 2023, trade among developing countries more than doubled, from $2.3 trillion to $5.6 trillion, largely driven by Asia1. Intra-Asia trade alone is projected to grow from $4.3 trillion in 2023 to $7.1 trillion by 20302.

This diversification accelerated following the 2018 U.S.-China trade war, prompting countries to reduce reliance on U.S. imports. For example, China’s share of exports to the U.S. declined from 19% in 2017 to 14.7% in 20243. At the same time, many countries have been pursuing bilateral and regional trade deals that exclude the U.S. Notably, the Regional Comprehensive Economic Partnership (RCEP), signed in 2020, includes 15 Asia-Pacific nations and covers around 28% of global trade.

Although the U.S. will remain a dominant global importer, the accelerating pivot away from dependence on its market places many economies in a stronger position to withstand rising U.S. tariffs. We expect this trend to continue gaining momentum in light of recent developments, as countries intensify efforts to expand trade partnerships beyond the U.S.

In this uncertain environment, our top priority is to stay close to our portfolio companies and continuously reassess our investment theses in light of new insights and ongoing dialogue with stakeholders. To that end, we have scheduled additional research travel to remain close to developments on the ground and ensure we are ready to adapt swiftly as conditions evolve—especially given the many unknowns that remain, including the durability of the 90-day pause and the potential for new trade deals.

We believe experience and steadiness are vital during periods of heightened volatility. The MCP team has been through many market cycles, including the Asian financial crisis, the global financial crisis, and—during MCP’s own tenure—the Covid-19 pandemic. Since our launch in 2018, amid the first U.S.-China trade war, we believe we have guided the fund through an extraordinary period marked by global disruption, rising geopolitical tensions, inflationary shocks, tech sector uncertainty, and the renewed political ascent of Donald Trump.

Today’s surge in market volatility bears strong resemblance, in our view, to the dislocation seen in early 2020, when fear overtook fundamentals. At that time, we believe the team responded swiftly and strategically repositioning the portfolio to take advantage of market dislocations and initiating positions in high-quality companies from our watch list. These were businesses with sound fundamentals and durable models, which we believed were being unduly punished by market sentiment.

We believe this timely and deliberate response, combined with the quality of our portfolio holdings—characterised by competitive strength, solid balance sheets, robust corporate governance, and leadership in innovation—was a key contributor to the fund’s strong outperformance. By 14 September 2020, just 241 days after the Covid-related market peak, MEMF (Private C USD Founder) had recovered its losses. From the trough to the subsequent peak on 16 November 2021, the fund delivered a return of 136.5% over a 603-day period, before concerns around global rate hikes began to weigh on broader markets.

As long-term investors, we view the current environment through a similar lens. We do not believe this is a time to retreat, but rather an opportunity to build positions in resilient companies with strong fundamentals—businesses we believe are well-positioned to benefit from a long-term recovery particularly as history shows that the subsequent bull market tends to outperform its preceding bear market.

Uncertainty and shock over the reciprocal tariffs announced on ‘Liberation Day’ by the new US administration has, to put it bluntly, created market chaos. The sharp global sell-offs are reminiscent of the turmoil experienced during the Covid-19 pandemic. As was the case then, few have been spared. Trump’s recent decision to delay reciprocal tariffs for 90 days applicable to any country that has not retaliated, has provided markets with what appears to be a temporary lifeline.

However, we do not interpret this as a signal that markets have bottomed, nor do we assume this policy will necessarily hold givenTrump’s unpredictability. Rather, this move appears to reflect a form of targeted pressure—some might say economic bullying—directed against China, particularly given that it remains the only country to have retaliated thus far. As a result, market confidence has been deeply shaken and we can expect elevated volatility and uncertainty to persist in the coming months.

Like many, we had anticipated the possibility of rising protectionism under a second Trump administration, though not to the extent we seem to be witnessing now. In recent months, we have proactively assessed the potential impact of higher tariffs on our portfolio. Each individual position has been carefully reviewed under this assumption, and we continue to re-evaluate our holdings in light of the evolving situation.

As far as the direct impact of Trump’s reciprocal tariffs is concerned, we believe companies exporting physical goods to the U.S. from countries facing the steepest approved tariff increases are likely to be most affected. Fortunately, although our portfolio includes companies based in several of these countries—which could be hit hard if the announced ‘Liberation Day’ tariffs are fully implemented—our current assessment suggests the immediate impact on our holdings may be limited. Many of our portfolio companies have minimal direct export exposure to the affected sectors, providing a degree of insulation from near-term disruption.

Take Classys, a Korean medical device manufacturer facing a potential 32% tariff on its U.S. imports. The company derives less than 5% of its revenue from sales to the U.S., significantly reducing the potential impact on overall earnings. The bulk of its revenue, approximately 35%, comes from the domestic Korean market, while Europe and Southeast Asia each contribute around 20%. Japan and Brazil account for roughly 10% each, providing further geographic diversification.

Additionally, the top three US-revenue exposed companies in our portfolio are asset-light, IP-based software companies. As a services industry, they are not directly targeted by the new tariffs. Furthermore, semiconductors are currently excluded from the newly announced tariffs. But the situation remains highly fluid. While chips themselves are not directly taxed, components that contain them, such as laptops and smartphones, had been at risk of future levies. However, over the weekend, the White House appeared to grant temporary exemptions for certain electronics, including smartphones, laptops, hard drives and flat-panel monitors. At the same time, a Section 232 investigation into semiconductor imports has been launched, raising the prospect of targeted tariffs based on national security grounds. We are closely monitoring developments in this sector, as it remains a potential flashpoint in the broader trade narrative.

Finally, we also prioritise business models oriented towards domestic consumption in select markets. As a result, our consumer holdings have minimal direct exposure to U.S. demand, with the exception being a Turkish apparel retailer, which derives less than 5% of its revenue from the U.S.

Beyond the direct taxation of goods, few businesses are likely to escape the broader, more insidious effects of escalating tariffs. Even in cases where companies are not directly targeted, tariff-induced slowdowns in demand and profitability can ripple through global supply chains, dampening investment sentiment and tightening margins. These second-order effects pose significant risks—not just to individual companies, but to entire economies. From shifts in consumer spending patterns to declining trade volumes and tightening financial conditions, the cumulative pressure could contribute to a broader global economic slowdown. We are actively assessing these cross-currents as we evaluate portfolio exposure and position for resilience.

In the meantime, the trade war between the US and China has exploded into full force. At the time of writing, the US has imposed tariffs of 145% on Chinese imports, while China has responded with tariffs of 125% on US goods. Who knows how much higher these could go. This extreme tariff war between the US and China alone will have serious repercussions across the global economy.

Amidst the chaos here are some glimmers of light on the tariff horizon. It’s worth remembering that we’ve been through a Trump-led trade war before, and global trade patterns had already begun to shift well before the current escalation. One of the most important structural changes over the past few decades has been the rise of South-South trade, particularly across Asia. Between 2007 and 2023, trade among developing countries more than doubled, from $2.3 trillion to $5.6 trillion, largely driven by Asia1. Intra-Asia trade alone is projected to grow from $4.3 trillion in 2023 to $7.1 trillion by 20302.

This diversification accelerated following the 2018 U.S.-China trade war, prompting countries to reduce reliance on U.S. imports. For example, China’s share of exports to the U.S. declined from 19% in 2017 to 14.7% in 20243. At the same time, many countries have been pursuing bilateral and regional trade deals that exclude the U.S. Notably, the Regional Comprehensive Economic Partnership (RCEP), signed in 2020, includes 15 Asia-Pacific nations and covers around 28% of global trade.

Although the U.S. will remain a dominant global importer, the accelerating pivot away from dependence on its market places many economies in a stronger position to withstand rising U.S. tariffs. We expect this trend to continue gaining momentum in light of recent developments, as countries intensify efforts to expand trade partnerships beyond the U.S.

In this uncertain environment, our top priority is to stay close to our portfolio companies and continuously reassess our investment theses in light of new insights and ongoing dialogue with stakeholders. To that end, we have scheduled additional research travel to remain close to developments on the ground and ensure we are ready to adapt swiftly as conditions evolve—especially given the many unknowns that remain, including the durability of the 90-day pause and the potential for new trade deals.

We believe experience and steadiness are vital during periods of heightened volatility. The MCP team has been through many market cycles, including the Asian financial crisis, the global financial crisis, and—during MCP’s own tenure—the Covid-19 pandemic. Since our launch in 2018, amid the first U.S.-China trade war, we believe we have guided the fund through an extraordinary period marked by global disruption, rising geopolitical tensions, inflationary shocks, tech sector uncertainty, and the renewed political ascent of Donald Trump.

Today’s surge in market volatility bears strong resemblance, in our view, to the dislocation seen in early 2020, when fear overtook fundamentals. At that time, we believe the team responded swiftly and strategically repositioning the portfolio to take advantage of market dislocations and initiating positions in high-quality companies from our watch list. These were businesses with sound fundamentals and durable models, which we believed were being unduly punished by market sentiment.

We believe this timely and deliberate response, combined with the quality of our portfolio holdings—characterised by competitive strength, solid balance sheets, robust corporate governance, and leadership in innovation—was a key contributor to the fund’s strong outperformance. By 8 October 2020, just 261 days after the Covid-related market peak, MMIT had recovered its losses. From the trough to the subsequent peak on 11 November 2021, the fund delivered a return of 168.7% over a 660-day period, before concerns around global rate hikes began to weigh on broader markets.

As long-term investors, we view the current environment through a similar lens. We do not believe this is a time to retreat, but rather an opportunity to build positions in resilient companies with strong fundamentals—businesses we believe are well-positioned to benefit from a long-term recovery particularly as history shows that the subsequent bull market tends to outperform its preceding bear market.

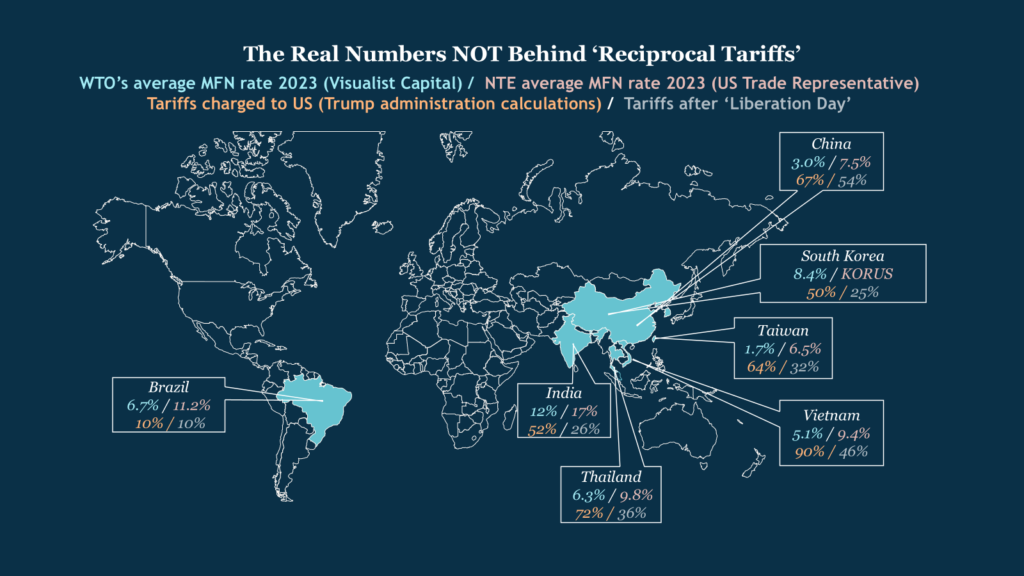

It doesn’t take much scrutiny to spot the flippant misinformation Trump often spreads on platforms like X and Truth Social, but he has now taken it a step further by incorporating fake news into the government’s official tariff policy. On ‘Liberation Day,’ Trump held up a board displaying the tariffs on US imports of the 60 ‘worst offenders’. The figures were shocking, such as Vietnam’s 90% tariff on U.S. imports, which could indeed justify an increased U.S. tariff in return.

However, these figures are blatantly false as they were calculated using an arbitrary and misleading formula: the US trade deficit with a country divided by the value of that country’s exports to the US in 2024. The reciprocal tariff rate is the resulting figure halved and rounded up.

In reality, the data tell a very different story. According to the 2025 National Trade Estimate (NTE) released by the Office of the US Trade Representative on March 31 2025, Vietnam’s average Most-Favored-Nation (MFN) applied tariff rate in 2023 was 9.4%. The report even says ‘‘the majority of U.S. exports to Vietnam face tariffs of 15 percent or less’’, with certain consumer-oriented food and agricultural products facing higher rates. Meanwhile, Visualist Capital’s mapping of WTO’s trade weighted average of MFN tariff rates shows Vietnam’s average is just 5.1%. An MFN tariff is one which applies equally to all WTO member countries, excluding special trade agreements.

Vietnam’s incorrect calculation is no fluke, take other countries and the data shows the US’s new calculations have highly inflated the number. An even greater discrepancy is evident in the case of South Korea which has almost entirely removed tariffs on US imports since the United States–Korea Free Trade Agreement (KORUS) enacted in 2012. The Korea Economic Institute of America calculated an average of 0.3-3.6% Korean tariffs on US imports in 2023.

This flawed methodology disproportionately penalises poorer, export-driven countries with large trade surpluses but limited imports from the US. For example, according to data from the US Consensus Bureau, while the EU’s trade surplus with the US is much larger (-$236 billion) than Vietnam’s (-$123 billion), the administration’s formula assigns a much higher tariff to Vietnam simply because it imports less in return ($13 bn vs $370 bn).

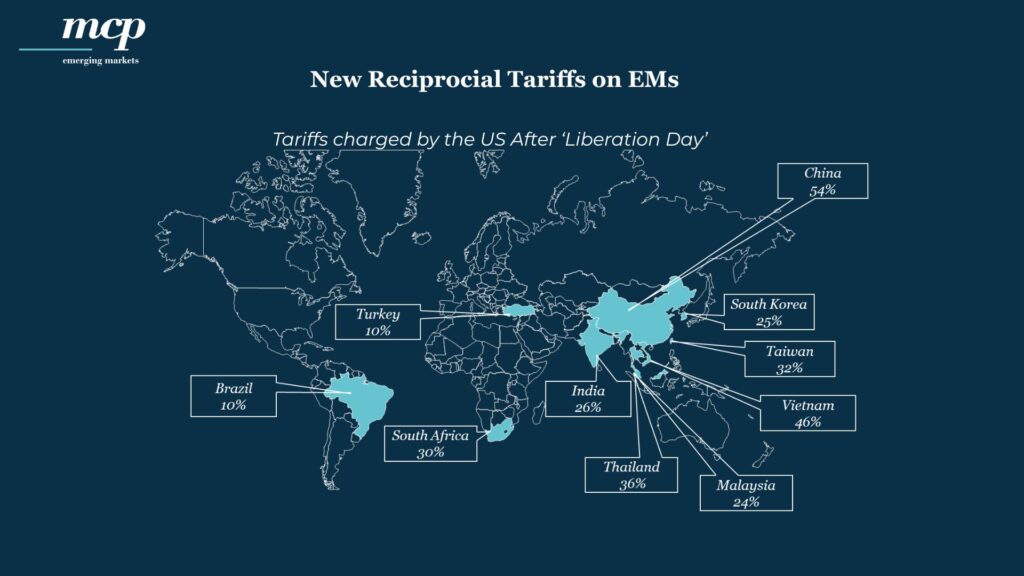

Donald Trump’s long anticipated tariff offensive was finally revealed yesterday on what he refers to as ‘Liberation Day’. We have mapped out the new tariffs impacting the EM countries where MCP is currently invested.

So far, these new tariffs have not significantly changed our outlook as the overall exposure of our holdings that export directly to the US in the affected sectors is limited. Notably, Trump has exempted certain sectors, such as semiconductors, where we maintain an overweight position. Likewise, our overweight exposure to the services sector, shielded from tariffs, adds to the resilience of our portfolio against these measures.

That said, we continue to remain cautious and watch the evolving situation closely, particularly any of Trump’s upcoming meeting with global leaders that could set a precedent for tariff negotiations. At the same time, we are monitoring potential indirect effects, such as an economic slowdown, shifts in global demand and supply chains or prolonged uncertainty in certain key sectors globally.

Our recent trips and direct engagement with portfolio companies in Taiwan, South Korea, and India further reinforce our confidence that the portfolio is well-positioned for the coming months.

On 11 March 2025, MCP Emerging Markets hosted a Zoom webinar where founding partner Carlos Hardenberg and investment analyst Swathi Seshadri provided an update on the strategy, performance and portfolio of the Mobius Investment Trust (MMIT).

The video below is a replay of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.