Moon Jae-in was elected as South Korea’s president 18 months ago after the impeachment and imprisonment of his predecessor Park. His mandate was clear: drive out corruption and improve corporate governance, particularly at the nation’s Chaebols. It started well: he appointed Kim Sang-Jo as the Head of a Fair Trade Commission. The so-called “Chaebol Sniper” has been a long time governance crusader, and his role was to curb the excesses of the Chaebol. But the initial enthusiasm was followed by disillusionment. Kim Sang Moon’s domestic agenda has lost momentum as reconciliation with North Korea has seemingly become his priorty. And his voters are far from happy: workers repeatedly took to the streets in November to protest Moon’s lack of reform. With an domestic economy in jeopardy and governance reform on the ropes, the “Korea Discount” is back.

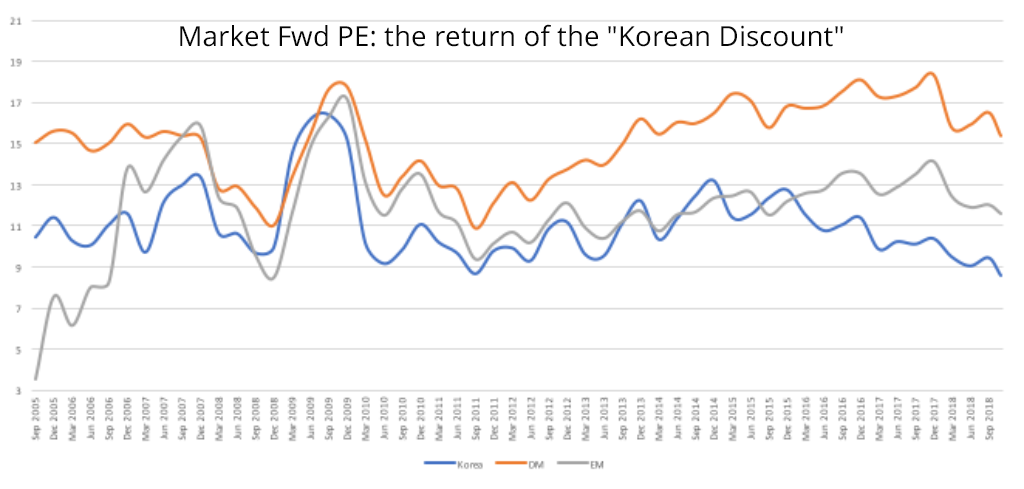

Source: Bloomberg

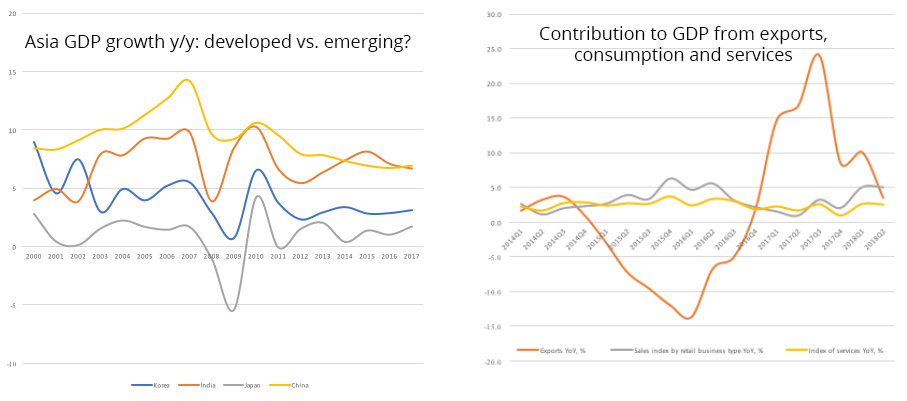

The Rise of the Chaebol Context is key. In the 1960s Park Chung Hee (killed by the head of the CIA in the Blue House, 1979) enrolled the help of leading businessmen to rebuild Korea. The “Miracle on the Han River” transformed Korea from a war ravaged country with per capita GDP below $100 to the economic powerhouse it is today, where per capita GDP stands at near $30,000. The achievement was astonishing – within barely two generations – and it was mainly down to a small group of entrepreneurs and their “chaebol”, the conglomerates they built in the process.[1]The Chaebol touched and continue to dominate all aspects of the economy. There are two dozen or so Chaebol remaining – of which Samsung, Hyundai and LG are the most famous. Their power is enormous – sprawling, interconnected webs of businesses in sectors as diverse as heavy industry and biotech. But with generational change, the Chaebol have fought to maintain their wealth and with that governance has suffered.Misaligned interestsBecause of an incentive structure skewed towards the preservation of control rather than the creation of value, Korean governance has been marginalised. The reasons are varied: 1) why disclose information which could jeopardise a competitive edge or anger customers; 2) why engage actively with financial markets when the focus is to build relationships with a few key clients; and 3) (in extreme cases) why increase your company’s valuation before a transitional period when the top rate of inheritance tax is almost 50%. Ironically, from the perspective of owner-managers and the wider shareholder value movement, there is no quicker way to weaken an owner’s control over a company than to attract external investors who increase its valuation. The result is webs of inter-related companies (despite improvements), excessive cash positions and limited focus on shareholder returns.Pressure to reformUntil recently, it was a given that what is good for the chaebol is good for South Korea. But this has changed after years of scandal and subterfuge. President Moon’s election in 2017 brought optimism around reforms to make Korean corporate governance more transparent, crystalising efforts made by previous administrations. Crucially the National Pension Service has adopted a formal stewardship code in July this year. The explicit aim is to push for better governance, transparency and accountably from its portfolio companies.[2]South Korea is at an economic cross-roads. The high growth days post-Asian crisis are long gone and Korea’s economy grew 2% year-on-year at the third quarter 2018, the slowest on-year growth since 2009. The export model that served them so well is faltering. China is doing to Korea what Korea did to Japan; and this is most evident in Korea’s biggest companies. Samsung Electronics’s market share in China has fallen from >20% in 2013 to less than 5% now; Hyundai Motor & Kia have lost 5% of market share to domestic auto manufacturers. The Korean economy is increasingly reliant on consumption – but consumption growth is tepid. The housing market is over-heating (despite the government’s efforts to dampen it), minimum wage regulation – designed to raise basic earnings – has just pushed jobs overseas, strained small and medium businesses, and reduced Korean competitiveness.

Source: Bloomberg

Opportunity for changeTax reform is rarely a subject to set pulses racing but in Korea it is essential: Korean individuals – particularly the third generation owners of Chaebols – are disincentivised to pay-out cash because they pay so much tax on their income.This goes some way to explain why the Korean market’s pay-out ratio is the lowest of major global markets at 20.8% (even Japan’s at 30% is higher); and why Korean company owners and managers are so pained to raise dividends. Ironically, tax code reform was taken off the agenda by a left-leaning president – partly because it is seen as a fillip to the oligarchs. President Park planned to address it.The corollary of higher pay-out ratios is focusing investment decisions on return on equity or return on invested capital: management deploying capital only when it makes economic sense, not because a client or the chairman says so. Employee stock option schemes – aligning interests between managers and owners – are rare. Adopting compensation structures which align the interests of owners, managers, employees and minority investors would be a marker to international investors that the old, misaligned ways are gone.Investment outlook The outlook is far from gloomy, however. After years of engaging with management teams, we are always impressed by the expertise and dedication they show. Korea is not the finished article, but change is afoot, and this brings the chance for re-ratings. Activist funds are springing up domestically, encouraged partly by the efforts of Elliot Advisors. In November Korean Airlines parent company was engaged by a local private equity house, the first high profile domestically driven activist case. This has sent shockwaves through boardrooms. A recent trip to Seoul confirmed how emboldened locals are feeling. Change is underway and corporations – feeling the pressure from investors – are taking notice.Our approach at Mobius is relatively straightforward: target companies offering earnings and cash flow growth trading at discount to their intrinsic valuations. Avoid businesses at risk from being disrupted by “China Inc.” and seek companies that have experienced generational change of ownership. There are several exciting opportunities in fast growth sectors (medical technology, ecommerce, gaming) but also less glamorous sectors (food products and turnarounds in heavy industry). South Korea is a source of world class intellectual property – from semiconductors to biotechnology and materials science. These companies are leaders in their fields and many trade at steep – and unjustified – discounts to international peers.We are excited about what the future holds. In the near term, it would help if Moon refocused on his agenda.[1] “jae” – wealth or property; and “beol” – faction or clan[2] NPS is itself not unfamiliar with corruption – the Chairman, Moon Hyung-Pyo was caught up in the scandal which ended President Park’s term.