Mobius Investment Trust Wins Prestigious AIC Shareholder Communication Award for Best ESG Communication

London, 2 October 2025 – Mobius Investment Trust (MMIT) is delighted to announce that it has been named the winner of the Best ESG Communication category at the 2025 AIC Shareholder Communication Awards. This prestigious accolade recognises MCP’s innovative and impactful approach to communicating its environmental, social, and governance (ESG) strategy.

The awards, hosted by the Association of Investment Companies (AIC), celebrate exceptional shareholder communication among AIC member investment trusts and their managers. The judging panel, made up of industry experts including Anthony Leatham of Peel Hunt and investment journalists Moira O’Neill and David Stevenson, commended MCP for its original and engaging ESG communications approach.

MCP’s ESG strategy stood out for its transparency and sophistication, avoiding the repetition often seen in conventional ESG reports. The trust’s communications showcase how ESG integration drives stock-picking decisions, ensuring that ESG is not treated as a compliance exercise, but as a critical factor in generating sustainable returns for shareholders.

At the heart of MCP’s ESG efforts are its quarterly ESG factsheets, which provide clear, visually engaging updates on key ESG metrics and portfolio engagement activities. These factsheets highlight measurable progress, such as the significant improvement in environmental reporting from 58% in 2020 to 78% in 2025. Additionally, MCP has pioneered the integration of corporate culture into its ESG framework under the concept of “ESG+C(ulture),” recognising the importance of culture in driving performance.

Commenting on the award, Carlos Hardenber, Mobius Investment Trust Investment Manager said:

“We are honoured to be recognised by the AIC for our ESG communication efforts. This award reflects our commitment to transparency and innovation, ensuring that ESG reporting is not just informative, but also actionable and meaningful for our shareholders.”

For more information on our ESG strategy, visit the ESG section of our website.

This year, China has emerged as a tale of two sides.

On the one hand, economic data remains soft, highlighting ongoing challenges in the broader economy. On the other, equity markets have rallied, placing China among the top-performing countries year-to-date. Yet this momentum appears at odds with fundamentals, as gains seem driven largely by multiple expansion than earnings growth.

July’s economic data, released by the National Bureau of Statistics, missed consensus estimates, highlighting the problems inherent in China’s economy.

Continued weak domestic demand was evident in retail sales growing by just 3.7% YoY, down from 4.8% in June and marking the slowest growth in five months, while the ongoing property sector crisis was evident in property investments falling to -12% YoY from -11.2% in June.

Other indicators also disappointed: unemployment rose, bank loans shrank for the first time since 2005 and fixed asset investment slowed to 1.6% YoY.

Manufacturing exports rose 7.2% YoY, but this was largely due to exporters rushing shipments ahead of anticipated US tariffs. Industrial output grew just 5.7% YoY, down from 6.8% in June – the slowest pace since November.

This slowdown was partly due to adverse weather conditions as both unusually high temperatures and flooding disrupted factory activity and construction.

What is more, China’s producer prices fell by 3.6% YoY, marking the 34th consecutive month of producer deflation, highlighting China’s ‘involution’ problem, whereby fierce competition drives prices down, eroding margins and profitability.

E-commerce giants like Temu and AliExpress exemplify this dynamic.

To stimulate domestic demand, Beijing has introduced several measures. A home appliance trade-in scheme offers subsidies of up to 20%, now extended through year-end.

In July, annual subsidies of 3,600 yuan ($500) per child under three years were introduced to boost consumption and address demographic challenges. A one-year consumer loan subsidy programme begins in September, offering 1% interest subsidy on loans up to 50,000 yuan.

However, such subsidies offer only short-term relief and, once withdrawn, demand may falter, as they likely will not address deeper issues: low household confidence, especially with 70% of wealth tied to a declining property market and overcapacity in the private sector.

Monetary policy has also been accommodative. The People’s Bank of China cut the reserve requirement ratio by 0.5 percentage points in May and lowered key interest rates, injecting RMB 1trn in long-term liquidity. Yet the issue is not expensive loans – it is weak consumer confidence.

Bright spot

Now, let us turn to the bright spot – China’s stock market.

Chinese equities have outperformed the US and many global peers this year. The CSI 300 is up 17% while the MSCI China index is up 27% YTD in USD terms.

Within the MSCI China, communication services (+9.1%), consumer discretionary (+5.6%) and financials (+4.8%) have led the performance. The Hang Seng index is up 25% YTD in USD terms, with Hong Kong seeing a record $90bn inflow from the mainland H1.

This rally, despite weak macro data, seems to have been driven more by government intervention than earnings strength. State-backed equity purchases and a surge in corporate buybacks have supported prices.

Central Huijin Investment, a sovereign wealth fund, injected RMB 198bn ($28bn) in Q2, mostly into ETFs tracking the CSI 300. Announcements of anti-involution policies and further stimulus have buoyed sentiment. Higher liquidity from lower rates and high household savings, along with capital shifting from property to equities, has also helped.

On the company side, Chinese firms are delivering earnings per share (EPS) growth of around 10% YoY — the first time in seven years this aligns with expectations. However, revenues have been flat for nearly three years. EPS gains stem from margin expansion (non-financial net profit margins at 5.3%, near a 14-year high) and buybacks, which hit record levels in 2024.

Both drivers now show signs of fatigue: manufacturing overcapacity pressures margins, and buyback activity is slowing, raising concerns about the sustainability of earnings growth beyond 2025.

Although the trade war has caused periods of volatility, its impact on Chinese equities seems to have been short lived and relatively minor.

China has adapted by diversifying supply chains and tariffs have been less severe than feared – currently 30% versus Brazil and India at 50%. In fact, uncertainty has attracted foreign capital, boosting markets.

So, which side of China’s two tales will ultimately prevail?

So far, the stock market rally seems to have been driven more by sentiment, policy support and liquidity than by earnings growth or economic fundamentals. The absence of a clear rebound in the economic data raises questions about the rally’s sustainability.

The scale and effectiveness of policy measures going forward will be crucial. While past rounds of stimulus seem only to have had a limited impact on deflation and pricing pressures, larger stimulus could act as the driver for sustained market momentum.

Alternatively, investor disappointment in the measures taken, or their continued ineffectiveness, could be the trigger for a market correction.

We were delighted to host our annual Investor Day in London on Tuesday, 23 September 2025, bringing together investors and portfolio companies for a day of discussion and insights. For those who couldn’t attend, please find the full recording below.

Highlights included insightful presentations from CarTrade, an Indian multi-channel auto platform provider, and TOTVS, a Brazilian software provider. CarTrade and TOTVS presented their respective businesses, provided an outlook for the coming years, spoke about their engagement with the MCP team, and showcased their innovation and structural growth within their respective industries.

This year’s key takeaways highlight favourable conditions for our portfolio looking forward, including easing tariff uncertainty, declining US interest rates, strengthening emerging market currencies, and accelerating investment in AI and technology supply chains. Additionally, strong results and constructive outlooks from many of our holdings should position them well beyond 2025.

Emerging markets have been hit hard by the latest wave of U.S. tariffs, with Chinese goods facing levies of up to 35% and India and Brazil up to 50%.

Yet, Carlos Hardenberg, investment manager at MCP Emerging Markets LLP, argues that “despite the current wave of global protectionism and escalating trade tariffs, emerging markets continue to offer compelling investment opportunities.”

He highlights two key factors underpinning their resilience: strong domestic demand and growing trade diversification.

Over the past 15 years since the Global Financial Crisis, the United States Dollar (USD) has strengthened significantly, particularly against emerging market currencies, leading to widespread undervaluation compared to historical averages. Many 2025 market outlooks anticipated further USD gains, driven by so-called Trump Trades, with investors expecting sectors that benefit from tax cuts, deregulation, and protectionism to outperform.

However, these market forecasts were soon proven wrong as Trump’s erratic policies regarding tariffs has resulted in the weakening of the USD this year, giving rise to doubts about its continued long-term strength. At MCP, we believe the undervaluation of EM currencies compared to the USD presents attractive opportunities for investors.

What Does EM Currency Undervaluation Mean for Investors?

EM currency undervaluation provides key investment opportunities to capitalise on additional sources of alpha when the currencies re-rate and gain ground; a trend that has gained momentum this year. Brazil is a key example – the Brazilian Real (BRL) has appreciated 10% against the USD YTD as of the 31 July – a welcome contrast to the BRL’s 27% depreciation in 2024. Key drivers behind the Real’s appreciation include improving fiscal conditions, positive economic data, and successive hikes in its benchmark interest rate (the Selic), which currently stands at 15%, helping to stabilise inflation expectations.

While currencies can present opportunities for additional sources of alpha, we are conscious that they can also become significant detractor to returns. That is why currency risk will always remain a key consideration in our vigorous macro-overlays. Additionally, while we do not invest based solely on currency attractiveness, it can contribute to the broader investment case for a high-quality, attractively valued stock.

In countries with more vulnerable currencies, we mitigate risk by focusing on companies with diversified currency exposure. We particularly favour exporters generating revenue in hard currencies. For example, CI&T is a software company based in Brazil which caters to the US market, generating more revenue in USD than in real, while in Turkey, Hitit, an airline and travel IT Solution provider, generates 65% of its revenues in USD and 13% in EUR.

So how undervalued are EM currencies?

There are several factors suggesting that that emerging market currencies may be due for a reversal in their long-standing depreciation trend, a view increasingly supported by foreign exchange movements this year.

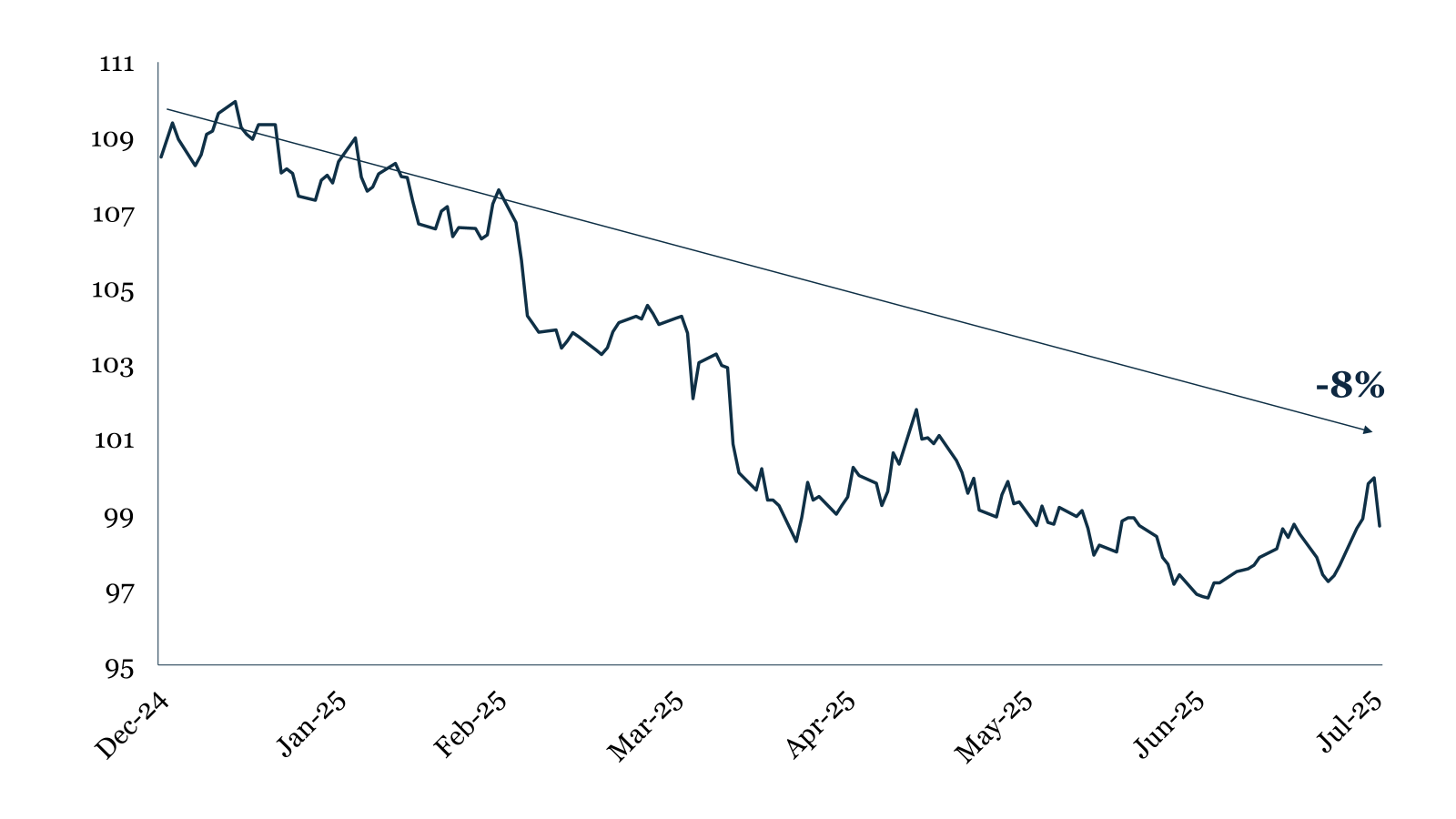

Firstly, the USD ended 2024 at two standard deviations above its 50-year average. Given the cyclical nature of currency markets, this suggests limited room for further appreciation[1]. In 2025 so far, the dollar has already retreated from its post-election highs, as market sentiment has turned increasingly negative towards Trump’s policies, fuelling concerns about a revival in inflation. This, coupled with an increasing fiscal deficit and mounting federal debt, has caused investor confidence in the US economy to decline.

USD Spot Index YTD

Source: Bloomberg, as of 31 July 2025.

The long-standing narrative of ‘American Exceptionalism’ that has driven US equity market dominance in recent years is beginning to unwind. In response, capital is increasingly shifting toward more globally diversified asset classes. Notably, emerging market portfolio inflows reached $42.8 bn in June according to data from the Institute of International Finance.

Should Trump’s erratic and inflationary policies continue, this erosion of trust in US institutions could become more permanent. Signs of this shift are already emerging, demonstrated by Moody’s downgrade of the US credit rating from AAA to Aa1 due to concerns around US debt.

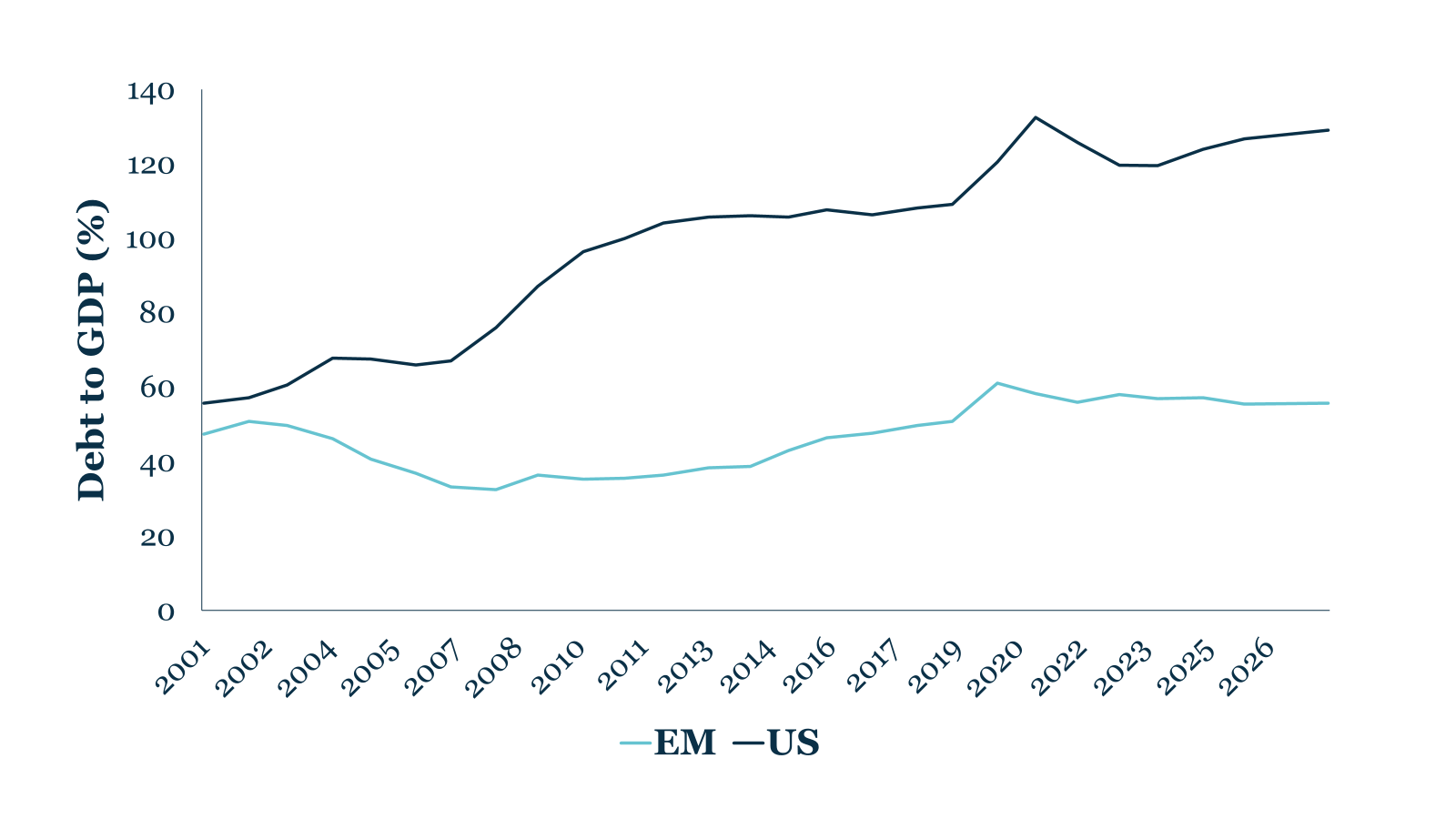

EM Debt has Remained Steady This Decade Compared to Soaring US Debt

Source: Ninety One, October 2024.

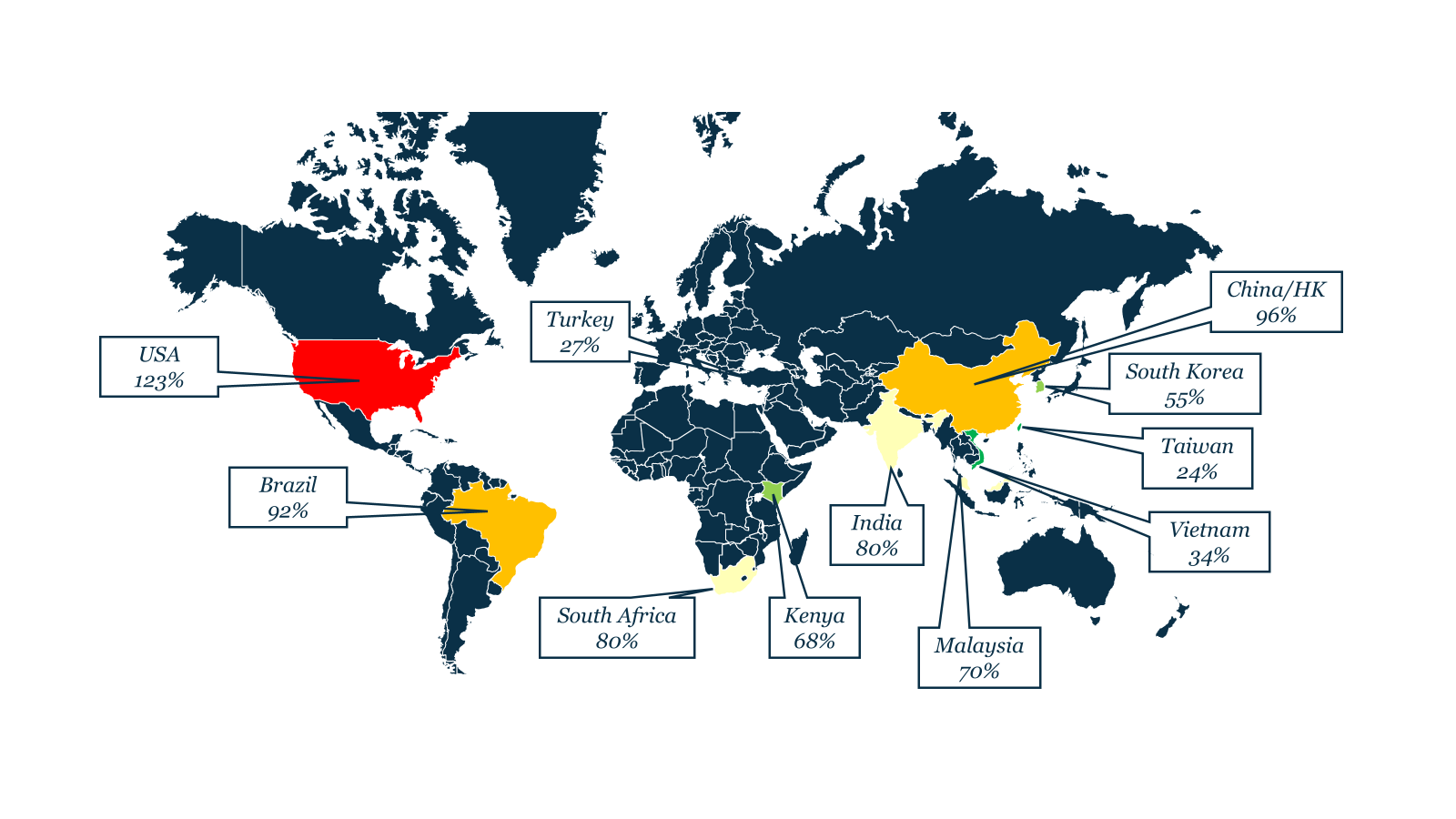

Many Emerging Markets Have Healthier Debt-to-GDP Ratios than the US

Source: IMF, April 2025. Percentages indicate general government gross debt as percent of GDP.

Globally, countries appear to want to move in only one direction: away from economic dependence on the US, including reducing their reliance on the US dollar. This is evident in the growing efforts of many countries to settle a larger share of their trade in domestic currencies. For example, in 2022 the Reserve Bank of India set up a trade mechanism to facilitate bilateral trade in Indian Rupee.

Adding further support to potential EM currency appreciations, global interest rates are on a downward trajectory. Although Trump’s policies may slow the pace of Fed rate cuts—despite his clear preference for looser monetary policy—the structural trend remains intact. Historically, a declining rate environment has supported EM currencies, given their inverse correlation with the USD. Lower US rates reduce the burden of dollar-denominated debt, easing external financing conditions for emerging markets.

Meanwhile, if EMs manage their own inflation effectively and maintain credible monetary policies, their currencies should strengthen as investor confidence shifts toward higher-yielding and well-managed EM economies. Notably, some of the strongest EM currency performers this year include the Brazilian real, Taiwanese dollar, South Korean won, and Malaysian ringgit.

We do not expect EM currency appreciation to occur uniformly across all EMs as each is shaped by its own unique mix of internal and external pressures. However, in cases where currencies do appreciate—especially those supported by strong structural reforms and credible institutions—the outcome can be meaningful alpha generation, as illustrated by Brazil this year.

Four asset managers, including Carlos Hardenberg, discuss their outlook for China, where they currently see particular opportunities or risks, and how they are currently positioned in their portfolios in Fundview.

View articlehere to learn about our approach to investing in China.

If you would like to attend or dial into the Investor Day please email Anna von Hahn at anna@mcp-em.com or Tess Peplow at tess@mcp-em.com. Please note this event is for professional investors only.

We would be delighted if you would join us for the MCP Investor Day 2025 on Tuesday, 23 September, at 11am (BST) at the Royal Society of Chemistry, Burlington House, Piccadilly, London W1J 0BA. This will be an in-person event with the option to join via Zoom. The investor day coincides with the Mobius Emerging Markets Fund and Mobius Investment Trust reaching their 7-year track records.

On this occasion, the founding partner, Carlos Hardenberg, and the MCP team, will reflect on the seven years since inception and provide an update on the portfolio, strategy and performance of the Mobius Emerging Markets Fund and the Mobius Investment Trust. Portfolio companies TOTVS and CarTrade will present their respective businesses, provide an outlook for the coming years and talk about their progress on ESG+C® efforts and their involvement and engagement with the MCP team.

The Companies

TOTVS provides enterprise software solutions with a strong presence in Brazil’s mid-sized business segment, primarily through its Enterprise Research Planning (ERP) platform. The company has been expanding its addressable market beyond traditional ERP into areas such as cloud services, HR tech, vertical SaaS, and business analytics. Its business model benefits from a high proportion of recurring revenues and integration with client operations.

CarTrade is a leading multi-channel digital marketplace in India, catering to both new and used car segments, as well as second-hand / used classifieds. Through multiple brands, it holds a dominant position in the market, ranked #1 across Auto Portals, Used Classifieds, and Vehicle Auction Platforms in India, despite having a topline of just <$100m.

The Speakers

Carlos Hardenberg

Carlos Hardenberg is the founder of MCP and has been Portfolio Manager of the strategy since inception in 2018. Carlos spent 17 years with Franklin Templeton Investments starting as a research analyst based in Singapore, focusing on South East Asia. He then went on to live and work in Poland before moving to Istanbul, Turkey for ten years. Carlos has spent extensive time travelling in Asia, Latin America, Africa and Eastern Europe researching companies and identifying investment targets.

He managed country, regional and global emerging and frontier market portfolios and was appointed lead manager of the LSE-listed Templeton Emerging Market Trust PLC in 2015. Carlos successfully managed the fund and generated significant outperformance over the entire period of his leadership. He also established and managed one of the largest global frontier market funds for a decade.

Gilsomar Maia

Gilsomar Maia is CFO and Investor Relations Officer at TOTVS. The executive has over 25 years of experience, including 15 in mergers and acquisitions, planning, and investor relations. He was named the Best CFO in the Technology, Media, and Telecommunications sector for Mid Cap companies by the “Latin America Executive Team” study, which was conducted and published by Institutional Investor magazine in the United States, from 2022 to 2024. Maia holds a degree in Accounting from Universidade Presbiteriana Mackenzie, an MBA in Capital Markets from the FIPECAFI Foundation, and an Advanced Certificate for Executives in Management, Innovation, and Technology from the MIT Sloan School of Management. Before joining TOTVS in 2006, he served as an Assurance Manager at Ernst & Young for eight years and later became the business controller for the Coimex Trading business unit.

Aneesha Bhandary

Ms. Aneesha Bhandary Executive Director & CFO Aneesha has played a pivotal role in CarTrade’s financial growth journey, including its IPO and post-listing governance. She joined CarTrade in 2015. She has been instrumental in taking the Company Public. Aneesha a 9 year stint with S.R.Batliboi & Co. LLP (Ernst & Young) as a Statutory auditor and has over 17+ years of experience in the field of Finance. With 19+ years of experience, Aneesha blends deep technical finance expertise with sharp business judgement. Aneesha has led initiatives in risk, reporting, investor engagement, and capital efficiency. Aneesha is also a Chartered Accountant and an IIM-C certified CFO, and was recognised as “Young CFO of the Year” by CII.

If you would like to attend or dial into the investor day, or have any further questions, please email anna@mcp-em.com. We look forward to welcoming you to this special event.

Throughout the past quarter—and indeed the entire year—we have experienced significant market volatility, driven in large part by shifting U.S. trade policies under the Trump administration, which have fuelled considerable uncertainty. Volatility peaked following the 2 April announcement of extraordinarily high, sweeping ‘reciprocal’ tariffs. This announcement shocked global markets, triggering sharp selloffs with some of the steepest price movements in decades. The subsequent pause of the tariffs to 9 July seemed only to confirm the erratic nature of U.S. policies, a sentiment further validated by the recent extension to 1 August.

Meanwhile, geopolitical tensions—including the ongoing war in the Ukraine and the escalating conflict in the Middle East—have added further layers of complexity to the global macro environment. Several emerging markets have faced their own significant challenges: India experienced a sharp market downturn in January and February; South Korea continued to navigate political instability following last year’s failed attempt to impose martial law; and Turkey came under renewed pressure after the arrest of President Erdogan’s main opposition leader. Finally, the surprise release of the Chinese chatbot DeepSeek introduced unexpected competitive dynamics in the global AI landscape, further unsettling investor sentiment.

Smaller, high-quality companies, particularly in the technology sector, were disproportionately affected by the uncertainty as investors fled to safe heaven assets like gold but also to the larger, more liquid names deemed to be less risky. Furthermore, amidst the volatility, we observed a market rotation into sectors such as banks and commodities. These areas, which we deliberately exclude from the portfolio due to their regulatory complexity, capital intensity, and limited pricing power, had already been trading at low valuations and therefore proved more resilient during recent market corrections.

Our portfolio is benchmark-agnostic, with an active share close to 100%, reflecting our high-conviction, bottom-up stock selection. While this naturally leads to periods of return divergence against the broader market, we believe it positions us well to deliver meaningful long-term outperformance.

We’ve navigated challenging periods before, such as in 2019 and 2022, and in both instances, the fund went on to deliver strong (out-)performance in the years that followed. As the dislocation begins to correct, MEMF’s NAV has started to recover, delivering 11.8% (Private C Founder USD) and 2.7% (Private C Founder EUR) terms over the quarter. Since inception, the fund has delivered a return of 49% (Private C Founder USD).

We viewed the recent market pullback as an opportunity to further strengthen the portfolio. We selectively added high-conviction names from our watchlist, taking advantage of attractive valuations and temporary dislocations. Active portfolio management has remained central to our day-to-day work: we trimmed or exited positions where, in our view, the macro environment had materially weakened the investment case and redeployed capital into more compelling opportunities. At the same time, we increased exposure to several high-conviction holdings that had been unfairly impacted by broader market sentiment. Encouragingly, many of our portfolio companies delivered strong Q1 results, with several beating expectations and issuing positive forward guidance, despite ongoing uncertainty.

Strong Q1 Results, Optimistic Outlook for 2025 & Beyond

Source: MCP, Bloomberg, company source. Figures refer to past performance. Past performance is not a guide to future performance.

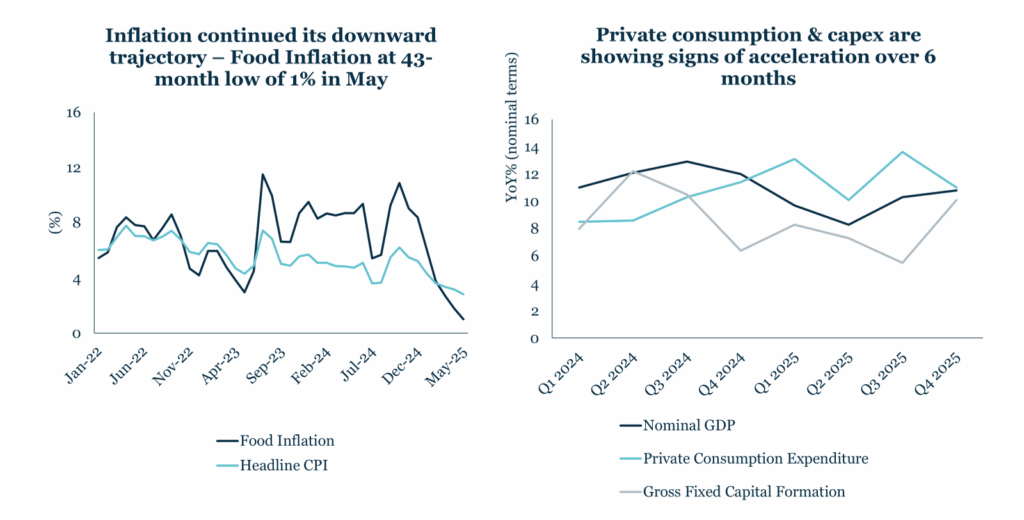

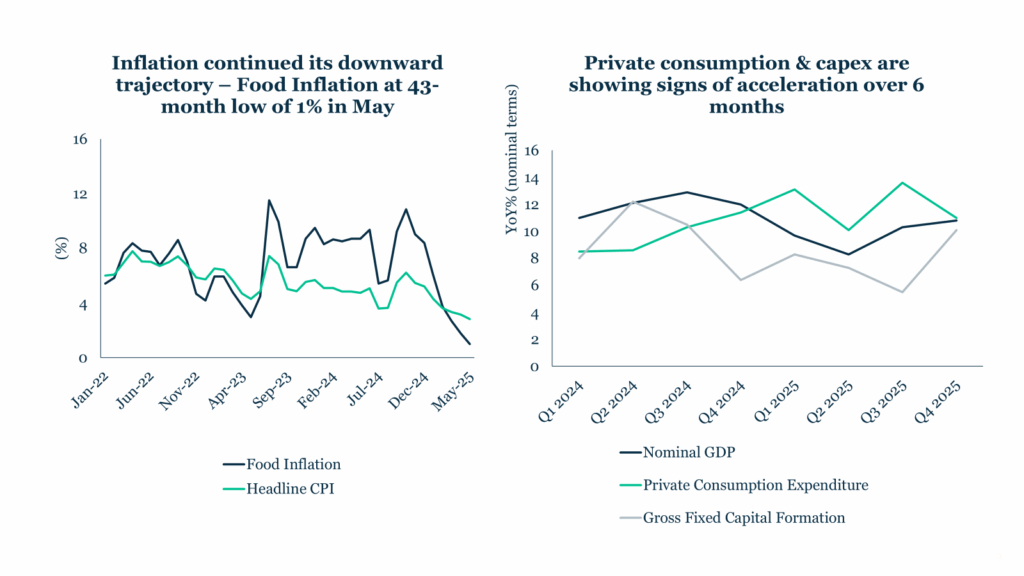

Our extensive on-the-ground research this year—spanning visits to Taiwan, India and Korea—provided valuable insight and generated a number of promising new ideas. India stands out as a particularly strong focus for us. We took advantage of market weakness earlier this year to add undervalued names, supported by an improving macro backdrop that includes rate cuts, easing inflation, and increased liquidity in the banking sector.

Economic Indicators Point to Continued Recovery in India

In Korea, the outcome of the 3 June elections brought political stability, which has boosted stock performance. The new government is pursuing a broad agenda of market-friendly reforms, not only to tackle the longstanding ‘Korea discount’, but also to enhance overall corporate governance, capital efficiency, and investor confidence. As a result, new opportunities are emerging, particularly in the technology sector. Brazil has also remained on our radar, with compellingly low valuations, improving macro fundamentals, and a strengthening real contributing to a more constructive outlook.

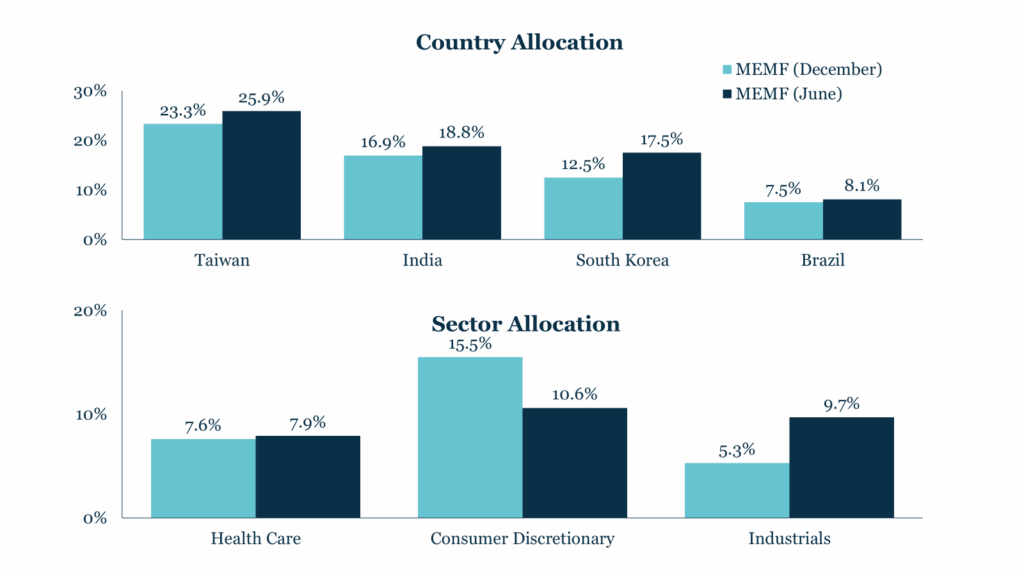

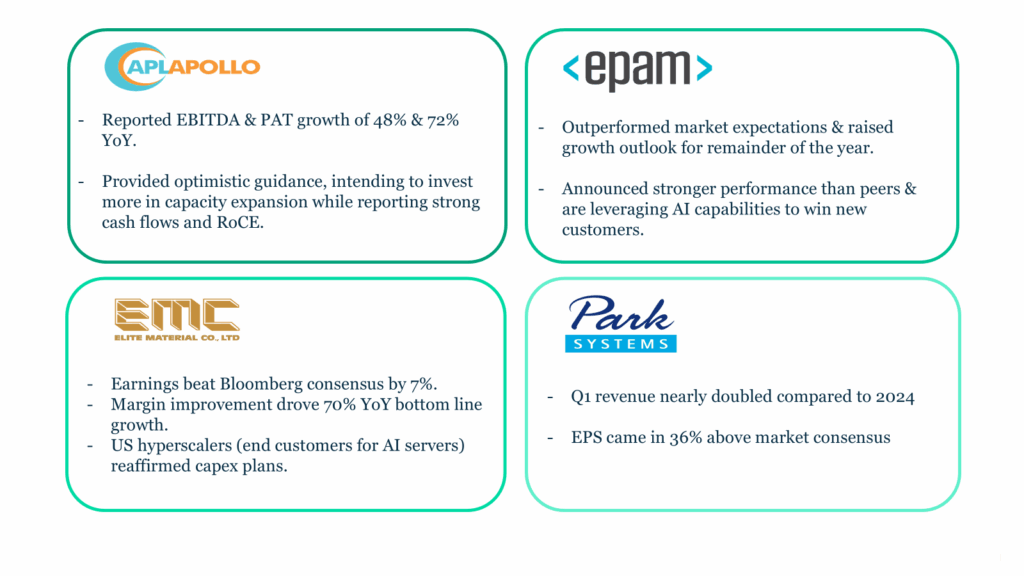

From a sector perspective, we have been active as well. In health care, we began reducing our position in Korean medical aesthetics company Classys after realising significant profits over the course of the holding period. In industrials, we added to APL Apollo and bought KEI Industries in India to capitalise on Indian infra and energy capex demands.

In consumer discretionary, we added CarTrade given its dominant position in car classifieds in India catering towards local consumption growth. We remain bullish on the technology sector; however, the composition of our tech holdings has been thoughtfully realigned to reflect our evolving views amid current macroeconomic challenges, broader market trends, and shifting IT spending priorities.

Country/Sector Allocation Changes YTD

Source: Bloomberg, MCP. MEMF (December): as of 31 December 2024. MEMF (June): as of 30 June 2025.

After the ‘DeepSeek scare’—when a Chinese artificial intelligence start-up launched a high-performing model at lower cost—first-quarter results from Amazon and Alphabet confirmed strong momentum in artificial intelligence investment. Businesses are rapidly shifting to artificial intelligence-driven models, requiring continued large-scale investment in computing infrastructure.

Encouragingly, many of our portfolio companies in the technology sector echoed this trend in their Q1 earnings reports, providing constructive guidance for the year ahead and pointing to an emerging rebound in demand, driven by renewed strength in AI-related spending.

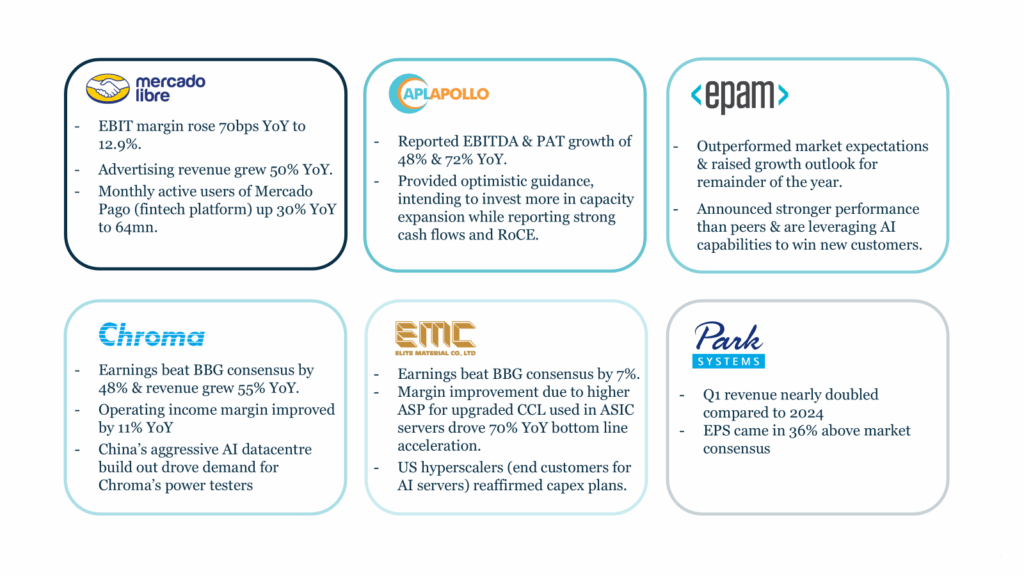

For example, Chroma, a Taiwanese supplier of testing equipment, beat Bloomberg earnings consensus by 48% driven by a 11% increase in operating margin year-on-year, and a 55% year-on-year revenue growth. Demand for Chroma’s power testers was supported by China’s aggressive AI datacentre build out, and the company’s outlook remains constructive for the rest of the year as it is entering a leading foundry’s packaging supply chain with a customised metrology tool.

Meanwhile, Elite Material (EMC), the global leader in high-speed copper-clad laminates (CCLs), reported earnings 7% ahead of Bloomberg consensus. EMC’s tailwinds came from strong demand for higher-priced CCLs, predominantly used in Application-Specific Integrated Circuit (ASIC) servers, which drove a 70% YoY bottom line acceleration. The reaffirmation of US hyperscalers’ (the end customers for AI servers) capex plans has reinforced EMC’s positive outlook.

The careful refinement of the portfolio has culminated in a deliberate and focused consolidation into 29 high-conviction holdings—companies we believe are best positioned to deliver sustainable, long-term growth. This portfolio is testament to our continued focus on high-quality businesses with deep moats and a strong orientation toward innovation. Throughout periods of market volatility, we have remained disciplined and patient, staying true to our convictions and executing the strategy we set out.

While we monitor macroeconomic developments closely, we adjust our positioning only when we believe such shifts materially affect a company’s long-term investment case. Underscoring our confidence in the strategy, the team increased its own commitment to the fund during the recent market pullback—demonstrating strong alignment with long-term shareholders. Much like the rebounds that followed challenging periods in 2019 and 2022, we view 2025 in a similar light. With improving visibility into the remainder of the year, we believe there is good potential for continued recovery, despite ongoing volatility and near-term challenges.

Outlook

Looking ahead, U.S. trade policies continue to inject a persistent sense of uncertainty and volatility into the economic outlook for the coming months. The initial 90-day reciprocal tariff pause—subsequently extended by an additional month—was designed to create space for the U.S. to negotiate new trade agreements. Yet, progress has been limited. To date, only the United Kingdom, Vietnam, Indonesia and China – though limited in scope – have reached accords, highlighting the limited effectiveness of a strategy centred around economic pressure.

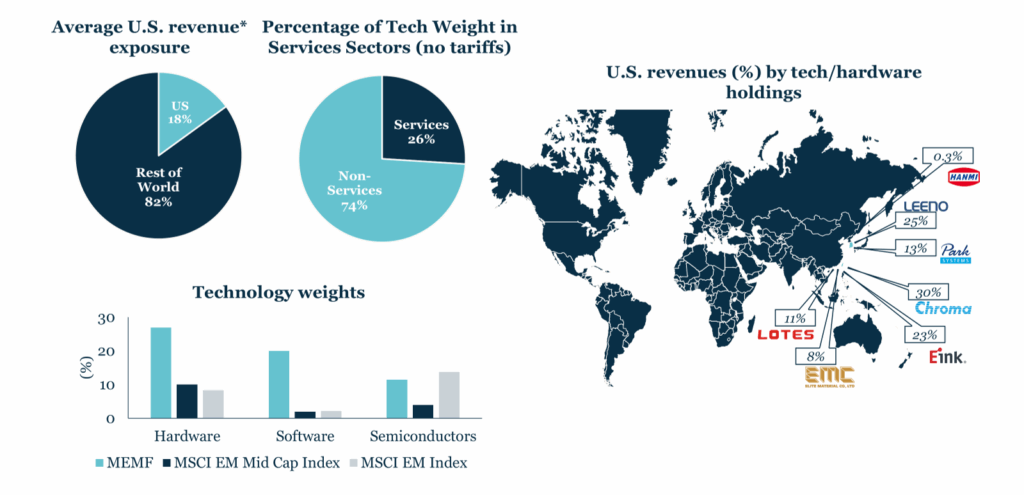

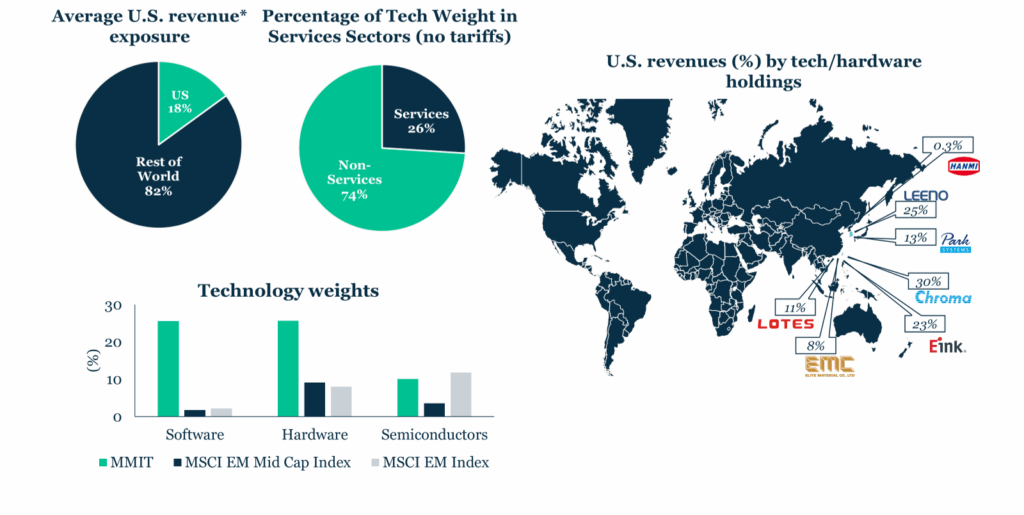

We continue to monitor the potential impact of heightened tariffs on our portfolio. However, direct exposure seems to be modest. Firstly, a large portion of our technology exposure is based in the software-as-a-service industry, and as services, these are not subject to tariffs.

Secondly, our remaining tech holdings, primarily in the semiconductor and hardware sectors, which are largely currently exempt from tariffs, generate only a limited share of their direct revenue from the U.S. market.

Thirdly, we favour business models oriented towards domestic consumption in select geographies, such as India, which similarly have minimal direct exposure to the U.S. Nonetheless, we continuously monitor the potential broader impact of the seemingly erratic U.S. policies on our portfolio.

Source: Bloomberg, MCP. As of 30 June 2025. Revenue data for FY2024.

MEMF Tech Holdings Show Low Direct Exposure to the U.S.

Source: Bloomberg, MCP. As of 30 June 2025. Revenue data for FY2024. Actual exposure through direct shipments is significantly lower than revenue exposure (e.g., Taiwan equipment maker shipping to OSATs and receiving revenue from US customer).

More broadly, the U.S. may be absorbing greater-than-expected fallout: rising inflation, weaker growth and confidence, and a softening dollar suggest a reversal in the decade-long USD strength—potentially a tailwind for emerging markets. With EM inflows rebounding ($19.2bn in May, tracked by the Institute of International Finance (IIF)), and a shift away from concentrated U.S. exposure, we believe our portfolio is well positioned to benefit.

Throughout the past quarter—and indeed the entire year—we have experienced significant market volatility, driven in large part by shifting U.S. trade policies under the Trump administration, which have fuelled considerable uncertainty. Volatility peaked following the 2 April announcement of extraordinarily high, sweeping ‘reciprocal’ tariffs. This announcement shocked global markets, triggering sharp selloffs with some of the steepest price movements in decades. The subsequent pause of the tariffs to 9 July seemed only to confirm the erratic nature of U.S. policies, a sentiment further validated by the recent extension to 1 August.

Meanwhile, geopolitical tensions—including the ongoing war in the Ukraine and the escalating conflict in the Middle East—have added further layers of complexity to the global macro environment. Several emerging markets have faced their own significant challenges: India experienced a sharp market downturn in January and February; South Korea continued to navigate political instability following last year’s failed attempt to impose martial law; and Turkey came under renewed pressure after the arrest of President Erdogan’s main opposition leader. Finally, the surprise release of the Chinese chatbot DeepSeek introduced unexpected competitive dynamics in the global AI landscape, further unsettling investor sentiment.

Smaller, high-quality companies, particularly in the technology sector, were disproportionately affected by the uncertainty as investors fled to safe heaven assets like gold but also to the larger, more liquid names deemed to be less risky. Furthermore, amidst the volatility, we observed a market rotation into sectors such as banks and commodities. These areas, which we deliberately exclude from the portfolio due to their regulatory complexity, capital intensity, and limited pricing power, had already been trading at low valuations and therefore proved more resilient during recent market corrections.

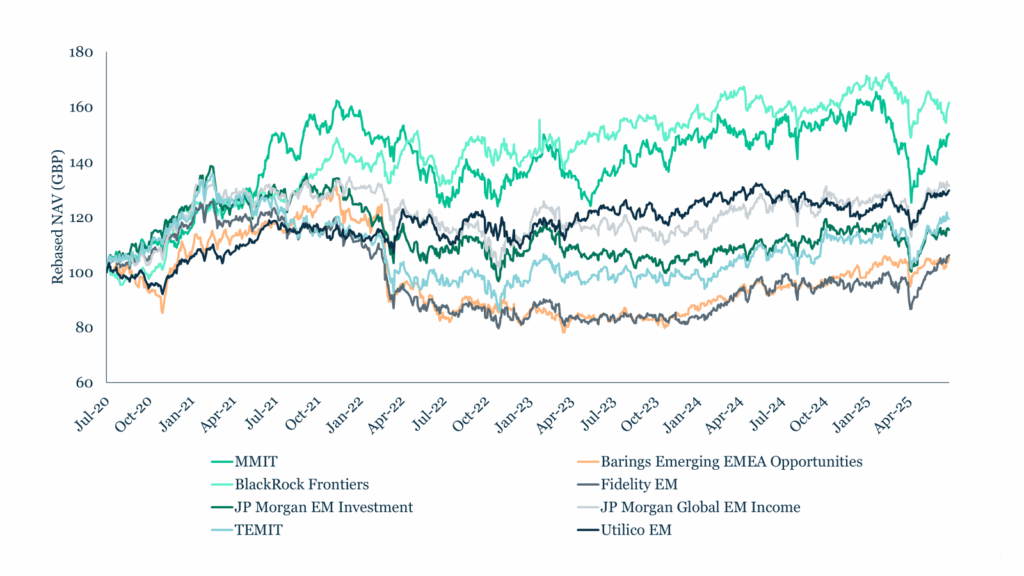

Our portfolio is benchmark-agnostic, with an active share close to 100%, reflecting our high-conviction, bottom-up stock selection. While this naturally leads to periods of return divergence against the broader market, we believe it positions us well to deliver meaningful long-term outperformance for investors. We’ve navigated challenging periods before, such as in 2019 and 2022, and in both instances, the trust went on to deliver strong (out-)performance in the years that followed. As the dislocation begins to correct, MMIT’s NAV and share price have started to recover, delivering 6.5% and 5.2% in GBP terms over the quarter. Since inception, the trust has delivered a NAV return of 54.8%.

MMIT is one of the Leading EM Trusts Over the Past 5 Years*

Source: Bloomberg, Frostrow, MMIT, rebased. As of 30 June 2025.

We viewed the recent market pullback as an opportunity to further strengthen the portfolio. We selectively added high-conviction names from our watchlist, taking advantage of attractive valuations and temporary dislocations. Active portfolio management has remained central to our day-to-day work: we trimmed or exited positions where, in our view, the macro environment had materially weakened the investment case and redeployed capital into more compelling opportunities. At the same time, we increased exposure to several high-conviction holdings that had been unfairly impacted by broader market sentiment.

Encouragingly, many of our portfolio companies delivered strong Q1 results, with several beating expectations and issuing positive forward guidance, despite ongoing uncertainty.

Strong Q1 Results, Optimistic Outlook for 2025 & Beyond

Source: MCP, Bloomberg, company source. Figures refer to past performance. Past performance is not a guide to future performance.

Our extensive on-the-ground research this year—spanning visits to Taiwan, India and Korea—provided valuable insight and generated a number of promising new ideas. India stands out as a particularly strong focus for us. We took advantage of market weakness earlier this year to add undervalued names, supported by an improving macro backdrop that includes rate cuts, easing inflation, and increased liquidity in the banking sector.

Economic Indicators Point to Continued Recovery in India

In Korea, the outcome of the 3 June elections brought political stability, which has boosted stock performance. The new government is pursuing a broad agenda of market-friendly reforms, not only to tackle the longstanding ‘Korea discount’, but also to enhance overall corporate governance, capital efficiency, and investor confidence. As a result, new opportunities are emerging, particularly in the technology sector. Brazil has also remained on our radar, with compellingly low valuations, improving macro fundamentals, and a strengthening real contributing to a more constructive outlook.

From a sector perspective, we have been active as well. In health care, we began reducing our position in Korean medical aesthetics company Classys after realising significant profits over the course of the holding period. In industrials, we added to APL Apollo and bought KEI Industries in India to capitalise on Indian infra and energy capex demands.

In consumer discretionary, we added CarTrade given its dominant position in car classifieds in India catering towards local consumption growth. We remain bullish on the technology sector; however, the composition of our tech holdings has been thoughtfully realigned to reflect our evolving views amid current macroeconomic challenges, broader market trends, and shifting IT spending priorities.

Following the ‘DeepSeek scare’ —when Chinese AI start-up DeepSeek introduced a large language model (LLM) with performance on par with Western counterparts but developed at significantly lower cost—Q1 results from hyperscale cloud providers such as Amazon and Alphabet reaffirmed the robust momentum of AI-related investment. The reality remains that businesses globally are accelerating their transition toward AI-driven models, necessitating sustained, large-scale investment in compute infrastructure. Encouragingly, many of our portfolio companies in the technology sector echoed this trend in their Q1 earnings reports, providing constructive guidance for the year ahead and pointing to an emerging rebound in demand, driven by renewed strength in AI-related spending.

For example, Chroma, a Taiwanese supplier of testing equipment, beat Bloomberg earnings consensus by 48% driven by a 11% increase in operating margin year-on-year, and a 55% year-on-year revenue growth. Demand for Chroma’s power testers was supported by China’s aggressive AI datacentre build out, and the company’s outlook remains constructive for the rest of the year as it is entering a leading foundry’s packaging supply chain with a customised metrology tool.

Meanwhile, Elite Material (EMC), the global leader in high-speed copper-clad laminates (CCLs), reported earnings 7% ahead of Bloomberg consensus. EMC’s tailwinds came from strong demand for higher-priced CCLs, predominantly used in Application-Specific Integrated Circuit (ASIC) servers, which drove a 70% YoY bottom line acceleration. The reaffirmation of US hyperscalers’ (the end customers for AI servers) capex plans has reinforced EMC’s positive outlook.

The careful refinement of the portfolio has culminated in a deliberate and focused consolidation into 25 high-conviction holdings—companies we believe are best positioned to deliver sustainable, long-term growth. This portfolio is testament to our continued focus on high-quality businesses with deep moats and a strong orientation toward innovation (see section on top holdings below). Throughout periods of market volatility, we have remained disciplined and patient, staying true to our convictions and consistently executing the strategy we set out.

While we monitor macroeconomic developments closely, we adjust our positioning only when we believe such shifts materially affect a company’s long-term investment case. Underscoring our confidence in the strategy, the investment team increased its own commitment to the trust during the recent market pullback—demonstrating strong alignment with long-term shareholders. Much like the rebounds that followed challenging periods in 2019 and 2022, we view 2025 in a similar light. With improving visibility into the remainder of the year, we believe there is good potential for continued recovery, despite ongoing volatility and near-term challenges.

Outlook

Looking ahead, U.S. trade policies continue to inject a persistent sense of uncertainty and volatility into the economic outlook for the coming months. The initial 90-day reciprocal tariff pause—subsequently extended by an additional month—was designed to create space for the U.S. to negotiate new trade agreements. Yet, progress has been limited. To date, only the United Kingdom, Vietnam, Indonesia and China – though limited in scope – have reached accords, highlighting the limited effectiveness of a strategy centred around economic pressure.

We continue to monitor the potential impact of heightened tariffs on our portfolio. However, direct exposure seems to be modest. Firstly, a large portion of our technology exposure is based in the software-as-a-service industry, and as services, these are not subject to tariffs.

Secondly, our remaining tech holdings, primarily in the semiconductor and hardware sectors, which are largely currently exempt from tariffs, generate only a limited share of their direct revenue from the U.S. market.

Thirdly, we favour business models oriented towards domestic consumption in select geographies, such as India, which similarly have minimal direct exposure to the U.S. Nonetheless, we continuously monitor the potential broader impact of the seemingly erratic U.S. policies on our portfolio.

Source: Bloomberg, MCP. As of 30 June 2025. Revenue data for FY2024.

MMIT Tech Holdings Show Low Direct Exposure to the U.S.

Source: Bloomberg, MCP. As of 30 June 2025. Revenue data for FY2024. Actual exposure through direct shipments is significantly lower than revenue exposure (e.g., Taiwan equipment maker shipping to OSATs and receiving revenue from US customer).

More broadly, the U.S. may be absorbing greater-than-expected fallout: rising inflation, weaker growth and confidence, and a softening dollar suggest a reversal in the decade-long USD strength—potentially a tailwind for emerging markets. With EM inflows rebounding ($19.2bn in May, tracked by the Institute of International Finance (IIF)), and a shift away from concentrated U.S. exposure, we believe our portfolio is well positioned to benefit.

* The Company has selected the following eight companies from the AIC’s Global Emerging Markets sector to form its peer group. These were chosen based on alignment with the Company’s own investment universe, excluding a small number of regionally focused trusts with narrower mandates. The selected peers are: Ashoka WhiteOak Emerging Markets (not in graph above as no 5 year track record), Barings Emerging EMEA Opportunities, Fidelity Emerging Markets Limited, BlackRock Frontiers Investment Trust, JP Morgan Emerging Markets Investment Trust, JP Morgan Global Emerging Markets Income Trust, Templeton Emerging Markets Investment Trust, and Utilico Emerging Markets Trust.

On 9 July 2025, MCP Emerging Markets hosted a Zoom webinar where founding partner Carlos Hardenberg and investment analyst Swati Mehta provided an update on the strategy, performance and portfolio of the Mobius Emerging Markets Fund (MEMF).

The video below is a replay of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.