The world’s attention is fixed on the outcome of what many have called one of the most divisive U.S. elections in recent history. Yet the results are anything but close, with a Republican sweep across the Senate, likely the House of Representatives, and, of course, the presidency, secured by Donald Trump. Businesses and governments worldwide are now asking how a second Trump presidency will affect them. Given Trump’s notorious unpredictability, the answer for many is not straightforward. At MCP, we’re asking the same for Emerging Markets and, despite the often pessimistic narrative, we’ve identified several potential silver linings in a Trump presidency.

Trump’s Domestic Economic Policies:

Trump positions himself as a champion of “the people,” and if that term refers to America’s wealthiest individuals and business leaders, he may be right. A central pillar of his domestic economic agenda is tax cuts, and with a Republican majority, an extension of the 2017 Tax Cuts & Jobs Act is highly likely. This act established a flat corporate tax rate of 21% and lowered individual tax rates, with the wealthiest Americans seeing the greatest benefit. Additionally, Trump has consistently advocated for deregulation, especially in sectors like digital assets and non-renewable energy.

Much like the pre-election polls, economists are divided on whether Trump’s next term will ultimately harm or hinder the U.S. economy in the long term. However, there is general consensus that, in the short term, Trump’s pro-business policies are likely to stimulate US economic growth. Herein lies the first silver lining for EM: a strong US economy has positive spill over effects on the global economy as it boosts demand from U.S. consumers for EM exports.

Trump, Trade and Tariffs:

However, the subject of Trump and trade is particularly sensitive for EM and Trump’s clear ‘America First’ stance is hard to ignore. Trump has been outspoken about his support for tariffs, yet both DM and EM may be left out in the cold as Trump has threatened a universal 10-20% tariff on all trading partners and indicated replacing income tax with tariff revenue via the proposed “Trump Reciprocal Trade Act.” That being said, China will clearly be the most effected with Trump advocating for a 60% tariff on Chinese imports.

It may be wise not to take such threats at face value. Trump himself has described tariffs as a powerful negotiation tool and he might actually use them as such. The reality is that the U.S. remains heavily reliant on imports, particularly from China, whose production capacity is unparalleled. Although there is momentum behind reshoring manufacturing, reducing the U.S.’s global trade deficits through this approach is likely a long-term endeavor, potentially spanning decades. This economic interdependence could restrain Trump’s ability to impose sweeping punitive trade measures without risking inflation and considerable supply chain and economic disruptions domestically.

Differing Impact on EM Regions:

While finding a silver lining in China itself may be challenging, it’s much easier to spot ones in countries like India, Indonesia, Vietnam, Malaysia, and Mexico. These nations, known for their low-cost manufacturing, are set to become even more attractive to FDI as the global shift to “China+1” accelerates. As higher tariffs on China undermine its cost competitiveness, supply chain gaps will emerge, offering these countries opportunities to meet the demand and capture a larger share of global manufacturing. This increase in production could help offset the negative effects of higher tariffs on their exports to the U.S.

Moreover, escalating U.S.-China trade tensions could create opportunities for other EM to strengthen their trade relationships with China. For example, during the trade war in 2018, China shifted from importing U.S. soy beans to sourcing them from Brazil. Similar patterns of retaliation could benefit countries with strong trade ties to China or those that produce goods that can replace US exports.

Resilience in EM:

Emerging Market companies have demonstrated their resilience, thriving even amidst geopolitical and economic uncertainties, thanks to robust business models, innovation, and strong growth prospects. Structural advantages such as favourable demographics, higher GDP growth projections, and ongoing digitalisation ensure that EM will remain competitive, despite potential tariff-related challenges.

While Trump’s presidency introduces a degree of unpredictability, more clarity over Trump’s intentions in the months ahead along with administration appointments is expected to reduce short-term market volatility. Although Trump’s policies pose risks to the global trade order, the outlook for EM is not all doom and gloom. In fact, certain EM regions stand to benefit from new growth and investment opportunities stemming from shifts set to accelerate under Trump such as China+1. We are confident that this resilient asset class will navigate these turbulent times as effectively as it did during Trump’s first presidency, during which the MSCI EM Index delivered a 57% return in USD terms1.

1 Bloomberg: From 20 January 2017 – 20 January 2021

Navigating Market Swings: Reflections on Volatility in Investing

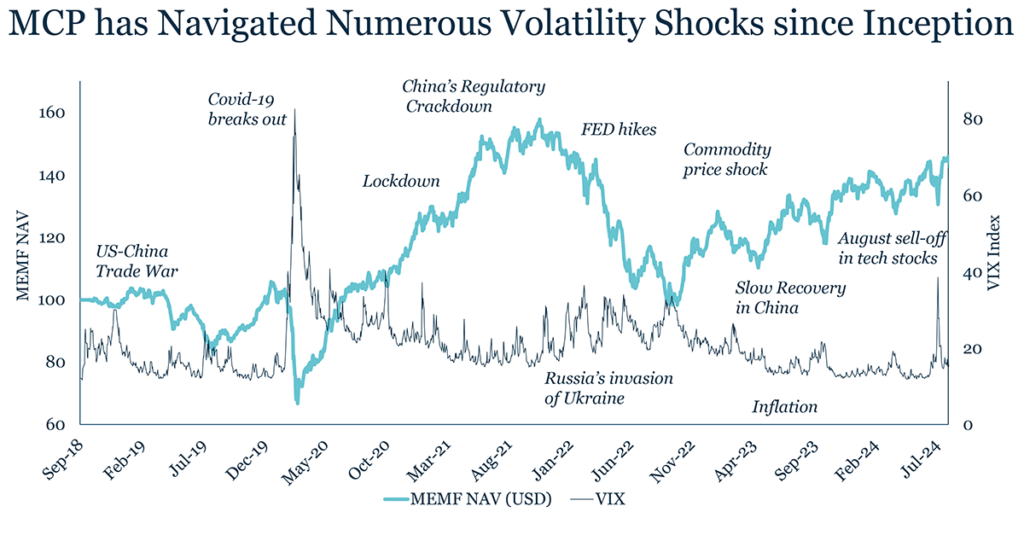

Navigating volatility has always been a priority for the MCP investment team, not just to mitigate risks but also to proactively capitalise on the opportunities that market fluctuations present. Given the recent spike in volatility this summer, we thought it was an opportune time to share our insights on navigating market turbulence, drawing on Carlos Hardenberg’s 25+ years of experience. Beginning his career during the Asian financial crisis, Carlos has navigated the dotcom bubble, the global financial crash, the Covid-19 pandemic and numerous other market disruptions. His experience as a long-only equities investor has only reinforced the idea that volatility can be your friend if you use it effectively.

Understanding Volatility

Managing market volatility starts with understanding its causes — asking why investors buy one day and sell the next, often without any significant change in fundamentals. This behaviour is rooted in the fear of the unknown, a human characteristic to which investors are not immune.

Source: Bloomberg. As of 30 September 2024.

Uncertainty leads to nervousness, causing a risk-averse instinct which, in investing, often leads to sell-offs. The herd mentality exacerbates the situation — as everyone else sells, the fear of being left behind and suffering greater losses grows stronger, pushing more investors to follow suit. The widespread use of algorithmic trading, most of which trades on the same set of predefined conditions that mirror market movements, compounds the effects of sell-offs and thus increases volatility further. In 2018, Select USA estimated that algorithms now dominate 60-75% of trading in major US, European and Asian markets.

Leveraging Volatility

In times of volatility, we believe it is important to remain calm and focus on fundamentals and the long-term. We seek high-quality companies with excellent management teams, strong moats, positive cashflows and little to no debt. These companies are more likely to prove resilient and maintain a positive outlook. Nevertheless, we always monitor macro developments and their potential impact on our investment case very closely. Timing is critical in responding to changing macro and micro conditions — selling too early or too late can have significant consequences. Yet 25 years of investment experience has taught Carlos that selling on volatility alone usually leads to poor investment decisions. During the 2008 global financial crisis, many investors fled risk assets such as emerging markets, resulting in a vast pool of undervalued EM stocks despite their strong fundamentals and sound business models. Rather than following the herd, Carlos leveraged the volatility as a source of additional alpha generation. By staying disciplined, closely monitoring his investments and adjusting his strategy when needed, he was well positioned to capitalise on these mispriced assets during the subsequent recovery, thereby leveraging uncertainty as a friend. Similarly, during the Covid-19 pandemic, the team swiftly repositioned the portfolio, seizing the opportunity to add high-quality companies from our watch list. These companies were being unfairly dragged down by market sentiment. This timely and strategic response, we believe, contributed significantly to the fund’s strong outperformance.

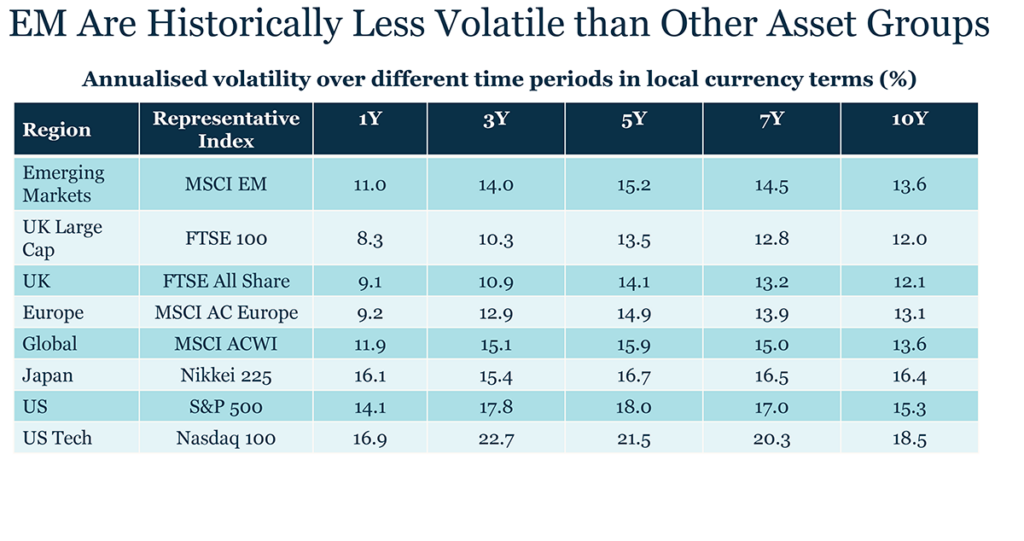

Interestingly, over the past decade, US equities have been more volatile than emerging markets in local currency terms. One reason could be the high concentration of the US market. Since 2014, big tech companies have rapidly increased their market dominance, with the ‘Magnificent 7’ now accounting for around 30% of the S&P500. In a highly concentrated market, sell-offs can become more severe as many investors rush to offload the same stocks, leading to outsized losses for those who remain invested. Historical examples have showcased the risks inherent in highly concentrated markets. For example, the dotcom bubble era was dominated by five tech stocks, which were quickly sold off when the bubble burst, contributing to the 78% loss in the Nasdaq index from its peak in March 2000 to its low in October 20021.

Source: FE Analytics

Market Concentration and Volatility

While the high concentration of the US market is widely recognised, many investors do not realise that the situation is similar in emerging markets. In the MSCI EM Index, the top 10 companies account for approximately 25% of the total index weight, despite there being around 1,300 constituents in total. In addition, many of the bulge-bracket EM funds’ portfolios are similarly concentrated in these top 10 names, potentially increasing their vulnerability to significant drawdowns during market sell-offs. This highlights the importance of portfolio diversification. We prefer smaller, lesser-known innovative companies in emerging markets, particularly in sectors like AI and the semiconductor supply chain, which we believe have a strong potential to deliver alpha.

Monetary Policy, Volatility and Emerging Markets

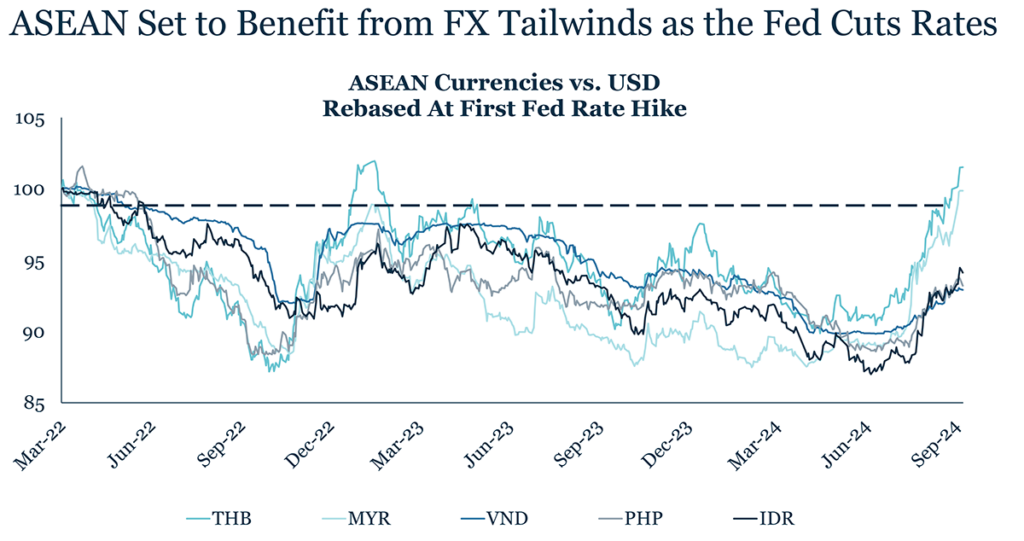

One of the main sources of volatility this year has been the Federal Reserve’s decisions regarding interest rate cuts. While the pace of future cuts and any unexpected employment or inflation data may continue to cause market fluctuations, the direction is now clear with the first cut behind us. Our focus, however, remains on the impact of these rate cuts on emerging markets rather than the short-term volatility around Fed meetings. With rates trending lower, as demonstrated by the Fed’s half-point cut on 18 September, we believe emerging markets are poised to benefit. Lower interest rates in advanced economies typically weaken the dollar, which in turn supports EM currencies and eases the burden of dollar-denominated debt.

Since 1988, EM equities have, on average, outperformed DM equities in 4/5 Fed rate-cutting cycles returning 29% in the 24 months following the last Fed rate hike2. Moreover, while many LatAm countries are ahead in the rate cutting cycle, Asian countries have been more cautious. Fed cuts now give many of them more room to begin their respective cutting cycles, thereby enabling cheaper borrowing, improving consumer sentiment and corporate spending, and stimulating growth.

Source: Maybank Research, Bloomberg, local sources. As of September 2024.

In addition, lower US interest rates can benefit emerging markets by reducing the attractiveness of safer, lower-yielding assets in developed markets, encouraging investors to seek higher yields in EM, increasing FDI flows and supporting EM asset prices. However, this impact varies across emerging markets as increased risk appetite and lower US yields cannot offset poor macroconditions or weak corporate fundamentals. For example, in the rate-cutting environment of 2019, Taiwan saw strong FDI inflows of $8.2bn, up 16% from 2018, while Argentina, with weaker fundamentals saw a 43% drop in FDI to $6.7bn3. Therefore, maintaining a robust macroeconomic overlay, combined with diligent stock selection, remains essential. This approach focuses on companies with strong fundamentals and resilient business models that can capitalise on a lower interest rate environment.

Volatility around Elections

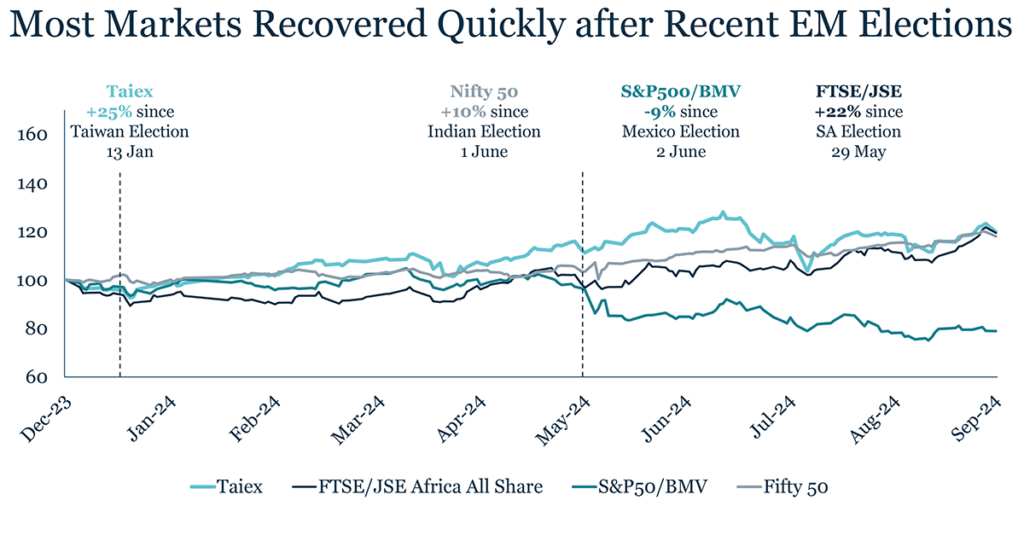

The global election year, seeing more than 60 countries and two billion people participating in elections4, has provided an additional source of volatility as uncertainty over new governments and policy directions incites investors’ fear of the unknown. However, most of the elections in emerging markets this year have not led to significant long-term spikes in volatility as the results have largely maintained the status quo in government policy. While initial declines in equity markets were mostly brief and quickly reversed (Mexico being one exception) some elections have even reduced local market volatility, with South Africa being a good example.

The US election remains a major source of uncertainty, more so than local EM elections, and will probably cause short-term market fluctuations in the lead up. However, historically, volatility tends to decline after the election announcement as uncertainty is reduced and, in fact, the MSCI EM Index often shows positive performance in the 100 days following the election announcement. The long-term impact of the new government’s policy direction, particularly on the strength of the USD and foreign policy, is what is most crucial for emerging markets. Donald Trump has perhaps been a more vocal proponent of protectionism, proposing extreme measures, including minimum tariffs of 60% on Chinese goods, 10% tariffs on global imports and, most recently, 100% tariffs on countries that turn from the US dollar. However, Joe Biden has retained and expanded many of the tariffs implemented by Trump during his presidency, reflecting a rare area of agreement between the two adversaries and a broader US shift towards de-globalisation and protectionism. Given Kamala Harris’s role as Vice President in implementing and expanding key protectionist policies such as the Inflation Reduction Act (2022) and the CHIPS and Science Act (2022), significant changes in trade policy may not be expected if she takes office.

Source: Bloomberg, figures are calculated from the first trading day after each country’s final election to 30 September 2024.

As a result, we expect friend shoring and nearshoring to continue driving capital into regions like Mexico and ASEAN, particularly in their manufacturing sectors. Additionally, the US’s decoupling from China is likely to strengthen ties with allies such as Taiwan and South Korea for semiconductor chips, and with South American and Eastern European countries for raw materials such as lithium, benefiting these emerging markets’ respective industries.

Geopolitics and Volatility

Geopolitics has long been, and is likely to remain, a significant source of volatility in global equity markets. No market, whether developed or emerging, is immune to the impacts of geopolitical events such as trade wars, ongoing conflicts or rising regional tensions. We believe the key to navigating these shocks, much like economic crises, is to stay disciplined by continuously monitoring the situation, staying informed and revisiting and reconfirming every single investment case as circumstances evolve. A disciplined macro-overlay is essential in emerging market investing, even for bottom-up stock pickers like ourselves. This approach has allowed us to effectively navigate and mitigate risks associated with major geopolitical events. For instance, we had no exposure to Russia during its invasion of Ukraine, driven by concerns over governance issues and the regulatory environment.

We closely monitor the relationship between China and Taiwan and believe that China will continue to focus on its own economic priorities in the near future, such as the overcapacity in the property market and high unemployment levels, and the recent measures to boost the economy seem to confirm this. Meanwhile, our exposure to Taiwanese companies is limited to asset-light businesses or those with a well-diversified global production base, providing some downside protection in the event of an escalation.

Conclusion: Stay Calm and Carry On

The bottom line is to stay disciplined and maintain a long-term perspective as markets tend to mean revert. Therefore, we believe by focusing on quality fundamentals rather than short term trends, volatility can be more effectively managed and even leveraged. In addition, falling interest rates have put EM back on the table as an attractive investment case for many, but we believe it is important to optimise EM investments via under-covered and mispriced small and mid-cap companies that will benefit from growing trends, such as AI, renewables and the growing consumer and middle classes, as well as diversifying your portfolio beyond the most concentrated stocks.

AI has been around since the mid-20th century, with Alan Turing, often regarded as the father of AI, introducing the Turing Test in his paper “Computing Machinery and Intelligence”. This is a method for determining if a machine can exhibit human-like intelligence, involving a human judge asking the same questions to a machine and another human; if the judge cannot distinguish which responses were provided by the machine or the human, the machine is said to have passed the test.

Turing’s work paved the way for artificial intelligence, first giving life to traditional AI which processes input databased on pre-defined patterns to make decisions. This technology is now ubiquitous in everyday life, seamlessly integrated into various applications like Spotify recommendations and online chess opponents. Today, Turing’s ambitions are even closer to being realised with the advent of generative AI which can create novel content based on its data inputs, making it vastly more sophisticated than traditional AI with potentially limitless use cases.

It was in fact the launch of Chat-GPT in November 2022 that show cased the unprecedented capabilities of Gen-AI on a global scale. Since then, we have seen the emergence of a large number of AI start-ups, accompanied by huge investments from both investors and large tech companies. This boom is reflected in the staggering growth of private sector spending on Gen AI-centric systems, which is expected to rise from $14 billion annually in 2020 to $137 billion annually by 20241.

Just as the advent of the factory may have been unimaginable to the 16th century peasant, or the advent of Chat-GPT may have been unimaginable to Turing’s peers, it is thought that Gen AI will lead to similar transformative inventions leaving no industry or corner of the globe untouched, hence Nvidia’s CEO Jensen Huang apt description of us witnessing “the dawn of anew industrial revolution”. A compelling example of Gen-AI’s potential to revolutionise an industry is in healthcare, where it promises ground breaking advances in medical treatment, diagnosis, distribution, vaccine development, and more. For example, early studies indicate that Gen-AI has the capability to detect early signs of breast cancer that may not be visible to the human eye. Given that approximately 13% of breast cancers go undetected by mammography2, a technology capable of reducing these omissions could potentially save millions of lives worldwide.

While there is no universal consensus on how much Gen-AI will contribute to productivity growth, numerous studies and forecasts highlight substantial contributions. For example, Goldman Sachs predicts Gen-AI will boost productivity growth by 1.5 percentage points over a 10-year period from 2023, and BCG estimates that productivity gains in the public sector will be valued at $1.75 trillion per year by 2033.

Estimates of Gen-AI’s contribution to economic growth also vary widely but all represent significant figures. Goldman Sachs estimated that Gen-AI will drive a 7% increase in global GDP between 2023-32. Meanwhile, JP Morgan estimated a wider range of a 7-10% increase over the same period. However, nearly all forecasts align on the industry’s Compound Annual Growth Rate (CAGR) which is being estimated at between 35-45% over 10 years, an impressive figure that underscores the opportunities for long-term investor returns.

Given this trajectory it is unsurprising the technology has been a major driver of investment this year. However, there are and will continue to be losers as well as winners in the AI story. The key is not only recognising today’s obvious winners, companies like Nvidia, which now have the downside of increasingly expensive valuations, but also identifying undiscovered, innovative companies with competitive edges that play lesser known, yet vital roles in the Gen-AI industry. Focusing on the semiconductor industry reveals that emerging markets are crucial for diversified exposure to the Gen-AI industry.

Countries like Taiwan and South Korea have established dominant positions in semiconductor manufacturing through a medley of factors, including decades of state-directed incentives and tax advantages, a favourable talent pool, a strong work ethic culture, and robust infrastructure. Today, Taiwan, ‘the Silicon Valley of the chip industry’, produces 60% of the world’s semiconductor chips and 90% of the most advanced ones3.

Accordingly, Taiwan, the Fund’s largest exposure (20.4% as of 28 June 2024), delivered a total return of 17.7% over Q2 2024. While the media often portrays US companies like Nvidia and OpenAI as epicentre of the Gen-AI industry, at MCP we recognise that these companies rely on the semiconductor manufacturers in EM which play a crucial, but perhaps less visible, role in the industry.

The complex semiconductor supply chains in emerging markets have led to a large universe of under-researched companies. Given their limited coverage by sell-side analysts, MCP researches investment opportunities within a diverse array of overlooked segments of the supply chain, including providers of niche components and equipment such as CPU sockets, CCLs, and connectivity solutions, as well as leaders in the IC design and semiconductor testing fields. MCP aims at identifying the market leaders in these sectors – companies often recognised as preferred vendors to industry giants for outsourced chip components and services. These companies typically operate in oligopolistic markets characterised by high barriers to entry due to their deep specialisation and have strong balance sheets, robust fundamentals and deep moats. A prime example of this type of company is Taiwan-based Lotes which we recently added to our portfolio (see company spotlight in MCP Manager’s Commentary Q2 2024).

Additionally, several other emerging markets are positioning themselves as the next leaders in the semiconductor and Gen-AI industries, perhaps most notably India. In February, the Indian government approved a $15 billion investment to build three new semiconductor plants, including its first semiconductor fab facility: a move to kick-off its journey to becoming a semiconductor manufacturing hub4. Additionally, the authorities have attracted tech companies to set up operations in India through incentives. For example, Microsoft has pledged $3.7bn to Telangana, and Amazon is planning on investing $12.7 bn in cloud infrastructure by 20305. We see this as a reflection that innovation and leadership in Gen-AI and related industries not only stretches beyond the US, but also stretches far across EM.

Once Gen-AI has been developed at the hardware level, it can be applied to various software applications in almost any industry. We are proud that almost all of our portfolio companies are embracing the technology and implementing it in their processes and software to improve operations, efficiency and productivity. Moreover, the software companies that are offering Gen AI products that help businesses to implement Gen-AI within their systems provide another type of AI exposure. Persistent Systems for example has earned the title of Generative AI Market Leader in the HFS Horizons: Generative Enterprise™ Services 2023 Report, which evaluated 35 service providers’ generative enterprise services.

Overall, we believe the generative AI industry has a bright future. While there will be obstacles along the way (e.g. environmental and safety concerns), the industry is set for significant growth. However, simply jumping on the Gen-AI bandwagon will not result in a surefire success story. Reflecting on the years of the internet boom, we see that the long-term trajectory of the industry will likely result in different winners and losers compared to those of today. At MCP, we identify under-researched companies in emerging markets which we believe are today’s innovators, and tomorrow’s winners of the Gen-AI story.

To find out more about portfolio manager Carlos Hardenberg’s and the MCP team’s insights into the Gen-AI industry, listen to Gen-AI, Beyond the Hype. This episode is part of our podcast channel, Insiders and Outliers -MCP on Emerging Markets, available on Spotify, Apple Podcasts and Soundcloud.

After a six-week period, India finally received its much-awaited election results on 4 June. Incumbent Narendra Modi and his party, the BJP, won 240 seats, failing to maintain the absolute majority they have enjoyed since 2014. However, the BJP’s wider alliance, the NDA, secured 292 seats, surpassing the 272-seat majority mark. As a result, Modi will remain the prime minister of the world’s largest democracy, leading a coalition government in which the BJP relies on smaller parties within the NDA.

Source: Citi Research, ECI

Over the past decade, the BJP’s pro-business agenda has proven to be highly popular among investors, making this week’s result a shock and disappointment for many who are worried about pro-business policy continuity. The party has implemented a wide spectrum of reforms aimed at prioritising economic growth, maintaining low inflation, ensuring fiscal prudence, boosting exports, attracting FDI and improving foreign relations. Here we list some of the party’s most significant reforms:

Make in India, 2014.

Promoting Manufacturing and Infrastructure

This multi-faceted initiative aimed to make India a manufacturing hub, particularly in electronics, whilst upskilling its labour force and attracting domestic and foreign investment into 25 key sectors, such as automotive and textiles. It included simplifying regulations and reducing red tape to improve the ease of doing business. Additionally, it placed a crucial emphasis on improving infrastructure through increased investments, as well as opening previously restricted infrastructure sectors to FDI, such as railways and construction.

Throughout its tenure, the BJP has intensified its efforts to develop electronics manufacturing along with semiconductor manufacturing, introducing further schemes such as the Production Linked Incentive scheme (2020) and the Semiconductor Mission (2022). These initiatives have attracted international businesses such as Apple, which aims to manufacture 1/4 iPhones in India by 2025, along with Taiwanese Powerchip Semiconductor Manufacturing Corp, Japanese Renasas, and Thai Stars Microelectronics, all of which are supporting the construction of India’s first three semiconductor fabrication facilities this year.

These initiatives reflect the agenda of the BJP in government over the past decade in which they have significantly increased capital expenditure across various sectors, not limited to manufacturing alone. This government has helped to drive investment, stimulate job creation, bolster consumer demand, and place India as a robust and stable alternative for countries looking to diversify their supply chains.

Source: Reuters, Indian Budget documents/speeches

Goods and Services Tax, 2017.

Reforming Tax

Another key reform is the Goods and Services Tax (GST) which consolidated the numerous cumbersome indirect taxes at both Central and State levels into one simplified and unified national tax framework. This overhaul not only streamlined tax processes but also accelerated the transport of goods and enhanced logistics efficiency by eliminating state barriers and reducing compliance burdens, measures particularly important in a country as large as India.

Furthermore, the GST has increased tax collections by broadening the tax base, integrating more businesses into the formal sector, and increasing tax compliance and administration efficiency. Since its inception, GST collections have consistently followed an upward trajectory, increasing from an initial Rs 92,283 crore in July 2017 to its highest yet of Rs2.1 lakh crore in April 20241. This has ensured fiscal prudence alongside the government’s increased capital expenditure on reforms such as Make in India. The government’s fiscal prudence is evidenced by the FY2023-24 fiscal deficit of 5.6% betting the forecast of 5.8%, according to recent data released by the CGA. Moreover, it is projected to further reduce to 5.1% this financial year2.

Source: PIB, WorldBank, Make in India

Technology Incubation and Development of Entrepreneurs (TIDE 2.0), 2019.

Encouraging Innovation

The Ministry of Electronics and Information Technology under the government launched TIDE 2.0, an upgrade of the original TIDE project launched in 2008. This initiative supports startups involved in emerging technologies like IoT, AI, and blockchain through technical and financial assistance. TIDE 2.0 reflects the government’s commitment to positioning India as a global hub for science and technology and fostering a favourable business ecosystem for innovative startups.

Source: World Intellectual Property Organisation

How will the election result impact the Indian market moving forward?

Modi will inevitably face greater challenges in passing certain business reforms this term. Unlike his previous two terms, he now must juggle the demands of allies with differing policy priorities to maintain a stable coalition, which may stymie the progress of certain business reforms. Vulnerable pipeline reforms include his land and capital reforms, the Uniform Civil Code, and the One Nation One Election initiative. On top of this, India may witness an increase in populist measures, such as unemployment reforms and higher rural spending.

However, a coalition government does not spell the end for pro-business reforms. Many of Modi’s core allies have a strong pro-business track record in their respective provinces. For example, Chandrababu Naidu of the TDP, who served as Chief Minister of Andhra Pradesh (1995-2004, 2014-2019), prioritised making the state an FDI and technology hub during his tenures. Progress is expected to continue in key areas such as manufacturing, regulatory improvements, labour law implementation, job creation, and workforce upskilling. Furthermore, the business reforms of the past decade will continue to drive India’s impressive economic growth, with an 8.2% GDP growth in FY2023-24, making it the fastest-growing major economy. The Reserve Bank of India recently raised the FY2024-25 real GDP growth forecast from 7.0% to 7.2%, highlighting the country’s ongoing growth prospects. Further still, the result does not undermine macro tailwinds such as India’s demographics, including a growing talent pool and consumer market, as well as its favourable position as the world looks to diversify supple chains.

Source: IMF, April 2024 Outlook

The Nifty 50 saw a sharp 6% drop on the day of the result3, the steepest decline in two years. Stocks in sectors such as PSUs and realty, which have benefited from the general market optimism and were trading at high valuations despite average fundamentals, were most affected by the volatility, which was largely a correction from the previous day’s rally and a short-term sell-off on unfulfilled expectations. By 7 June, the Nifty 50 had already recovered all of its election day losses and we expect the Nifty 50 and Sensex 50 to continue their strong performance so far this year, up 7% and 8% respectively4 (as of 7 June 2024).

This week’s election result has not affected our bullish view on India. Our conviction in India’s long-term growth story has further strengthened over the past year, leading MCP to add three new high-conviction Indian ideas to the portfolio. A two-month trip by an MCP analyst to meet with companies and experts on the ground reinforced our bullish view. We believe India’s journey to become one of the world’s great economic powerhouses will not be undone by a single election result.

The history of semiconductors dates back to the 19th century, marked by Karl Ferdinand Braun’s discovery of rectification in 1874. Practical applications then emerged in the early 20th century, such as the cat’s whisker detector, a rudimentary semiconductor device used in early radio receivers. This device consisted of a thin wire, or ‘whisker’, that made contact with a semiconductor crystal, such as silicon, to detect and convert electrical signals into audio signals.

Since its inception, the industry has been characterised by cyclicality as well as its relentless pursuit of innovation, defined by Moore’s Law, which states that the number of transistors on computer chips double every two years with little change in price. Of course, the industry has come a long way since those first primitive semiconductors and their applications, and continuous advances have given way to semiconductors so sophisticated that they have become indispensable to the functioning of modern society. The industry’s rapid evolution is reflected in its staggering growth, with annual sales quadrupling in just two decades – soaring from $139 billion in 2001 to $573.5 billion in 20221. This rapid growth is well illustrated by the development of ASML’s market capitalisation below.

Cyclicality and Semiconductors

Most recently, the semiconductor industry has faced global supply chain disruptions, triggered by the Covid-19 pandemic. While some sectors, notably automotive, faced reduced orders, most, such as consumer electronics, saw unprecedented growth due to the shift to remote working. US sanctions on companies with ties to China, combined with factors such as the 5G rollout, the Russia-Ukraine war and severe weather events, added to sector volatility. Semiconductor manufacturers responded to heightened demand during the pandemic by increasing inventories, supported by government subsidies. However, the end of the consumer electronics replacement cycle resulted in an industry slowdown in the latter half of 2022 and excess chip inventories.

A year later, inventory levels stabilised, particularly in the global IT components sector, marking a turning point in the cycle. TSMC’s revenue, a key indicator of industry health given they manufacture around 90% of the world’s advanced chips, rose by 14.4% in Q4 2023 from the previous quarter2. Some concerns persist regarding oversupply, especially for foundational chips, as Chinese chipmakers continue to increase production. Nonetheless, the industry is expected to maintain its upward trajectory, with sales revenue estimated to reach between US$588-613 billion in 2024, surpassing 2022’s record of US$574 billion, and 2027 forecasts come in around US$736.40 billion3.

Geopolitics and Semiconductors

The global shortage of semiconductors provided a wake-up call for many governments, particularly in the US and Europe as it served to highlight the vulnerability of over-reliance on the global supply chain. In response, governments began efforts to de-risk their supply chains through onshoring and nearshoring production. This trend has proved beneficial to some players in the supply chain as the total addressable market for existing suppliers increases in line with an increase in capacity and production. For example, Park Systems, which supplies wafer inspection equipment, is benefitting from the increasing demand of smaller nodes and the corresponding expansion of manufacturing lanes.

The US government’s 2022 CHIPS Act is a prime example of efforts to onshore. It allocated $52.7 billion4 in federal subsidies to support domestic chip R&D, manufacturing and workforce development. Just recently, President Biden announced up to $8.5 billion direct funding to US chipmaker Intel under the CHIPS Act to fund new chip plants in the US.

The US government-imposed restrictions on the export of advanced chips and chip manufacturing equipment to China in October 2022, and tightened the restrictions in November 2023. The move was intended to pre-empt the prospect of Chinese global dominance in the industry, as the Chinese government also sought self-sufficiency. However, the move has yielded mixed results. While it has hindered China’s progress in advanced chip manufacturing and AI development, leading to a focus on foundational chip manufacturing instead, it has likely accelerated China’s path to self-sufficiency by making this an even higher priority for Beijing and forcing Chinese companies to be more innovative in order to develop their own advanced chips. For example, in October 2023 Beijing announced a $40bn state-backed fund to boost the semiconductor sector, and at the same time, scientists at China’s Tsinghua University announced the development of the world’s first fully system-integrated memristor chip in October 2023, with significant applications in AI and autonomous driving5.

Semiconductors and Artificial Intelligence

In 2024, the consumer electronics sector is poised for solid growth with a forecasted 3.5% and 4% increase in PC and smartphone sales respectively according to Gartner. This upswing is fuelled in part by a new notebook renewal cycle, as well as a wave of smartphone replacements driven by on-device AI, which allows smartphones to process data within the device rather than on a remote cloud server; this reduces security issues and enables AI services without internet connection. This development, we believe, will benefit a number of our portfolio companies that cater to this industry. One example is Elite Material, a key supplier of high-density copper clad laminates, a crucial component used in advanced chip production. Another example is LEENO which is set to see higher revenue growth in 2024 given their significant R&D exposure to on device AI.

NVIDIA’s recent Q4 2023 report of a 265%6 increase in quarterly revenues from one year ago serves as a prime example of the substantial growth AI can drive, with CEO Jensen Huang asserting that AI has reached a ‘tipping point’. The seemingly limitless potential of the AI revolution will sustain growth in the semiconductor industry for years to come, benefiting well established companies like NVIDIA and Arm, as well as lesser-known businesses in our portfolio that cater to such industry giants.

eMemory Technology

Within the semiconductor industry, eMemory, a world-leading IP provider to over 2,400 foundries, IDMs and fabless companies, is a prime example of the type of company we like to invest in, with deep moats, sound balance sheets and a strong outlook based on sustainable growth and expansion. In a recent quarterly earnings call, chairman Charles Hsu summarised their strong growth potential: ‘‘Our total addressable market will increase as the world expands foundry capacity and move toward more advanced technology. Our technology coverage in each foundry will increase as more technology processes develop and more fabs are established.’’ To this end, the company has several advanced 3/4/5nm semiconductor projects underway and has successfully licensed its 3nm OTP and PUF technology to a US foundry customer with whom it will work to develop the most cutting-edge processes. In addition, the royalty income for each foundry is increasing, as is the demand for licensing, resulting in increased licensing income, all of which increases eMemory’s profitability.

The promising outlook for eMemory, which will very likely profit from both increasing semiconductor capacity and complexity, is reflected in the positive outlook for many of our other portfolio companies. For example, LEENO, (see Company Spotlight in our Q1 2024 Manager’s Commentary) should be benefiting from the increasing complexity of chips, which require more advanced pins and sockets for testing in the R&D phase.

Outlook

The expanding total addressable market of semiconductor end markets, facilitated by this expansion in semiconductor capacity and complexity, suggests we may come to see a potential reduction in the industry’s cyclicality. The industry may become increasingly shielded from the vulnerabilities associated with single market trends with dampened demand in one sector likely having a less pervasive effect on the overall semiconductor industry and its supply chain. Furthermore, many of the new end markets, such as automotive, industrial automation, 5G infrastructure, AI and cloud computing, have larger chip demands per unit compared to those associated with consumer electronics. The outlook for the semiconductor industry is positive, not just for 2024, but for the next decade. Despite historical peaks and troughs, the industry’s overarching trend is one of exponential growth, with forecasts pointing to a milestone of $1 trillion in market revenues by 2030.

At MCP, we avoid trying to time each cycle perfectly and instead focus on identifying highly innovative companies that are positioned to benefit from the industry’s long-term trends, such as eMemory. This strategy does not begin and end with the semiconductor industry, but extends to all the industries in which we invest. In this way, we aim to create long-term, sustainable value for our investors.

To find out more about portfolio manager Carlos Hardenberg’s and the MCP team’s insights into the semiconductor industry, listen to Decoding the Semiconductor Industry. This episode is part of our new podcast channel, Insiders and Outliers – MCP on Emerging Markets. Monthly episodes are available on Spotify, Apple Podcasts and Soundcloud.

On 26 February 2024, South Korea’s Financial Services Commission (FSC) together with the Korean Exchange (KRX) announced the country’s Corporate Value Up Programme. Similar to, and most likely inspired by, Japan’s decade-long initiative, the aim is to raise valuations and boost shareholder returns. This is a move to address the so-called ‘Korea discount’ where listed companies tend to have lower valuations compared than their global peers. In fact, over two thirds of listed companies on the Kospi have a price-to-book (P/B) ratio of less than 11.

Source: Bloomberg

A significant contributor to the Korea discount is weak corporate governance standards, particularly within the notorious chaebols – wealthy and influential family-owned conglomerates like Samsung, Hyundai Motor and LG. Chaebols have traditionally prioritised maintaining control over maximising shareholder value and including minority shareholders in active participation. One notable example is the deliberate suppression of company value to minimise the blow to the next generation when it comes to paying the hefty 50-60% inheritance tax. However, it’s important to recognise that while chaebols play a crucial role, there are other factors contributing to the discount, including traditionally low dividend payouts and inefficient asset utilisation among Korean companies.

The Corporate Value Up Programme is a set of voluntary guidelines encouraging companies to devise mid- to long- term plans and targets to increase shareholder value, with board members playing a key role in the implementation. Companies are encouraged to disclose these plans annually on the KRX website. Korean financial regulators have emphasised that there are significant financial incentives for companies to participate in the programme, claiming that the incentives will exceed those offered by Japan in its equivalent initiative. In addition, best practice companies (those with a proven track record of profitability or those that are expected to boost valuation) will be included in the upcoming Korea Value-up Index, the other major pillar of Korea’s efforts.

The Korea Value-Up Index, to be introduced in June, mirrors Japan’s JPX Prime 150 Index by including companies that are making efforts to improve their valuation. The purpose of the index is to create a market environment that promotes investments in such companies, makes them more accessible to retail investors and enhances market transparency. Pension funds and institutional investors will use the index as a benchmark, and ETFs tracking the index are expected to be launched by December. Evaluations of key financial indicators, including P/B ratio, price-to-earnings ratio and return on equity will be part of the index’s criteria. These indicators, along with dividend payouts, will be regularly published on the KRX website.

Concerns have been raised about the lack of detail in Korea’s Value Up Initiative, particularly regarding the unspecified tax incentives the FSC places great emphasis on. Another source of disappointment is the voluntary nature of the programme; without enforcement companies may not take decisive action to improve valuations, rendering the initiative meaningless. As a result, the Kospi Index fell by 0.8% on the day of the announcement2.

The FSC has responded to such criticism by stating that is it more realistic to provide powerful incentives than to enforce cooperation, and that final guidelines will be announced in June. The FSC has also stressed the importance taking a long-term view. Chairman Kin Joo-hyun stated that “enhancing the corporate value of a company is not something that can be achieved in a short period of time with only one or two measures.”

A look at Japan may help to better understand Korea and its initiative. Japan has faced similar challenges of low valuations and shareholder returns since its market crash in 1987. As a result, the country embarked on a corporate governance mission over a decade ago. Efforts ramped up last year when the Tokyo Stock Exchange (TSE) announced in March that listed companies with a P/B ratio of less than one must submit a plan to improve capital efficiency. In October, the TSE announced its ‘name and shame’ measure whereby from January 2024 it will publish a list of companies with poor shareholder returns that have disclosed these plans, thus indirectly calling out companies that haven’t. These efforts are finally bearing fruit as the Nikkei 225 hit a 34-year high on 22nd Feb closing above 39,000 points3. Many investors are putting Japan back on the agenda in 2024 after a 34-year hiatus.

So, what lessons can Korea learn from Japan? While Korea’s initiative may result in little change in the short-term, due to its unspecified and voluntary nature, it should not be deemed insignificant. Given that Japan’s reforms took over a decade to take effect, Korea’s equivalent reforms should not be expected to happen overnight but should be considered an important starting point for long-term improvements.

As China enters a new year it is fitting to draw a comparison with this year’s zodiac animal, the dragon. Undoubtedly, the Chinese economy could do with a bit of luck and strength, attributes associated with the dragon. However, the key question remains: will the market heat up or will investors just get burnt?

Rewind one year and investors were projecting a strong recovery in China given a long-awaited farewell to its zero-Covid policy. This optimism was short lived. The rally in China’s stock market quickly tailed off as structural problems became alarmingly apparent. Deep-seated problems in the property sector, with defaults by major developers led by property giant Evergrande, had a knock-on effect on domestic lenders. FDI flows, domestic manufacturing, exports and consumer spending all remained weak, exacerbating China’s deflationary cycle. Such issues left Chinese equities trading at record lows.

However, a closer look at key metrics could indicate a disconnect between market sentiment and the reality on the ground. Box office sales increased in 2023, domestic tourism is booming with planned travel expenditures for 2024 surpassing 2019 figures, and car sales are reaching unprecedented highs. These are all important signals for a potential rebound in consumer spending this year.

Furthermore, the Chinese government has initiated measures to strengthen domestic demand, support the stock market and shift away from an over-reliance on infrastructure and real estate investment. A recent measure by Beijing to mitigate selloffs in the market and promote stability comes in the form of increased purchases of onshore Chinese stock market ETFs by state and sovereign wealth funds.

While measures so far have fallen short of substantial fiscal interventions many investors hoped for, the cumulative impact of the government’s smaller-scale initiatives should not be ignored. Furthermore, China’s upcoming National People’s Congress (NPC) session on 4-5 March is a key annual meeting where economic and social development plans for the year will be unveiled. Analysts expect a GDP growth target of 5% and the announcement of further measures to boost growth, support demand and improve the business environment.

So, given China’s attractive valuations, improving consumer sentiment and increasing fiscal support, why do we continue to invest cautiously in China?

First of all, despite some positive signs, structural challenges remain. 70% of household wealth is tied up in property, and the crisis is by no means over. Property investment and new construction dropped 9.6% and 20.4% respectively in 20231. Furthermore, Evergrande’s liquidation order in January and the liquidation petition filed against Country Garden on 28th February are exacerbating the lack of confidence in the property sector. This may lead to an extended period of cautious consumer spending.

Additionally, the CCP’s intervention in the economy, coupled with lower corporate governance standards among Chinese companies compared to their Asian EM counterparts, continue to steer us away from direct investment in China. The CCP’s near destruction of the EdTech sector in 2021 is a prime example of the regulatory risks inherent in the country.

Finally, when it comes to companies, we rarely find the level of governance, fundamental quality and innovation that would meet our investment criteria. Instead, we prefer to access the Chinese market indirectly through countries such as Taiwan and South Korea which also benefit from improving consumer sentiment in China. For example, our portfolio includes Elite Material, a Taiwanese company specialising in components for the semiconductor industry. It operates manufacturing facilities across China and generates a significant proportion of its revenues in the country while offering Taiwanese standards of governance and transparency.

No investor can afford to ignore the world’s second largest economy and China is still forecast to grow by 4.6% in 20242, much faster than any developed market economy and many of its emerging market peers. So, we continue to scour the Chinese market for exciting companies that meet our quality investment criteria.

1 National Bureau of Statistics of China

2 IMF World Economic Outlook Growth Projections, January 2024

As we reflect on a volatile year 2023, we are reminded of the words of Winston Churchill: “A pessimist sees the difficulty in every opportunity; an optimist sees the opportunity in every difficulty.”

The year unfolded with global fears of inflation, coupled with concerns over the ongoing conflict in Ukraine and uncertainties surrounding the US and European economies. A sluggish recovery in China and unsettling events, such as the terrorist attacks in Israel and the ensuing conflict added layers of complexity and prompted cautious positioning by investors.

Since our launch in 2018, MCP has weathered a pandemic, geopolitical turbulence and economic shocks. Our strategic choices, based on a rigorous focus on quality, careful selection of management teams and business models, and a vigilant awareness of macroeconomic and company-specific risks, have steered us through these turbulent waters. We avoided investing in Russia and had almost no direct exposure to China. By taking advantage of the opportunities presented by market conditions, the Mobius Emerging Markets Fund (MEMF) has generated sustainable long-term returns, culminating in a five-year track record of significant outperformance, with return of 26.9% (Private C USD Founder, as of 29 September 2023) since inception compared with the MSCI EM USD Index return of -8.6%. In the current year alone, MEMF has outperformed the MSCI EM Index by an impressive 10% (as of 29 December 2023).

One of the exciting companies that have contributed to our success is Classys. Founded as a family business in Seoul in 2007, Classys is the global market leader (ex-US) in non-invasive medical aesthetic devices with a 30% market share. Its cutting-edge devices use high-intensity focused ultrasound (HIFU) and radio frequency (RF). Classys’ “razor and blade” business model, which sells both medical devices and cartridges, has led to continuous gross margin improvements. Although the company is already present in 70 countries, its expansion into the US and China offers immense growth opportunities. In the third quarter of 2023, Classys again reported robust results, driven by product innovation and geographic expansion, and has provided positive guidance for FY24.

This positive momentum is not limited to Classys; it is evident across our portfolio. In particular, our technology holdings are seeing inventories normalise and demand pick up. Our quality portfolio companies have demonstrated resilience and adaptability, and as business and consumer spending continues to improve, our companies will benefit from the recovery. Although developed markets outperformed emerging markets in2023, low valuations, a potentially weaker USD and expected higher growth suggest a positive outlook for emerging markets in 2024.

We recently announced Mark Mobius’ well-deserved retirement from Mobius Capital Partners. We would like to express our gratitude for his mentorship, leadership, and the remarkable energy and passion he brought not only to the business but also to our lives. The firm and its vehicles continue seamlessly under Carlos Hardenberg’s leadership, supported by our exceptional team of passionate and dedicated analysts. We are committed to continuing to deliver superior long-term returns over the next decade.

We thank you for your continued trust and support. As we embark on the exciting path ahead, we wish you a happy and prosperous New Year. Thank you for being an integral part of our journey.

We have recently returned from a research trip to India, a visit we had been very excited about as we had missed in-person interactions with our holdings and interesting businesses that we have been following for a while. While our regular calls and meetings in London have allowed us to stay in close contact, a personal meeting with CEOs and managers on site cannot be substituted.

India in the Portfolio

India has been an important allocation for the Mobius Emerging Markets Fund since its inception. MEMF’s Indian holdings have contributed 40% to (gross) return as of the end of March 2023. This was almost entirely driven by stock selection. Our visit has confirmed our bullish outlook on the region, and the exciting companies diligent stock pickers can find in India.

Some Important Facts about India

India, a country of 1.4 billion people, and soon expected to be the most populous country in the world, offers a plethora of opportunities for us as long-term, quality-oriented investors. Companies have evolved, are increasingly more professionally managed, and are focused on corporate governance and sustainability efforts, which has helped in attracting domestic and foreign capital flows. Innovation is omnipresent, and India has created 100 unicorns in the last five years. Unrelenting deal activity in PE and VC also means new and innovative businesses available to invest in as public market investors. There are over 6,000 listed companies in the small- and mid-cap space.

Source: Bloomberg, RBI

Growing Middle Class

In India, we observe income inequality and a changing social fabric, as in most other emerging markets, but are convinced that rapid income acceleration, technological adoption and corporate spending—aided by favourable economic and fiscal policies—will keep India on a steady growth path. GDP per capita has quintupled over the last 20 years. By 2030, the Indian economy will be led by the middle class, and upward income mobility will continue to drive consumption.

Source: Brookings Institution, as of 2020, People Research on India’s Consumer Economy. *Asterix indicates forecast

The Growth Premium

In its latest World Economic Outlook, the IMF forecast India to grow 5.9% in 2023 and 6.3% in 2024, more than any other major economy. This compares to 1.3% and 1.4% projected growth for advanced economies. The Indian economy clearly has recovered from the pandemic-related slowdown and is now on an impressive, sustained growth trajectory for the next decade. Growth will primarily come from the increase in private consumption (and we have witnessed this on the ground with busy markets and fully occupied restaurants and shopping malls) and will be fuelled by a broad-based expansion of capital expenditure by the private and public sectors.

Source: World Population Review, IMF World Economic Outlook Update April 2023

Supportive Government Policies

We view the recent economic policies—including increased spending on infrastructure, incentives to boost certain niche manufacturing segments, focus on improving ease of doing business and fiscal measures undertaken to keep inflation in check—largely positively. Shortly before our visit, India’s government announced a raise in capital expenditure of 33% to 10 trillion rupees ($122.29 billion) in the next fiscal year to drive investments in infrastructure. We witnessed first-hand rampant construction activity across the cities we visited. The scale of expansion of the Metro (public rail transport) is mind-boggling and is being talked about by everyone we met. Further, construction of new expressways, bridges and airports continues to support the public infrastructure and we see this as a good indicator of the economic growth the country is witnessing.

Source: Bloomberg, Macquarie Research, As of 28 February 2023 (FY -> Apr – Mar)

Digitalising the Financial System

Another key driver of economic growth is a healthy credit cycle with multiple banks competing and lending activity again on the agenda. Our interactions with small and large banks also point to the good health of corporate credit in India which is the cornerstone of future expansion. India’s financial system has made significant progress in efficiency with technology and innovation becoming mainstream. The digital payment system UPI is basically used by every Indian and has almost replaced cash entirely (UPI enabled approximately 2,300 transactions a second in 2022). Ever-increasing smartphone penetration, combined with the government’s efforts to reduce cash transactions, has brought the majority of the population into the digital payment ecosystem. As a result, about 80% of Indians own a bank account today, a significant change from only five years ago.

China plus 1

During our visit, the world was surprised to learn about one of the largest airplane deals in recent history with Air India (the erstwhile national carrier, now owned by the Tata Group, among India’s largest conglomerates) ordering over 400 planes from Airbus and Boeing. Our visit also coincided with several global investor summits and G20 meetings and we constantly heard of the large-scale investments across diverse sectors such as manufacturing and renewable energy. India’s recovery and robust position is clearly no secret, and a term we heard everywhere was ‘China plus 1’. Although we don’t invest directly in airlines, infrastructure or asset-heavy manufacturing companies, we have found small businesses that fit our quality criteria and are poised to benefit from these sectoral tailwinds. As part of our research, we met over 20 companies during our trip in addition to economists, local fund managers, entrepreneurs and private investors.

Source: Ministry of Finance (India)

Our Portfolio Holdings

The most satisfying finding from our trip was that our holdings are doing even better than we had expected. APL Apollo Tubes, one of our key holdings for over three years, had just reported its highest ever quarterly volume of 600k tons of steel tubes. The passion and the vision of the founder MD, his attention to detail and strong intent to professionalise the organisation with the right talent, continues to impress us. We are firm believers in investing in companies with good culture and this meeting with the MD reaffirmed APL’s focus on their culture—employees are considered family. During the visit to the warehouse of a distributor to APL for 10+ years we clearly saw the brand appeal and scale of distribution of APL Apollo superseding that of their peers. At a visit to one of their plants, we witnessed the highly efficient manufacturing process with >90% of energy needs met through renewable energy.

A key holding—and one of the top performers for us since inception—is Persistent Systems, a global digital engineering company that differentiates itself from the other IT companies in India by catering to a niche customer segment. Despite the macro headwinds, Persistent continues to be among the fastest growing companies and has kept up its trajectory of new deal wins. All our interactions with competitors and other investors highlighted the quality of management, the recent success in reorganisation and its ability to continue to grow in a difficult market. We remain firm believers in their long-term success and have successfully engaged with the company on various initiatives over the years.

A New Investment

We continue to find similar promoter-run businesses in India led by professional management teams and with a clear succession plan in place. One such new addition to our portfolio is CE Infosystems (MapMyIndia), a small yet exciting business that is a domestic leader in providing geospatial technology and automotive navigation solutions in India (please also see Company Spotlight above). Our interactions with the founding family—including the CEO and the heads of different businesses who have been with the company for over 10 years—highlighted the importance of culture in the organisation. Promoters have gradually transferred ownership in the form of ESOPs to key employees, even before ESOPs became common among tech companies in India. Coincidentally, CE Infosystems was celebrating its 25th anniversary on the day of our visit and were preparing for an organisation-wide cricket tournament. After our visit to their experience centre and the interactions with the team, we walked away with the feeling that they can innovate continually and combat disruption, while maintaining their sticky customer base.

Conclusion

India will remain an exciting country for us, and we will watch closely as the country is headed into elections in May 2024 during which the incumbent government needs to successfully navigate current economic headwinds for a third victory. During our trip we identified new potential investments in niche segments within financials, manufacturing and technology sectors which would benefit from the longer-term opportunities the country offers across consumer and corporate spending.