In contrast to previous years, when MMIT delivered strong returns driven by small- and mid-cap emerging market companies despite broader EM equities lagging, the asset class entered a recovery phase in 2025. Emerging markets demonstrated to global investors that they can deliver strong returns in a market previously dominated by American exceptionalism.

However, the benefits were largely captured by a small number of mega-cap stocks, resulting in unusually narrow market leadership. While gains have been highly concentrated so far, a broader set of supportive dynamics for emerging markets should increasingly extend beyond the largest stocks and benefit quality small- and mid-cap companies.

At the same time, many of our holdings have continued to execute well operationally, but this has not been fully reflected in share prices due to macroeconomic headwinds. As these pressures ease, we see scope for a catch-up in valuations, providing support to the portfolio in the years ahead.

Emerging Markets Supported by Numerous Tailwinds

Source: Bloomberg, Research Affiliates (RA) Asset Allocation Study. As of 31 December 2025.

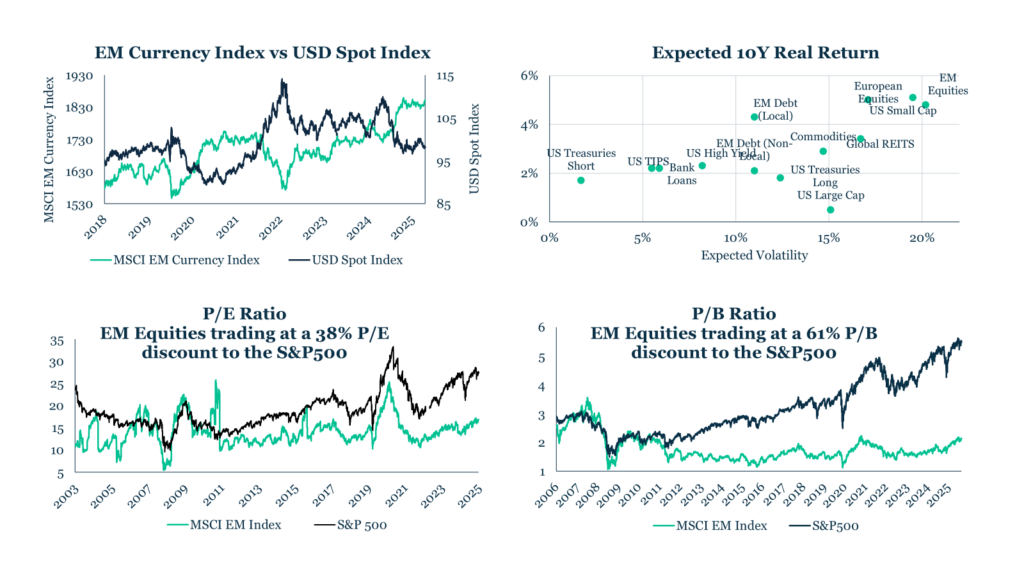

At year end, emerging markets were trading at a 38% discount on a P/E basis and a 61% discount on a P/B basis relative to developed markets. These valuation gaps are particularly pronounced in the sectors we focus on, such as technology and consumer discretionary. Importantly, the attractive discounts noted above are also increasingly evident across quality stocks, extending beyond traditional value segments.

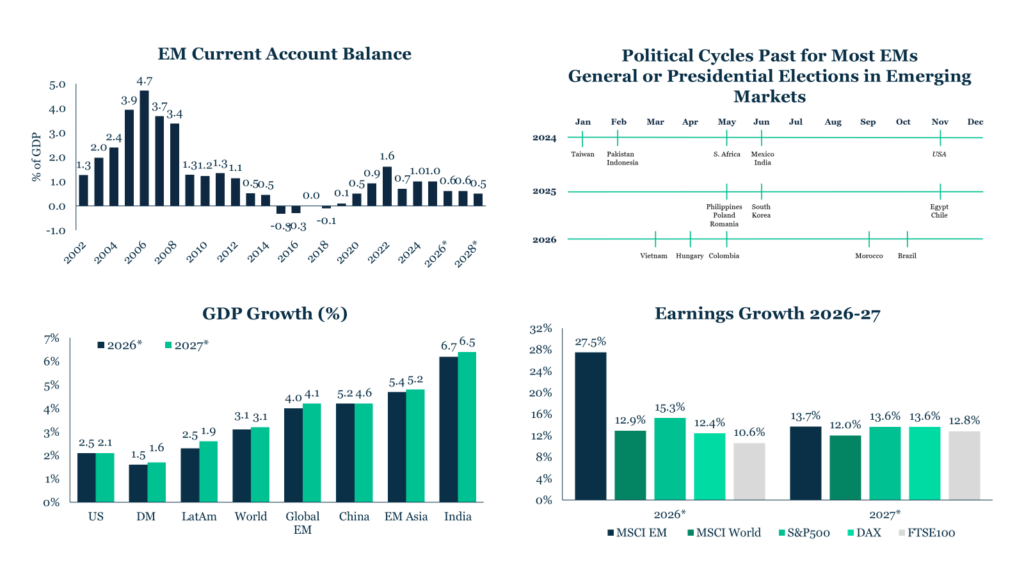

Furthermore, emerging markets are supported by a 9.4% weakening of the US dollar in 2025, which is expected to continue into 2026. This typically benefits EM currencies, with the Brazilian real, Colombian peso and Taiwanese dollar among the strongest performers this year. EM bond spreads are also near some of their highest levels. Emerging markets continue to maintain healthier debt levels than developed markets (69% versus 109% of GDP in 2024), while simultaneously offering stronger GDP and earnings growth projections.

Higher Growth in EMs Combined with Healthier Debt Levels

Source: IMF WEO October 2025, Bloomberg. * indicates forecast.

Political risk related to elections is currently cyclically low, with major electoral events in 2026 limited to Vietnam and Brazil across our key markets. However, geopolitical risks more broadly remain elevated. Recent developments, including tensions between the US and Europe over Greenland and events in Venezuela, have already added complications to the outlook for 2026, alongside long-standing risks such as the Russia–Ukraine conflict, instability in the Middle East, global trade wars, and ongoing tension between China and Taiwan. We remain highly mindful of geopolitical risks and always apply a macro risk overlay to our bottom-up stock selection.

The Federal Reserve’s expected rate cuts this year further enhance the outlook, as lower US yields generally push investors toward higher-return emerging market assets—particularly as many EMs benefit from moderating inflation and higher real rates themselves. While effects may vary across countries, the global easing cycle provides a broadly supportive backdrop for EM performance.

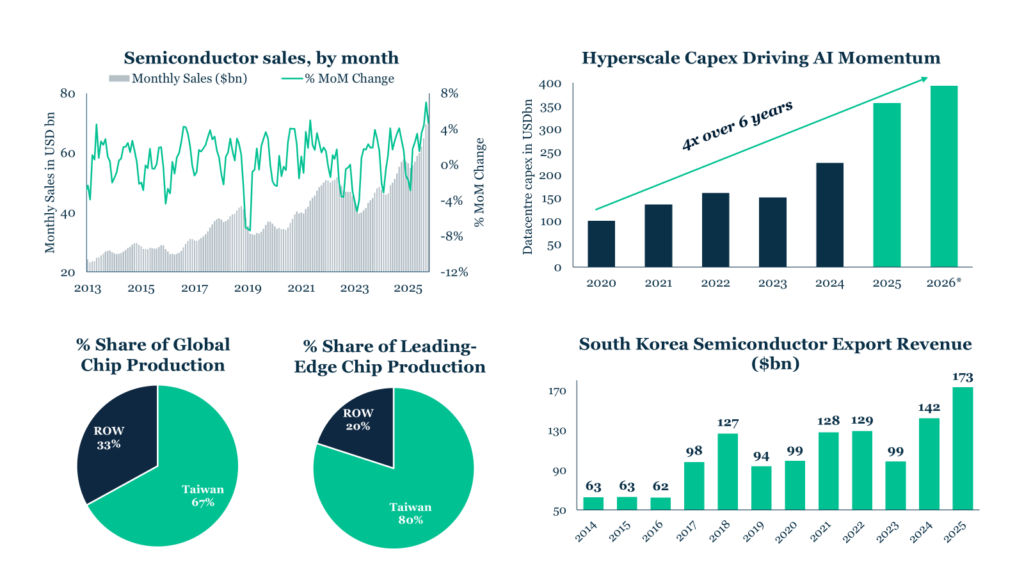

Furthermore, a number of country-specific tailwinds should support our portfolio exposures. Taiwan continues to benefit from a powerful semiconductor investment cycle and a globally competitive innovation ecosystem. South Korea is advancing structurally in high-end manufacturing, materials and automation, where we continue to find globally competitive businesses trading at attractive valuations.

Taiwan and Korea Well Positioned in Semiconductor and AI Markets

Source: Statista, Semiconductor Industry Association, Bloomberg, Economic Times, South Korea Ministry of Trade. * indicates forecast. Data as of 31 December 2025.

Despite a challenging start to 2026, marked by foreign outflows amid reduced risk appetite and heightened macro volatility following recent geopolitical developments, India’s longer-term outlook remains compelling. We continue to look through near-term volatility, supported by resilient GDP growth, rising discretionary consumption and improving capital expenditure trends. The year 2026 could turn into another period of significant progress for the country.

Brazil offers selective opportunities as inflation moderates, interest rates decline and corporate balance sheets strengthen. We remain cautious around the upcoming elections, which are likely to introduce additional volatility in 2026.

While emerging markets have delivered strong headline returns this year, dispersion beneath the surface has been significant. With valuation spreads at elevated levels and earnings revisions diverging meaningfully by country, sector and company, passive exposure increasingly reflects index concentration rather than the breadth of opportunity available.

In this environment, disciplined bottom-up stock selection is essential to identifying structurally stronger businesses beyond benchmark heavyweights. We believe the portfolio is well positioned should the recovery broaden into under-owned areas of the market where fundamentals remain intact.

With a portfolio built around high-quality, lesser-known companies and a disciplined, active approach to capital allocation, we remain fully committed to our investment philosophy and to delivering long-term performance and shareholder value.

Since the inception of the strategy in 2018, our objective has remained unchanged: to deliver long-term performance by identifying high-quality, innovative, under-researched mid-cap compounders with strong fundamentals that are not represented in the benchmark. This disciplined investment philosophy has driven strong results over prior years, culminating in 35.2% outperformance against the MSCI EM Mid Cap Index in GBP terms by the end of 2024.

However, 2025 played out differently, despite emerging markets finally ending a decade of underperformance versus developed markets. The year proved challenging in relative terms for the strategy, as the market environment was particularly difficult for quality-oriented mid-cap stocks. Returns were increasingly driven by a narrow group of large, liquid companies and by style dynamics that ran counter to our investment approach.

That said, Q4 showed early signs of stabilisation and improvement. Over the quarter, MMIT’s net asset value returned 2.5%, while the MSCI EM Mid Cap Index (Net TR) delivered a return of 2.2% in GBP terms. This relative improvement was supported by solid operational performance across several portfolio holdings, with a number delivering results ahead of expectations.

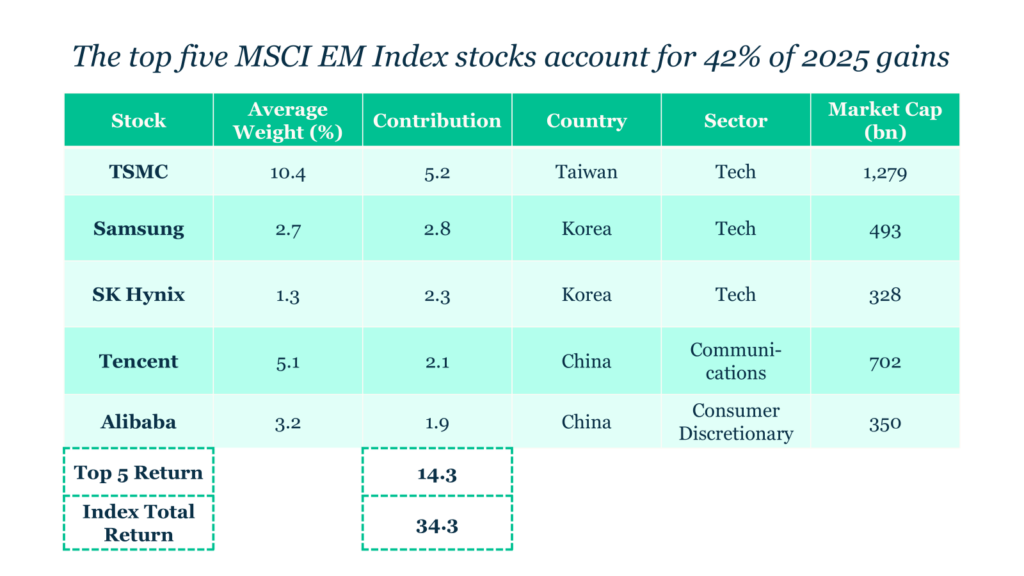

Emerging markets recorded steady gains over the quarter, finishing the year as the strongest-performing global equity asset class. As is often the case in the early stages of a recovery, initial inflows were concentrated in the largest and most liquid stocks. Within the MSCI EM Index, the top five holdings accounted for over 40% of total returns in 2025.

Performance in EM Driven by a Few Large Companies

Source: Bloomberg. As of 31 December 2025.

Our investment universe is deliberately focused on lesser-known, under-researched small- and mid-cap companies across emerging markets, where we believe our bottom-up research adds the greatest value by looking beyond well-known benchmark constituents. The under-researched nature of this segment—typically marked by limited coverage, lower visibility and minimal benchmark overlap—can give rise to pricing inefficiencies that are largely absent in the highly efficient mega-cap space.

Active management is more likely to add value in these less crowded areas of the market, where returns are driven more by company-specific fundamentals than by index flows. Against a backdrop of unusually narrow market leadership, we believe this positioning may offer meaningful potential for relative catch-up as fundamentals reassert themselves.

During 2025, the strategy’s emphasis on quality encountered significant style headwinds, with quality stocks—especially within emerging markets—suffering one of their worst periods of relative underperformance compared with the broader benchmark. Smaller companies, particularly growth-oriented businesses in the technology sector, were disproportionately affected by continued macroeconomic and geopolitical uncertainty.

Investor risk appetite remained constrained, with capital rotating towards perceived safe-haven assets such as gold and towards larger, more liquid equities viewed as more resilient in volatile markets.During this period, investors favoured sectors such as banks, commodities and defence-related industries, supported by higher interest rates, elevated fiscal and defence spending, and ongoing geopolitical tensions. This defence-led rotation provided relative support to parts of the industrials and commodities sectors.

These areas, which are deliberately excluded from the portfolio due to their regulatory complexity, capital intensity and limited pricing power, were generally trading at lower valuation multiples and tended to be more resilient during periods of market correction.

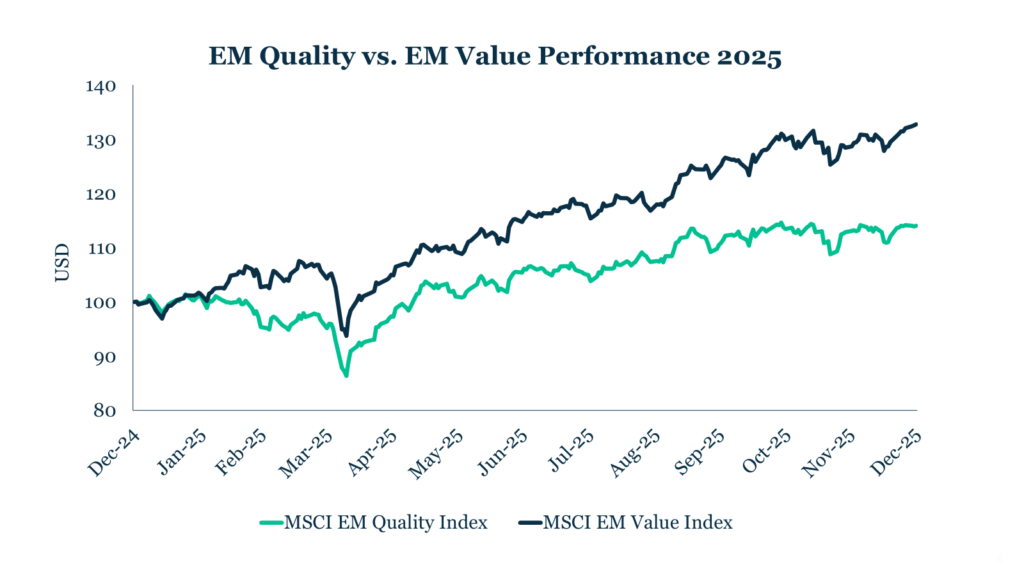

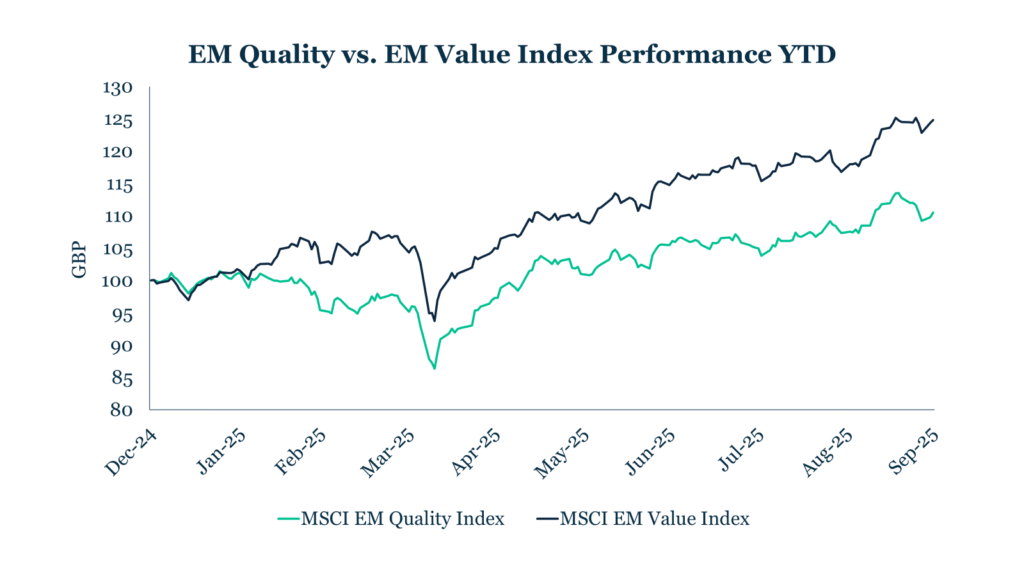

EM Quality Has Fallen Behind Value This Year

Source: Bloomberg, MCP. Figures refer to past performance. Past performance is not a reliable indicator for future performance. As of 31 December 2025.

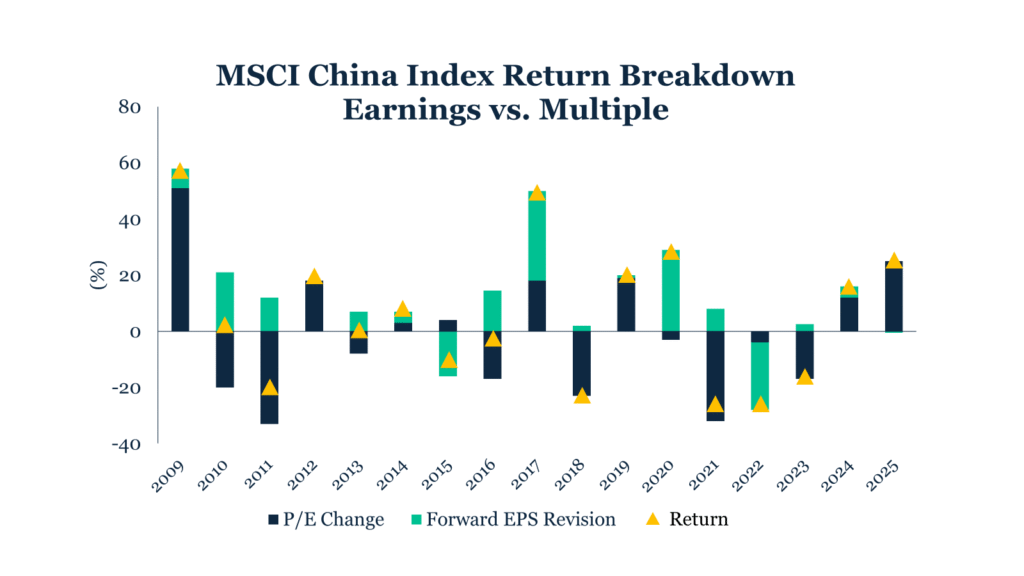

Additionally, China was a major contributor to emerging market performance in 2025, accounting for approximately 25% of MSCI Emerging Markets Index gains while representing around 23.6% of the index. However, we believe the rally has been driven primarily by multiple expansion, improved sentiment and policy support rather than an improvement in underlying fundamentals such as earnings growth.

Economic data remains weak, highlighting a disconnect between market performance and a meaningful recovery, and gains have been concentrated largely in the technology sector, where valuations have become less compelling. Structural risks also remain, including the potential for abrupt and unpredictable regulatory intervention, as experienced in 2021.

Against this backdrop, we continue to approach the market with caution, while remaining open to selectively deploying capital where individual companies meet our quality, governance and valuation criteria, without compromising discipline in pursuit of exposure.

Furthermore, performance was negatively impacted by our exposure to the software and IT services sector (19.3% in MMIT versus 1.8% in the MSCI EM Mid Cap Index as of 31 December 2025). The sector experienced tariff-related volatility, which led many corporates to delay discretionary IT spending decisions into 2026. As Gartner, a leading independent IT research and advisory firm, has noted, this resulted in “a business pause on net-new spending due to a spike in global uncertainty.”

Looking ahead, Gartner forecasts global IT spending growth of 9.8% in 2026. We view the recent weakness as cyclical, with recovery prospects supported by AI-driven demand and the resumption of previously deferred projects.

As a result of these factors, relative performance this year has not matched the strong returns achieved in prior periods. While disappointing, such outcomes are not unusual for strategies with a high active share. They are an inherent feature of a differentiated investment approach and a key driver of long-term results. Periods of softer relative performance have occurred in the past and have often been followed by improved relative outcomes as stock-specific fundamentals reassert themselves. This is reflected in the trust’s since-inception outperformance of 6.5% against the MSCI EM Mid Cap Index, despite the current year’s drawdown.

Active portfolio management remained central to the team’s day-to-day process throughout the year. We increased exposure to existing high-conviction holdings trading at attractive valuations following periods of volatility and selectively initiated positions from our watchlist, taking advantage of temporary share price dislocations in companies we believe were unfairly impacted by broader market sentiment.

This has allowed us to acquire high-quality stocks at discounts to historical valuations during one of the weaker periods of relative performance for quality companies in recent years. At the same time, we trimmed or exited positions where changes in the macro environment had, in our assessment, materially weakened the investment case.

Over the course of the year, we rigorously revisited every investment case, challenging attribution, portfolio exposures and our assumptions around earnings and valuation. Above all, we have remained committed to our investment philosophy. Our focus is unchanged: investing in high-quality, lesser-known, well-managed companies that compound value over time and align with our strategy and responsible investment principles.

Style Headwinds Have Driven Valuation Compression

Source: Bloomberg, as of 31 December 2025. * Adjusted.

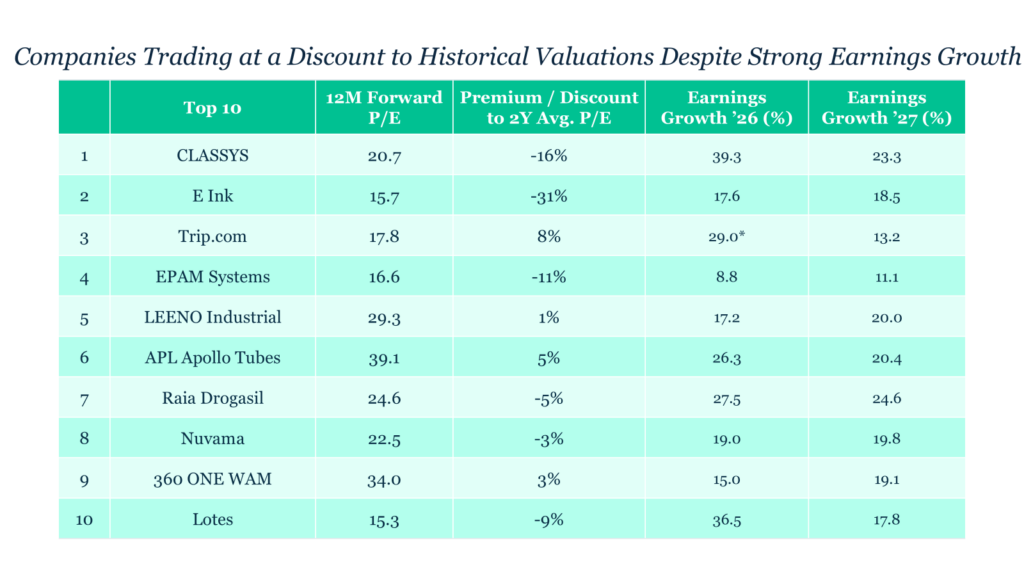

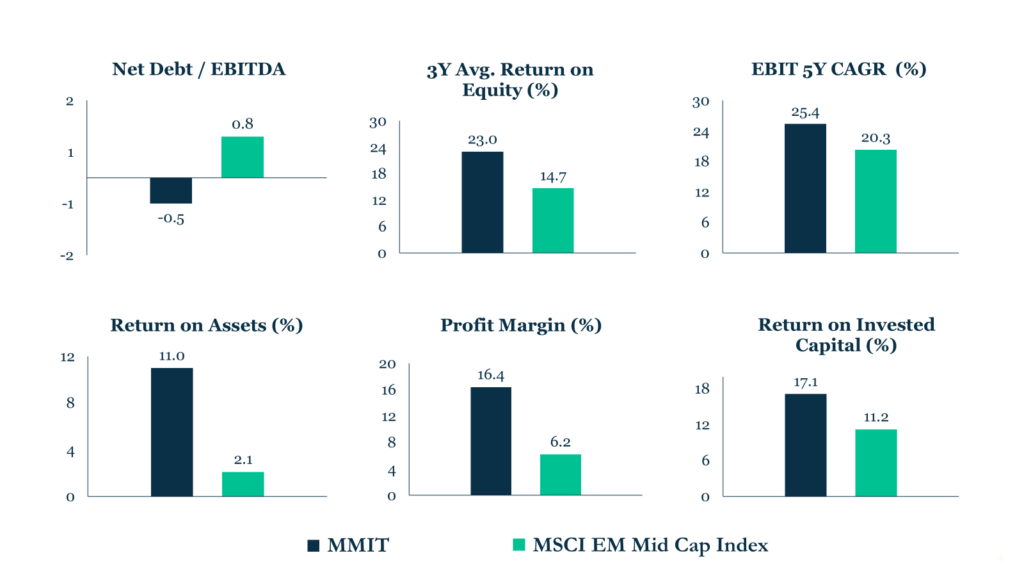

In this environment, the portfolio’s underlying fundamentals remain supportive. Market consensus forecasts a 23% forward EPS CAGR (three to five years) for the average portfolio company, supported by strong balance sheets and profitability, including a three-year average ROE of 23%, net debt/EBITDA of -0.5 and profit margins of 16%. In several cases, companies have delivered results ahead of expectations and seen earnings estimates revised upwards, yet share price performance has remained subdued.

MMIT Portfolio Offers High Growth and Profitability

Source: Bloomberg. All figures Portfolio/Index averages in USD as of 31 December 2025. Portfolio data is based on available data for portfolio companies.

Periods such as these—following a challenging year but characterised by resilient fundamentals and improving growth prospects—are often when long-term opportunities in high-quality businesses begin to emerge. In that sense, the conditions outlined throughout this commentary bring us full circle to the observation by Ruchir Sharma: “the best time to buy quality stocks is now.”

”It’s not what happens to you, but how you react that matters.”

Epictetus

Dear Fellow MMIT Shareholder,

This year reminded us what active investing truly means — to act when necessary, to be patient when appropriate, and to hold conviction when it stands tested, revisited, and reaffirmed under new circumstances.

Active investing can also mean diverging from the market — sometimes sharply. That divergence can be uncomfortable in the short term, as it has been this year, but it is also what drives long-term results. By definition, active investing means being different from the benchmark, taking positions built on conviction, not composition, and aiming to deliver differentiated and sustainable returns. In previous years, the same approach led to significant outperformance, and we believe it has once again left the portfolio better positioned for what lies ahead. Our focus remains unchanged: we aim to invest in high-quality, well managed companies that compound value over time and align with our strategy and responsible investment principles.

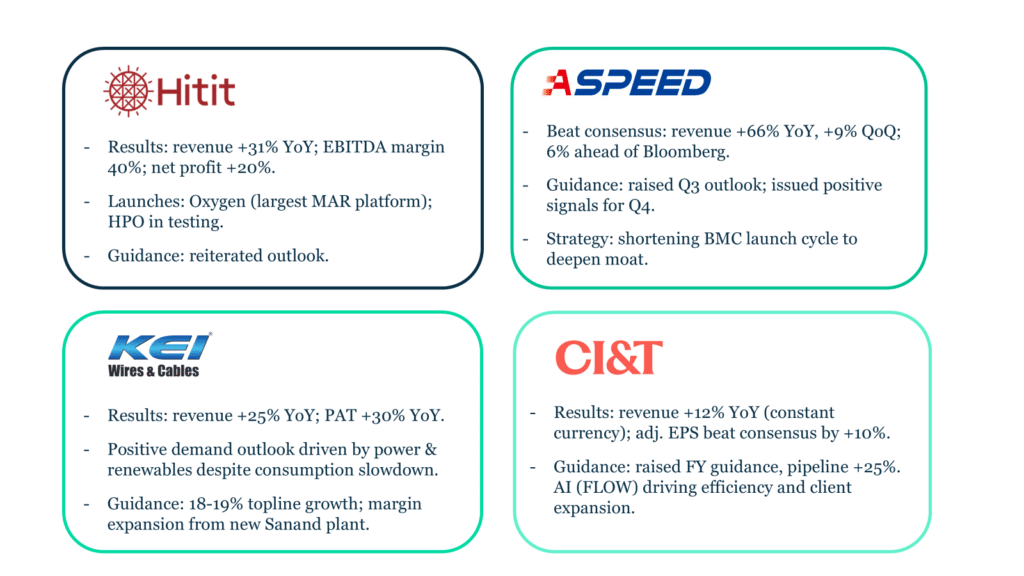

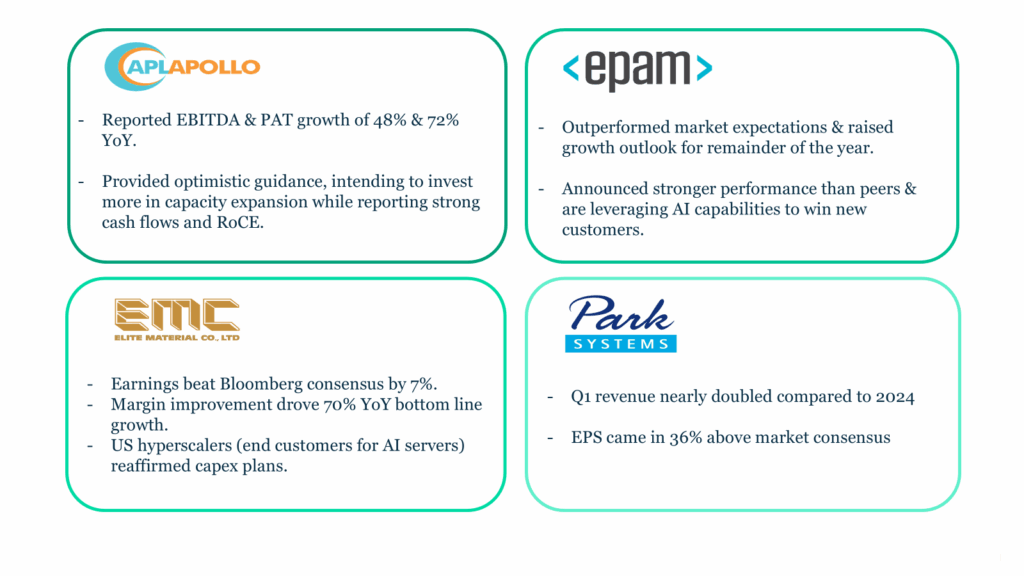

Portfolio companies have shown the same proactive spirit. CarTrade for example, expanded through the OLX integration and doubled its user reach; E Ink committed to new capacity for next-generation displays; TOTVS continued to build on its strategic acquisition of StoneCo’s Linx unit to strengthen its leadership in enterprise retail software; and Park Systems continued to broaden its nanotechnology tools across industries, just to name a few.

This spirit and innovation is clearly paying off as companies across the portfolio have delivered strong Q2 reports with many beating expectation and upgrading their outlooks for the coming years. CarTrade’s revenue increased by 22% YoY and Profit After Tax increased 106% YoY; E Ink’s revenue increased by 35% YoY and gross margin increased by 60% (+15pp); TOTVS’ earnings beat their EPS estimate by +1.6%; and Park Systems’ revenue increased by 17% YoY, 5% ahead of Bloomberg consensus.

Fundamentals Should Drive Recovery: Q2 2025 Reports

Source: MCP, Bloomberg, company source. Figures refer to past performance. Past performance is not a guide to future performance.

Despite these strong company-level results, this year has been challenging, with gains concentrated in benchmark-heavy countries and sectors. Tariff-related uncertainty in the first half of the year pushed investors toward “safe havens,” while in emerging markets, value outperformed quality as capital rotated into lower-valuation, more defensive sectors like financials amid EM rate cuts. A defence-led rally boosted industrials, and China’s stimulus- and liquidity-driven rebound lifted the benchmark.

Meanwhile, our overweight in software weighed on performance as companies delayed IT projects in a volatile environment. In general, much of the rally in emerging markets this year has been driven by a handful of mega-cap stocks, while less-known companies have attracted less investor attention. The MSCI Emerging Markets Index is up approximately 28% year-to-date, with internal analysis suggesting that the top ten Asian technology names account for almost half of these gains1.

In Q2, we began to see early signs of a potential reversal, indicating that recent portfolio headwinds may have been cyclical. This view is cautiously supported by improving macro conditions — including easing tariff volatility, momentum in AI and technology, further interest rate cuts, and a declining USD — as well as country-specific catalysts in India, Taiwan, Korea, and Brazil. While these factors could provide a more supportive backdrop, we expect any recovery to become clearer over the course of next year as these trends gradually come into play.

The quarter began with renewed tariff uncertainty as President Trump again delayed the implementation of reciprocal tariffs, allowing time for several major trade deals to be struck with the EU, Korea, and Japan. Finally, tariffs took effect on 1 August across more than 90 countries, hitting India and Brazil hardest at 50%. Since then, trade-related volatility has eased, and markets have reacted less sharply to new tariff announcements than earlier in the year, when smaller emerging-market stocks were disproportionately affected as investors rotated into larger, lower-valued names and other perceived safe-haven assets amid heightened uncertainty.

EM Quality has Fallen Behind EM Value YTD

Source: Bloomberg, as of 30 September 2025.

During the early-year volatility, we increased our exposure to existing high-conviction names and selectively added new names from our watchlist by taking advantage of attractive valuations and temporary dislocations from companies that we believe were unfairly impacted by broader market sentiment. With tariff related volatility likely subsiding, quality names, should now be better placed for a recovery.

The technology sector once again outperformed most other sectors globally, driving gains in both the US and China. Strong Q2 results from US hyperscalers and confirmation of continued large-scale AI capital expenditure reignited confidence in AI-led growth. To put this into perspective, the Guardian reported that Big Tech has invested more than $155 billion in AI this year2 — roughly equivalent to the cost of building the International Space Station. Meanwhile, policy support for domestic chipmakers and new AI product launches from China’s leading technology firms have fuelled a rally in Chinese and Hong Kong tech stocks.

Hyperscaler Capex Driving AI Momentum

Source: CL Taiwan, Daiwa.

This strength in US and Chinese technology has also supported companies, including many in our portfolio, in emerging markets like Taiwan and South Korea which play vital roles in AI supply chains. For example, NVIDIA’s Rubin GPU rollout and rising ASIC volumes are boosting demand across the semiconductor supply chain, benefitting companies such as Elite Material, a global leader in high-performance copper clad laminates used in printed circuit boards. In its Q2 report, Elite announced an additional round of capacity expansion in 2026 due to strong demand, with revenue up 40% YoY. Other examples include Chroma raising its guidance for system-level testing revenue in light of rising demand from leading ASIC and GPU projects.

Other positive macro news for emerging markets comes in the form of the Federal Reserve’s first interest rate cut of the year this September, with rates now targeted at 4-4.25%. Fed officials also hinted that further rate cuts would follow in the remainder of the year. Lower US interest rates tend to benefit emerging markets by making lower yielding developed market assets less attractive, potentially prompting investors to seek higher returns in EMs some of which are also experiencing moderating local inflation, lower public debts and higher real rates. This can boost foreign direct investment and support EM asset prices. However, the impact is uneven, as greater risk appetite and lower US yields cannot fully offset weak macroeconomic conditions or poor corporate fundamentals in certain markets. Nevertheless, the continuation of the downward trajectory of global rate cuts should be positive for emerging markets overall.

Within our key markets, local factors are at play indicating the potential for country-level recoveries. Taiwan should benefit from the global AI momentum mentioned above with its global leadership in advanced semiconductors underpinning both industry demand and geopolitical importance. Korea should profit from a semiconductor recovery, as well as governance reforms and its Value Up initiative which is creating potential to unlock shareholder value by improving governance and capital allocation.

Meanwhile, India’s combination of fiscal prudence, resilient domestic consumption grounded in a young population, moderating inflation, and pro-growth policy support creates a constructive macro backdrop underpinning the country’s long term, high growth trajectory. In Brazil, while we expect volatility ahead of the 2026 elections, there is a clear path towards SELIC rate cuts and normalisation of real interest rates which would provide a catalyst for the Brazilian equities market.

China Rally Driven by Multiple Expansion, Not EPS Growth

Source: Macquarie.

While China has dominated headlines this year with a strong market rebound placing it among the top-performing countries, we believe the rally has been driven primarily by sentiment and policy stimulus, rather than underlying fundamentals, as reflected in persistently weak economic data this quarter. The lack of a clear recovery in the real economy raises questions about the rally’s sustainability. Additionally, the rally has been largely concentrated in the tech sector which is now trading at less attractive valuations. For these reasons, we continue to exercise caution. We have been carefully screening the Chinese market across select sectors to identify companies that meet our stringent quality and governance standards. While only a few appear potentially aligned with these criteria, we remain disciplined and will continue our search without compromising on quality.

Overall, as we reflect on the year, we are reminded of Epictetus’ words: “It’s not what happens to you, but how you react to it that matters.” While this year has presented significant challenges, it has only strengthened our conviction in both our strategy and our portfolio companies. Rather than being discouraged by volatility, we used it as an opportunity to deepen our positions in high-quality, well-managed businesses.

By staying disciplined and true to our active, conviction-driven approach, we believe we are now well positioned to benefit from key macro, country and sector specific tailwinds over the coming years. Reflecting this confidence, the team has increased its investment in the strategy — a clear signal of our optimism about the future of our portfolio companies and the opportunities ahead in emerging markets which we intend to capitalise on.

On 17 October 2025, the Mobius Investment Trust portfolio manager Carlos Hardenberg hosted a webinar on Investor Meet Company to help retail investors better understand the opportunities within emerging markets, as well as outlining MMIT’s differentiated approach to generating long-term capital growth across emerging markets.

Throughout the past quarter—and indeed the entire year—we have experienced significant market volatility, driven in large part by shifting U.S. trade policies under the Trump administration, which have fuelled considerable uncertainty. Volatility peaked following the 2 April announcement of extraordinarily high, sweeping ‘reciprocal’ tariffs. This announcement shocked global markets, triggering sharp selloffs with some of the steepest price movements in decades. The subsequent pause of the tariffs to 9 July seemed only to confirm the erratic nature of U.S. policies, a sentiment further validated by the recent extension to 1 August.

Meanwhile, geopolitical tensions—including the ongoing war in the Ukraine and the escalating conflict in the Middle East—have added further layers of complexity to the global macro environment. Several emerging markets have faced their own significant challenges: India experienced a sharp market downturn in January and February; South Korea continued to navigate political instability following last year’s failed attempt to impose martial law; and Turkey came under renewed pressure after the arrest of President Erdogan’s main opposition leader. Finally, the surprise release of the Chinese chatbot DeepSeek introduced unexpected competitive dynamics in the global AI landscape, further unsettling investor sentiment.

Smaller, high-quality companies, particularly in the technology sector, were disproportionately affected by the uncertainty as investors fled to safe heaven assets like gold but also to the larger, more liquid names deemed to be less risky. Furthermore, amidst the volatility, we observed a market rotation into sectors such as banks and commodities. These areas, which we deliberately exclude from the portfolio due to their regulatory complexity, capital intensity, and limited pricing power, had already been trading at low valuations and therefore proved more resilient during recent market corrections.

Our portfolio is benchmark-agnostic, with an active share close to 100%, reflecting our high-conviction, bottom-up stock selection. While this naturally leads to periods of return divergence against the broader market, we believe it positions us well to deliver meaningful long-term outperformance for investors. We’ve navigated challenging periods before, such as in 2019 and 2022, and in both instances, the trust went on to deliver strong (out-)performance in the years that followed. As the dislocation begins to correct, MMIT’s NAV and share price have started to recover, delivering 6.5% and 5.2% in GBP terms over the quarter. Since inception, the trust has delivered a NAV return of 54.8%.

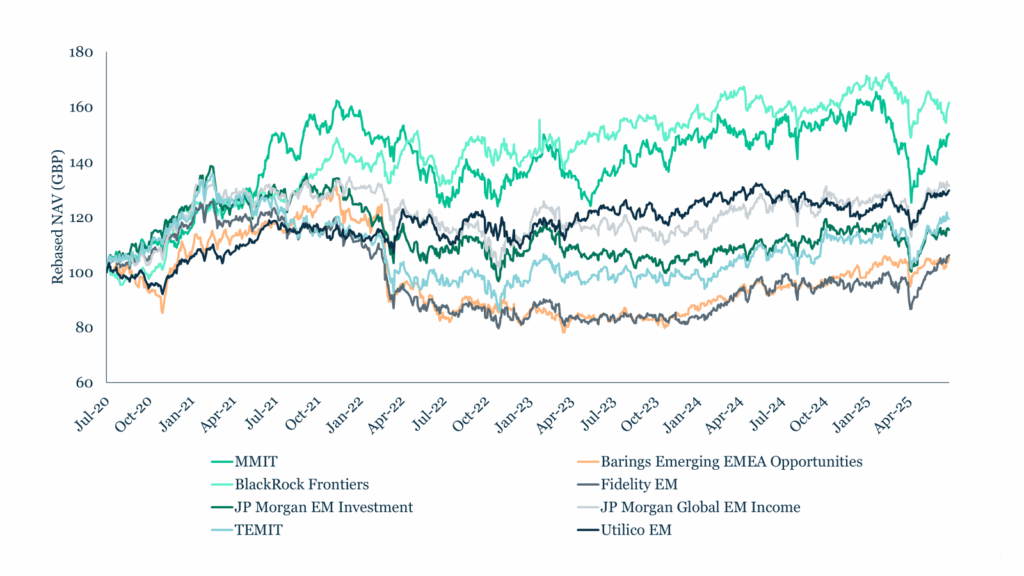

MMIT is one of the Leading EM Trusts Over the Past 5 Years*

Source: Bloomberg, Frostrow, MMIT, rebased. As of 30 June 2025.

We viewed the recent market pullback as an opportunity to further strengthen the portfolio. We selectively added high-conviction names from our watchlist, taking advantage of attractive valuations and temporary dislocations. Active portfolio management has remained central to our day-to-day work: we trimmed or exited positions where, in our view, the macro environment had materially weakened the investment case and redeployed capital into more compelling opportunities. At the same time, we increased exposure to several high-conviction holdings that had been unfairly impacted by broader market sentiment.

Encouragingly, many of our portfolio companies delivered strong Q1 results, with several beating expectations and issuing positive forward guidance, despite ongoing uncertainty.

Strong Q1 Results, Optimistic Outlook for 2025 & Beyond

Source: MCP, Bloomberg, company source. Figures refer to past performance. Past performance is not a guide to future performance.

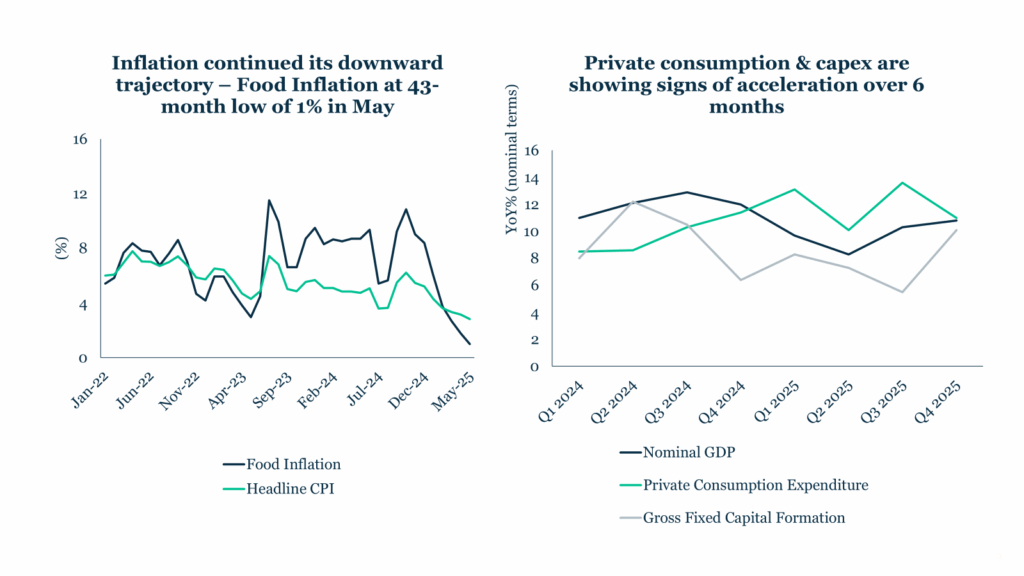

Our extensive on-the-ground research this year—spanning visits to Taiwan, India and Korea—provided valuable insight and generated a number of promising new ideas. India stands out as a particularly strong focus for us. We took advantage of market weakness earlier this year to add undervalued names, supported by an improving macro backdrop that includes rate cuts, easing inflation, and increased liquidity in the banking sector.

Economic Indicators Point to Continued Recovery in India

In Korea, the outcome of the 3 June elections brought political stability, which has boosted stock performance. The new government is pursuing a broad agenda of market-friendly reforms, not only to tackle the longstanding ‘Korea discount’, but also to enhance overall corporate governance, capital efficiency, and investor confidence. As a result, new opportunities are emerging, particularly in the technology sector. Brazil has also remained on our radar, with compellingly low valuations, improving macro fundamentals, and a strengthening real contributing to a more constructive outlook.

From a sector perspective, we have been active as well. In health care, we began reducing our position in Korean medical aesthetics company Classys after realising significant profits over the course of the holding period. In industrials, we added to APL Apollo and bought KEI Industries in India to capitalise on Indian infra and energy capex demands.

In consumer discretionary, we added CarTrade given its dominant position in car classifieds in India catering towards local consumption growth. We remain bullish on the technology sector; however, the composition of our tech holdings has been thoughtfully realigned to reflect our evolving views amid current macroeconomic challenges, broader market trends, and shifting IT spending priorities.

Following the ‘DeepSeek scare’ —when Chinese AI start-up DeepSeek introduced a large language model (LLM) with performance on par with Western counterparts but developed at significantly lower cost—Q1 results from hyperscale cloud providers such as Amazon and Alphabet reaffirmed the robust momentum of AI-related investment. The reality remains that businesses globally are accelerating their transition toward AI-driven models, necessitating sustained, large-scale investment in compute infrastructure. Encouragingly, many of our portfolio companies in the technology sector echoed this trend in their Q1 earnings reports, providing constructive guidance for the year ahead and pointing to an emerging rebound in demand, driven by renewed strength in AI-related spending.

For example, Chroma, a Taiwanese supplier of testing equipment, beat Bloomberg earnings consensus by 48% driven by a 11% increase in operating margin year-on-year, and a 55% year-on-year revenue growth. Demand for Chroma’s power testers was supported by China’s aggressive AI datacentre build out, and the company’s outlook remains constructive for the rest of the year as it is entering a leading foundry’s packaging supply chain with a customised metrology tool.

Meanwhile, Elite Material (EMC), the global leader in high-speed copper-clad laminates (CCLs), reported earnings 7% ahead of Bloomberg consensus. EMC’s tailwinds came from strong demand for higher-priced CCLs, predominantly used in Application-Specific Integrated Circuit (ASIC) servers, which drove a 70% YoY bottom line acceleration. The reaffirmation of US hyperscalers’ (the end customers for AI servers) capex plans has reinforced EMC’s positive outlook.

The careful refinement of the portfolio has culminated in a deliberate and focused consolidation into 25 high-conviction holdings—companies we believe are best positioned to deliver sustainable, long-term growth. This portfolio is testament to our continued focus on high-quality businesses with deep moats and a strong orientation toward innovation (see section on top holdings below). Throughout periods of market volatility, we have remained disciplined and patient, staying true to our convictions and consistently executing the strategy we set out.

While we monitor macroeconomic developments closely, we adjust our positioning only when we believe such shifts materially affect a company’s long-term investment case. Underscoring our confidence in the strategy, the investment team increased its own commitment to the trust during the recent market pullback—demonstrating strong alignment with long-term shareholders. Much like the rebounds that followed challenging periods in 2019 and 2022, we view 2025 in a similar light. With improving visibility into the remainder of the year, we believe there is good potential for continued recovery, despite ongoing volatility and near-term challenges.

Outlook

Looking ahead, U.S. trade policies continue to inject a persistent sense of uncertainty and volatility into the economic outlook for the coming months. The initial 90-day reciprocal tariff pause—subsequently extended by an additional month—was designed to create space for the U.S. to negotiate new trade agreements. Yet, progress has been limited. To date, only the United Kingdom, Vietnam, Indonesia and China – though limited in scope – have reached accords, highlighting the limited effectiveness of a strategy centred around economic pressure.

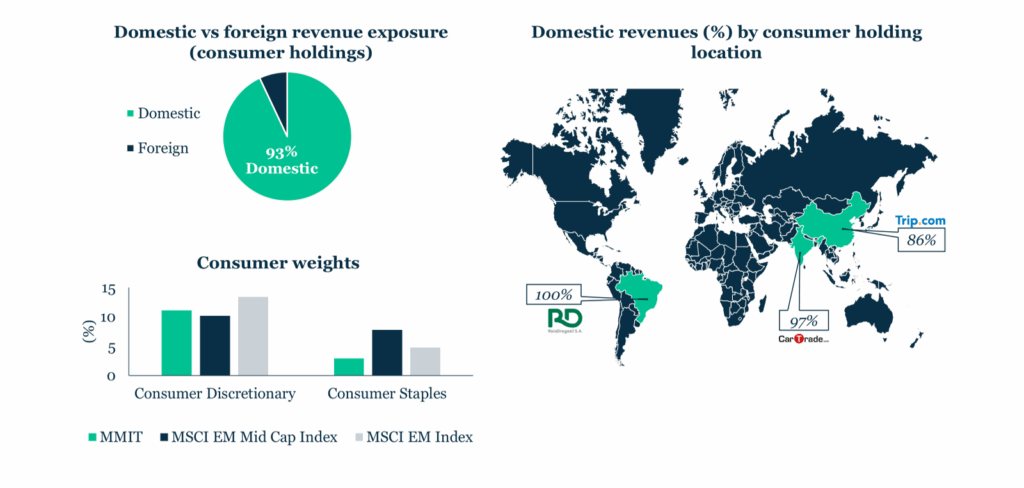

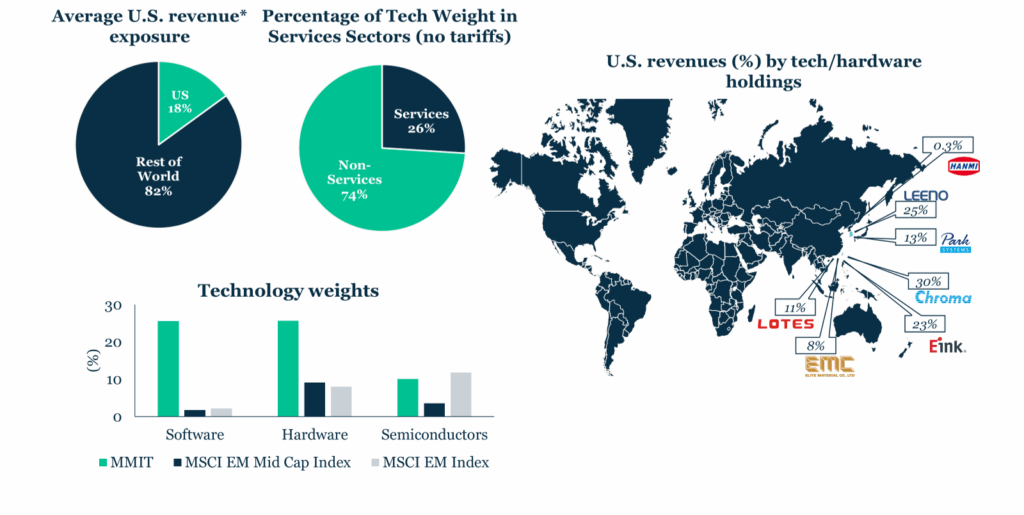

We continue to monitor the potential impact of heightened tariffs on our portfolio. However, direct exposure seems to be modest. Firstly, a large portion of our technology exposure is based in the software-as-a-service industry, and as services, these are not subject to tariffs.

Secondly, our remaining tech holdings, primarily in the semiconductor and hardware sectors, which are largely currently exempt from tariffs, generate only a limited share of their direct revenue from the U.S. market.

Thirdly, we favour business models oriented towards domestic consumption in select geographies, such as India, which similarly have minimal direct exposure to the U.S. Nonetheless, we continuously monitor the potential broader impact of the seemingly erratic U.S. policies on our portfolio.

Source: Bloomberg, MCP. As of 30 June 2025. Revenue data for FY2024.

MMIT Tech Holdings Show Low Direct Exposure to the U.S.

Source: Bloomberg, MCP. As of 30 June 2025. Revenue data for FY2024. Actual exposure through direct shipments is significantly lower than revenue exposure (e.g., Taiwan equipment maker shipping to OSATs and receiving revenue from US customer).

More broadly, the U.S. may be absorbing greater-than-expected fallout: rising inflation, weaker growth and confidence, and a softening dollar suggest a reversal in the decade-long USD strength—potentially a tailwind for emerging markets. With EM inflows rebounding ($19.2bn in May, tracked by the Institute of International Finance (IIF)), and a shift away from concentrated U.S. exposure, we believe our portfolio is well positioned to benefit.

* The Company has selected the following eight companies from the AIC’s Global Emerging Markets sector to form its peer group. These were chosen based on alignment with the Company’s own investment universe, excluding a small number of regionally focused trusts with narrower mandates. The selected peers are: Ashoka WhiteOak Emerging Markets (not in graph above as no 5 year track record), Barings Emerging EMEA Opportunities, Fidelity Emerging Markets Limited, BlackRock Frontiers Investment Trust, JP Morgan Emerging Markets Investment Trust, JP Morgan Global Emerging Markets Income Trust, Templeton Emerging Markets Investment Trust, and Utilico Emerging Markets Trust.

On 24 June, the Mobius Investment Trust portfolio manager Carlos Hardenberg hosted a webinar on Investor Meet Company to help retail investors better understand the opportunities within emerging markets, as well as outlining MMIT’s differentiated approach to generating long-term capital growth across emerging markets.

Despite a volatile macroeconomic environment, the Trust maintains high conviction in select small and mid-cap companies with strong margins, governance, and innovation-led business models – particularly in India, Taiwan, and Southeast Asia. The portfolio, concentrated in fewer than 30 holdings, has achieved a 44.4% return since inception and outperformed both the MSCI Emerging Markets Index and its LSE-listed peers over the past 5 years. With earnings growth in emerging markets forecast at 14-16% for 2025-2026, MMIT sees an inflection point driven by attractive valuations, resilient GDP growth, favourable demographics, and global decoupling from overvalued developed markets. The Trust actively avoids overexposed sectors and geographies like China, maintains liquidity discipline, and integrates ESG factors into its investment process. Management is exploring portfolio gearing to enhance upside potential and continues to focus on aiming to deliver superior risk-adjusted returns. With a high active share and deep on-the-ground research, MMIT is likely to benefit from innovation-led value creation across emerging markets. Investors are encouraged to view the current discount as a long-term opportunity.

Uncertainty and shock over the reciprocal tariffs announced on ‘Liberation Day’ by the new US administration has, to put it bluntly, created market chaos. The sharp global sell-offs are reminiscent of the turmoil experienced during the Covid-19 pandemic. As was the case then, few have been spared. Trump’s recent decision to delay reciprocal tariffs for 90 days applicable to any country that has not retaliated, has provided markets with what appears to be a temporary lifeline.

However, we do not interpret this as a signal that markets have bottomed, nor do we assume this policy will necessarily hold givenTrump’s unpredictability. Rather, this move appears to reflect a form of targeted pressure—some might say economic bullying—directed against China, particularly given that it remains the only country to have retaliated thus far. As a result, market confidence has been deeply shaken and we can expect elevated volatility and uncertainty to persist in the coming months.

Like many, we had anticipated the possibility of rising protectionism under a second Trump administration, though not to the extent we seem to be witnessing now. In recent months, we have proactively assessed the potential impact of higher tariffs on our portfolio. Each individual position has been carefully reviewed under this assumption, and we continue to re-evaluate our holdings in light of the evolving situation.

As far as the direct impact of Trump’s reciprocal tariffs is concerned, we believe companies exporting physical goods to the U.S. from countries facing the steepest approved tariff increases are likely to be most affected. Fortunately, although our portfolio includes companies based in several of these countries—which could be hit hard if the announced ‘Liberation Day’ tariffs are fully implemented—our current assessment suggests the immediate impact on our holdings may be limited. Many of our portfolio companies have minimal direct export exposure to the affected sectors, providing a degree of insulation from near-term disruption.

Take Classys, a Korean medical device manufacturer facing a potential 32% tariff on its U.S. imports. The company derives less than 5% of its revenue from sales to the U.S., significantly reducing the potential impact on overall earnings. The bulk of its revenue, approximately 35%, comes from the domestic Korean market, while Europe and Southeast Asia each contribute around 20%. Japan and Brazil account for roughly 10% each, providing further geographic diversification.

Additionally, the top three US-revenue exposed companies in our portfolio are asset-light, IP-based software companies. As a services industry, they are not directly targeted by the new tariffs. Furthermore, semiconductors are currently excluded from the newly announced tariffs. But the situation remains highly fluid. While chips themselves are not directly taxed, components that contain them, such as laptops and smartphones, had been at risk of future levies. However, over the weekend, the White House appeared to grant temporary exemptions for certain electronics, including smartphones, laptops, hard drives and flat-panel monitors. At the same time, a Section 232 investigation into semiconductor imports has been launched, raising the prospect of targeted tariffs based on national security grounds. We are closely monitoring developments in this sector, as it remains a potential flashpoint in the broader trade narrative.

Finally, we also prioritise business models oriented towards domestic consumption in select markets. As a result, our consumer holdings have minimal direct exposure to U.S. demand, with the exception being a Turkish apparel retailer, which derives less than 5% of its revenue from the U.S.

Beyond the direct taxation of goods, few businesses are likely to escape the broader, more insidious effects of escalating tariffs. Even in cases where companies are not directly targeted, tariff-induced slowdowns in demand and profitability can ripple through global supply chains, dampening investment sentiment and tightening margins. These second-order effects pose significant risks—not just to individual companies, but to entire economies. From shifts in consumer spending patterns to declining trade volumes and tightening financial conditions, the cumulative pressure could contribute to a broader global economic slowdown. We are actively assessing these cross-currents as we evaluate portfolio exposure and position for resilience.

In the meantime, the trade war between the US and China has exploded into full force. At the time of writing, the US has imposed tariffs of 145% on Chinese imports, while China has responded with tariffs of 125% on US goods. Who knows how much higher these could go. This extreme tariff war between the US and China alone will have serious repercussions across the global economy.

Amidst the chaos here are some glimmers of light on the tariff horizon. It’s worth remembering that we’ve been through a Trump-led trade war before, and global trade patterns had already begun to shift well before the current escalation. One of the most important structural changes over the past few decades has been the rise of South-South trade, particularly across Asia. Between 2007 and 2023, trade among developing countries more than doubled, from $2.3 trillion to $5.6 trillion, largely driven by Asia1. Intra-Asia trade alone is projected to grow from $4.3 trillion in 2023 to $7.1 trillion by 20302.

This diversification accelerated following the 2018 U.S.-China trade war, prompting countries to reduce reliance on U.S. imports. For example, China’s share of exports to the U.S. declined from 19% in 2017 to 14.7% in 20243. At the same time, many countries have been pursuing bilateral and regional trade deals that exclude the U.S. Notably, the Regional Comprehensive Economic Partnership (RCEP), signed in 2020, includes 15 Asia-Pacific nations and covers around 28% of global trade.

Although the U.S. will remain a dominant global importer, the accelerating pivot away from dependence on its market places many economies in a stronger position to withstand rising U.S. tariffs. We expect this trend to continue gaining momentum in light of recent developments, as countries intensify efforts to expand trade partnerships beyond the U.S.

In this uncertain environment, our top priority is to stay close to our portfolio companies and continuously reassess our investment theses in light of new insights and ongoing dialogue with stakeholders. To that end, we have scheduled additional research travel to remain close to developments on the ground and ensure we are ready to adapt swiftly as conditions evolve—especially given the many unknowns that remain, including the durability of the 90-day pause and the potential for new trade deals.

We believe experience and steadiness are vital during periods of heightened volatility. The MCP team has been through many market cycles, including the Asian financial crisis, the global financial crisis, and—during MCP’s own tenure—the Covid-19 pandemic. Since our launch in 2018, amid the first U.S.-China trade war, we believe we have guided the fund through an extraordinary period marked by global disruption, rising geopolitical tensions, inflationary shocks, tech sector uncertainty, and the renewed political ascent of Donald Trump.

Today’s surge in market volatility bears strong resemblance, in our view, to the dislocation seen in early 2020, when fear overtook fundamentals. At that time, we believe the team responded swiftly and strategically repositioning the portfolio to take advantage of market dislocations and initiating positions in high-quality companies from our watch list. These were businesses with sound fundamentals and durable models, which we believed were being unduly punished by market sentiment.

We believe this timely and deliberate response, combined with the quality of our portfolio holdings—characterised by competitive strength, solid balance sheets, robust corporate governance, and leadership in innovation—was a key contributor to the fund’s strong outperformance. By 8 October 2020, just 261 days after the Covid-related market peak, MMIT had recovered its losses. From the trough to the subsequent peak on 11 November 2021, the fund delivered a return of 168.7% over a 660-day period, before concerns around global rate hikes began to weigh on broader markets.

As long-term investors, we view the current environment through a similar lens. We do not believe this is a time to retreat, but rather an opportunity to build positions in resilient companies with strong fundamentals—businesses we believe are well-positioned to benefit from a long-term recovery particularly as history shows that the subsequent bull market tends to outperform its preceding bear market.

On 11 March 2025, MCP Emerging Markets hosted a Zoom webinar where founding partner Carlos Hardenberg and investment analyst Swathi Seshadri provided an update on the strategy, performance and portfolio of the Mobius Investment Trust (MMIT).

The video below is a replay of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.

We are pleased to announce that the Mobius Investment Trust has been nominated in the Global Emerging Markets category at the Citywire Investment Trust Awards 2024.

On 6 June 2024, Mobius Capital Partners held a Zoom webinar where founding partner Carlos Hardenberg provided an update on the strategy, performance, and portfolio of the Mobius Investment Trust.

The video below is a recording of the webinar.

Please email Anna von Hahn at anna@mcp-em.com should you have any questions or would like further information.